What are ETFs?

Exchange Traded Funds or ETFs for short, are often associated with index-tracking funds that trade on the stock exchange like shares.

Their tracking feature means that the ETFs hold a basket of shares that match the index. For example, one cannot theoretically buy directly into the S&P 500 index, the most popular index in the world. However, one can replicate that index through various index ETFs such as the SPY ETF, which seeks to track the S&P 500 passively.

The SPY ETF will hold the same shares, with the same composition as that of the S&P 500 index. Hence, for an investor who wishes to replicate the performance of the S&P 500 index, he/she just need to purchase the SPY ETF.

Why buy ETFs? 4 Key reasons to purchase ETFs

An ETF combines the benefits of a fund and a share in one security. Here are 4 key reasons why you should consider a purchase of ETFs.

#1 – Diversification

Similar to a fund, purchasing an ETF allows an investor to invest cost-effectively in entire markets with just a single security. I highlighted the SPY ETF earlier, which allows an investor to spread his investment across 500 of the largest US-listed companies.

For those who wish to gain even more exposure to more companies through a single security, one can check out an ETF such as the Vanguard Total World Stock ETF (Ticker VT) which buys into 9,461 stocks. That is as much diversification as you can get, simply through 1 counter.

#2 – Easy to get started

Unlike a unit trust or a mutual fund which is not actively traded over the exchange, and hence not easily accessible to the man-in-the-street, buying ETFs is as simple as buying stocks, since these ETFs are actively traded on the stock exchange (for eg NYSE).

Investors who wish to purchase a unit trust/mutual fund will typically need to access these products through a specialized brokerage platform. For example, in Singapore, one of the largest brokerage platforms that one can have access to unit trust/mutual fund products is FSMOne.

Most typical brokerage platforms, however, do not offer such products to retail investors.

On the other hand, since ETFs are traded just like stocks, they will be easily accessible.

#3 – Transparency in pricing

ETFs are traded on the stock exchange similar to shares. As such you can buy and sell ETFs at any time during trading hours based on the price that is available for all to see.

In comparison, mutual funds are traded only once a day via the investment company. Hence, the pricing isn’t as transparent and it is more difficult to be actively trading mutual funds based on short-term strategies (ie day trading)

#4 – Flexibility

There are ETFs available to track everything from stocks held in a particular index, to those in key sectors. Beyond stocks, ETFs can also be available to track other asset classes such as bonds, commodities, and even currencies.

Some of the largest and most popular bond ETFs are the likes of Vanguard Total Bond Market Index Fund (BND) for market diversification, the Vanguard Short-term inflation-protected security (VTIP) for protection against inflation, or perhaps the iShares 20+ Year Treasury bond ETF (TLT) for the largest leverage to rate movements.

There are also various commodity ETFs available to track a broad commodity index passively, such as the Invesco DB Commodity Index Tracking Fund (DBC) or to target specific commodities such as Gold, by which the most popular one is undoubtedly the SPDR Gold Shares (GLD).

There are also currency ETFs, although these are not as popular, and the main usage is typically to track the strength of the US Dollar against a basket of currencies. The most popular currency ETF is the Invesco DB US Dollar Index Bullish Fund (UUP)

Passive ETFs vs. Active ETFs

I highlighted earlier that buying an ETF, such as the SPY, is an easy solution to track the performance of a key index (in this case the S&P 500), on a passive basis. There are many passive ETFs and the key advantage of these ETFs are that typically spot low expense ratios.

The expense ratio is the operating expenses associated with the running of the ETF. These are the additional costs that an investor will need to pay vs. owning a stock (which has no operating costs)

Since a passive ETF does not require active management, there is a very low expense ratio associated with it. Some of the world’s largest passive ETFs (by asset under management) such as the Vanguard S&P 500 ETF (VOO) have an expense ratio of only 0.03%.

This means that if you have got $1,000 invested in VOO, the recurring annual expense that you have to pay for the ownership of this ETF is just $0.30 per year.

Do note that the expense ratio is typically adjusted into the prices of the ETF already, hence it might not be as evident as a direct expense such as commissions that a brokerage charges or advisory fee that a Robo advisor platform charges.

Do note that there are increasingly more ETFs that are “actively” managed. Active ETFs have a manager or team making decisions on the underlying portfolio allocation on a day-to-day basis, hence not adhering to a passive investment strategy.

Active ETFs feature many of the same benefits of a traditional passive ETF like price transparency, liquidity, etc, but with a fund manager that can adapt the fund to changing market conditions. Hence, the combination of active management + ETF provides investors with an innovative solution to asset management.

Active ETFs have higher expense ratios compared to passive ETFs such as the VOO ETF. This put pressure on fund managers to consistently outperform the market. One of the most popular active ETFs in the last few years is the family of ETFs run by ARK-Invest.

Tax-related issues associated with ETFs

There are 1000s of ETFs that are currently listed. Most investors will likely be exposed to US-domiciled ETFs. These are ETFs that are registered in the US. Most ETFs are domiciled in the US.

There is another category of ETF which is domiciled in Ireland and Luxembourg (often listed in the UK). These are ETFs approved for sale in the EU and are recognizable by the acronym UCITS in their name.

UCITS is a set of EU regulations that sets standards for counterparty risk, asset diversification, information disclosure, and other consumer protections. US ETFs are not governed by UCITS principles and may also be subject to tax disadvantages, the biggest of all being withholding taxes on dividend distribution.

Withholding taxes

Typically when it comes to analyzing the “cheapness” of an ETF, most investors will focus on the ETF’s expense ratio which is the direct operating cost associated with managing the fund.

However, there is another indirect component that investors should look to minimize and that is the withholding taxes on dividend distribution.

For non-US-based investors (Singaporean investors for example) purchasing a US-domiciled ETF (which is often the case), one will incur a dividend withholding tax. This means that if the US ETF has a dividend yield of 3% for example, a Singaporean vested in this ETF will not get the full 3% yield. Instead, some of the yields will be “lost” to withholding taxes.

This is an indirect expense that is often evident to investors but should still be considered when purchasing US-domiciled ETFs. The higher the dividend yield of the ETF, the greater will be the indirect cost associated with dividend withholding taxes.

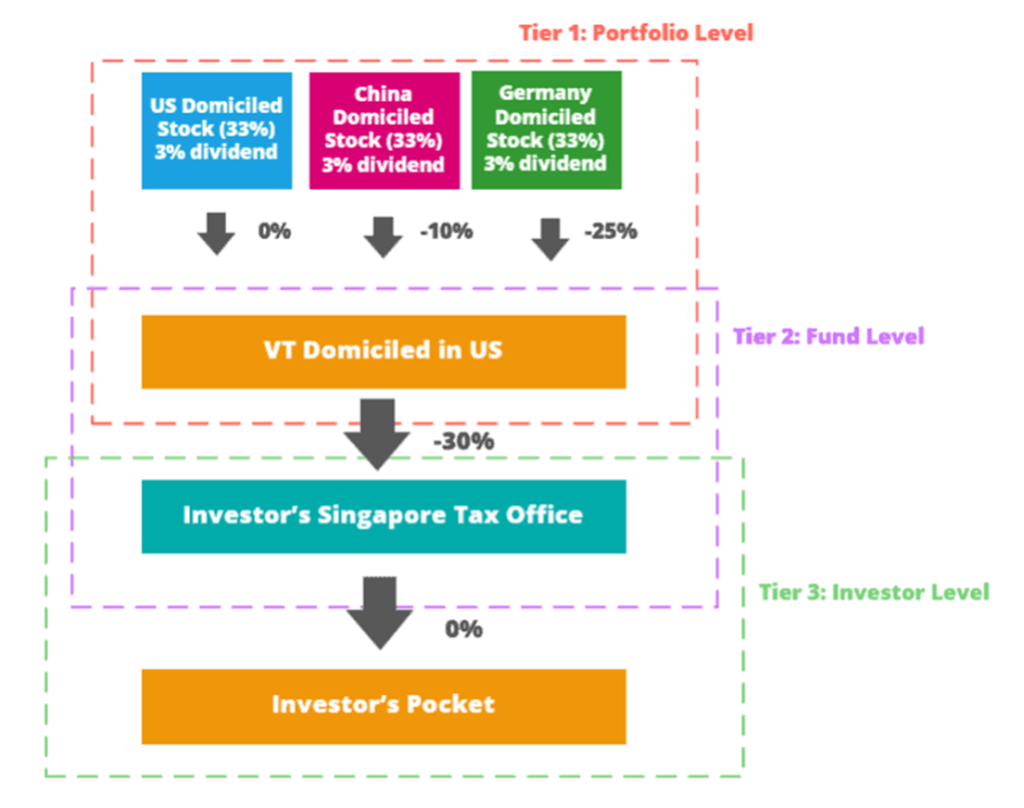

US-domiciled ETFs

Let’s use a quick example based on the diagram below to illustrate the impact of dividend withholding taxes on a US-domiciled ETF like VT.

There are 3 levels that an investor should be aware of. Level 1: Portfolio Level, Level 2: Fund Level, and Level 3: Investor Level

In level 1, when the individual companies declare a dividend to the ETF, there could be withholding taxes involved. Since VT holds a myriad of stocks and when these stocks declare a dividend, there will be different levels of withholding taxes involved.

To simplify matters, let us just assume that VT only holds US, China, and Germany domiciled stocks. For US stocks, there will be ZERO dividend withholding tax for US-domiciled ETFs on the portfolio level. Hence, if the ETF only holds predominantly US stocks such as the SPY ETF, there is essentially no/minimal withholding tax on the portfolio level.

China and German stocks are subjected to 10% and 25% withholding taxes on the portfolio level.

Level 2 is the fund level. For a US-domiciled ETF, after collecting all the dividends from the individual companies, they are then distributed out to shareholders of the ETF. If you are a US-based shareholder of VT, there will not be a 30% withholding tax. If you are a non-US-based shareholder (Singaporean investor for example), you are now subjected to a 30% withholding tax on the Fund Level.

Level 3 is the investor level, which for a Singaporean investor, it is typically at 0%.

So, what is the impact of the 3 levels of withholding tax for a Singaporean investor in the above simplified VT example with equal holdings of US, China, and Germany stocks (33% each).

US Stock Dividend received: 3% * (1-0.0) * (1-0.30) * (1-0.0) * 33% = 0.7%

China Stock Dividend impact: 3% * (1-0.1) * (1-0.30) * (1-0.0) * 33% = 0.62%

Germany Stock Dividend impact: 3% * (1-0.25) * (1-0.30) * (1-0.0) * 33% = 0.52%

Total Dividend received = 0.7% + 0.62% + 0.52% = 1.84%

Withholding tax impact = 3% – 1.84% = 1.16%

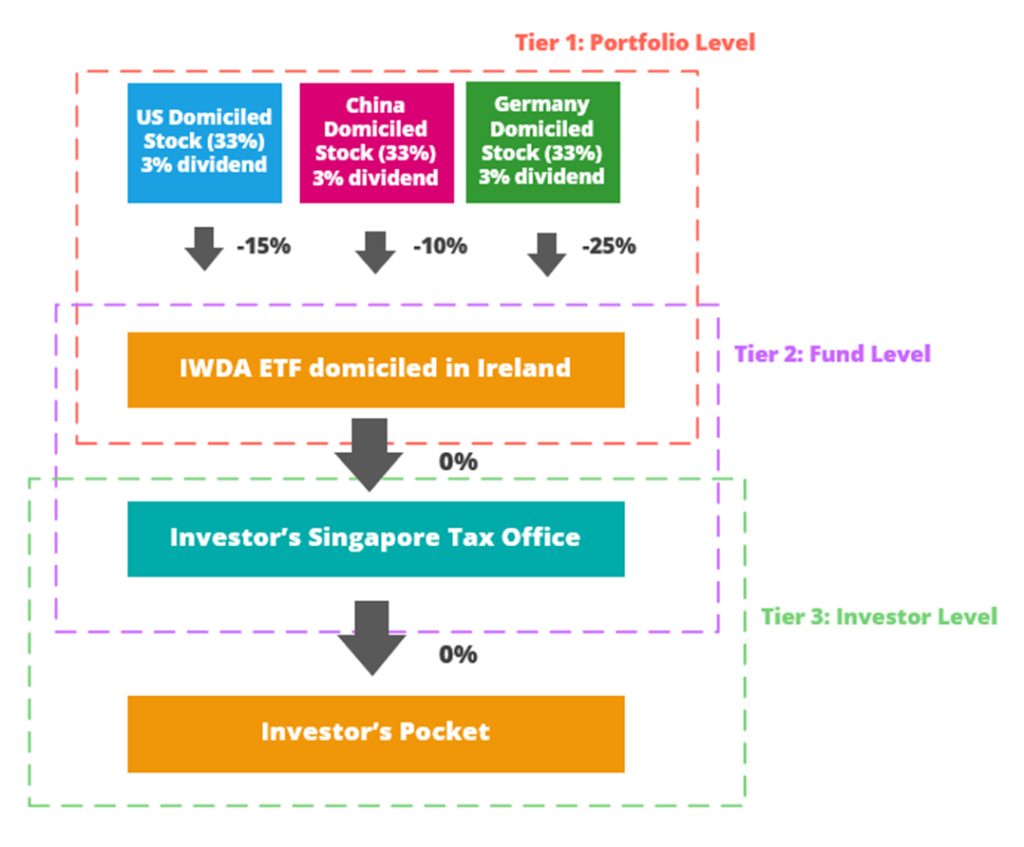

Non-US-domiciled ETFs (UCITS ETFs)

Now let’s take a quick look at a similar UCITS ETF (vs. VT) such as the IWDA (UCITS ETF)

For IWDA, since it is domiciled in Ireland, US companies that declare a dividend will need to be subjected to a 15% withholding tax on the portfolio level. The withholding tax on China and German stocks are assumed to be the same.

On the fund and investor level, there is no withholding tax payment required for a Singaporean investor. Let us quickly calculate the withholding tax impact.

US Stock Dividend received: 3% * (1-0.15) * (1-0.0) * (1-0.0) * 33% = 0.84%

China Stock Dividend impact: 3% * (1-0.1) * (1-0.0) * (1-0.0) * 33% = 0.89%

Germany Stock Dividend impact: 3% * (1-0.25) * (1-0.0) * (1-0.0) * 33% = 0.74%

Total Dividend received = 0.84% + 0.89% + 0.74% = 2.47%

Withholding tax impact = 3% – 2.47% = 0.53%

The overall withholding tax impact based on this simplified example (using VT and IWDA) shows that, for a Singaporean investor, it seems more efficient to be vesting in UCITS ETF (0.53% withholding tax) vs. US-domiciled ETF (1.16% withholding tax).

However, this is purely from a withholding tax impact and there could be other considerations such as commissions costs involved for UCITS ETF that might totally eliminate its cost advantage from a dividend angle.

Additional Reading: UCITS ETFs taxation. Are they that cost-efficient after all?

For high-yielding ETFs, it is more advantageous to be looking at a UCITS ETF (assuming there is one) vs. US-domiciled ETF and purchased through a low-commission cost platform. One can also be looking at purchasing these high-yielding UCITS ETFs through Robo Advisor platforms (commission cost replaced by advisory/platform costs). However, the choices might be very limited.

If I am looking to engage an income strategy to grow my stream of passive dividend income, I will want to be looking at a high-yielding UCITS ETF vs. a US-domiciled ETF so as to minimize or totally eliminate the impact of dividend withholding taxes on the dividends distributed.

One such ETF that might be interesting is the FTSE All-World High Dividend Yield UCITS ETF (VHYL) that is denominated in GBP. It has a yield of about 4%. If one ignores the risk of GBP depreciation, then the other expense considerations will be 1) commission costs (approx 0.2%), 2) FX conversion charges (by platform approximating 0.4%), and 3) Expense ratio (approx. 0.29%).

That will amount to about 0.9% which is the one-time initial charge, with recurring charges being the 0.29% expense ratio.

I will disclose more about the brokerage platform to use in a separate video guide.

Tips and Tricks to selecting the right ETFs

There are a few key tips I will like to highlight when selecting the right ETF to begin one’s investing journey.

Using ETF is likely the simplest and easiest manner for a newbie investor to get started on his/her investing journey without incurring significant costs. However, with a wide array of ETFs to choose from, it can get confusing at times.

Here are some tips which you can consider to help you find the right ETF for your investment objective.

Tip #1: Differentiating Passive and Active ETFs

Do you want to invest in an ETF that mimics a particular index or do you wish to have an active fund manager to make changes to your portfolio according to his/her expertise? Data has shown that active management DOES NOT lead to outperformance, particularly when the higher operating expenses to manage the fund is being considered.

Most beginner investors should stick with passive ETFs for a start. One could select an ETF that mimics your home market index (which you are likely familiar with) or select a more diversified approach by investing in the entire universe through a global market ETF.

Once you have gotten the confidence to invest in these passive ETFs, preferably on a recurring basis through a dollar cost average approach, you can select riskier but potentially higher reward products such as thematic ETFs, etc.

Tip #2: Look to minimize the expense ratio as much as possible

The expense ratio is the recurring cost that one would have to pay annually for the maintenance of the portfolio. Hence, a high expense ratio is often the cause of underperformance on a longer-term basis.

Compare and select the best-known, broadest indices that follow the market you wish to track. For example, there are many ETFs that seek to track the performance of the S&P 500. Which is in fact the best in terms of cost minimization (aka lowest expense ratio)?

The table below shows the 4 key ETFs that track the S&P 500. While most investors typically associate the SPY ETF with the S&P 500, it is the VOO ETF that has a much larger asset under management.

In terms of expense ratio, SPY has the highest expense ratio at 0.09% and also the worst return on a 5 and 10 years horizon vs. its peers.

It makes more sense to be vested in the other ETF (vs. SPY) if one wishes to track the S&P 500.

Tip #3: Consider withholding taxes on the distribution

As highlighted earlier, an often “overlooked” expense is that of the withholding taxes on dividends. This might not be critical if the ETF you are focused on is not a high-yield one. The typical “index-hugging” ETFs such as the SPY has a yield of about 1.5-2%, translating to withholding tax costs of about 0.4-0.6%.

As the expense ratio is typically very low (less than 0.10%), the all-in cost (withholding tax + expense ratio) could be approx. 0.5-0.7% for these US-domiciled ETFs. That is still manageable, assuming that one engages a DIY approach to purchase these ETFs without additional fees (commission fees or advisory fees using Robos)

For higher yielding ETFs, the All-in recurring costs if one purchases a US-domiciled ETF could balloon to 1.3-1.4%.

In this scenario, to reduce the impact of withholding taxes, one could consider UCITS ETFs. However, these types of ETFs are not widely available on all brokerage platforms and can only be purchased on a selected few.

I will be dwelling more on the ideal brokerage platforms to select for the purchase of UCITS ETFs as well as some possible income strategies in my video guide.

How to purchase ETFs

There are 2 ways in which an investor can seek to invest in ETFs. 1) A DIY approach through many of the offline/online brokerages and 2) through Robo Advisors that invest in ETFs.

DIY Approach

The DIY approach comes with more flexibility and some cost savings. This is suitable for an investor who has an idea of what type of ETFs he/she wants to be vested in. The next step would be to select a brokerage platform that has extremely low/zero commission charges.

Ideally, the platform would also be able to provide a Regular Savings Plan option for these specially selected ETFs.

Unlike using a Robo Advisor where there will be advisory/platform fees incurred, the main fees involved on a DIY basis would be 1) Commission, 2) Expense Ratio and 3) Dividend withholding taxes

Robo Advisors

Many Robo Advisors here invest using ETFs as the core products. I have written a pretty comprehensive Beginner Guide to Robo Advisors in Singapore and readers can refer to that article for more information on their product offerings.

Investing using Robo Advisor is a more “hands-off” approach that is best suited for investors who have got no idea what ETFs to select.

All you have to do is to set your risk profile (whether you are a risk taker or a risk-averse person) and you leave it to the Robo Advisor to allocate what they believe are the right ETFs for you (combination of equity ETFs and bond ETFs).

For that convenience, you will have to pay an additional advisory fee which typically ranges from 0.6-0.8%/annum.

Hence, the All-In Costs when partaking in ETFs using a Robo Advisor would be 1) Advisory Fees, 2) Expense Ratio, and 3) Dividend Withholding Taxes.

This could all add up to be pretty significant.

Advisory fees (0.7%) + Expense Ratio (0.4%) + Dividend Withholding taxes (0.5%) = 1.6%

One way to reduce expenses in these circumstances is to look at a Robo Advisor offering such as from digiPortfolio (DBS bank), with its portfolio offering focused on SG-listed ETFs or UK-listed ETFs which does not incur dividend withholding tax on the Fund Level.

Best Singapore ETFs to invest in

For a Singaporean investor, he/she can engage a DIY approach to create a portfolio of Singapore ETFs to invest in.

I will highlight 4 ETFs that I believe are the best-in-class that an investor can purchase directly on the SGX while concurrently structuring a portfolio that is recession and inflation-proof.

These 4 ETFs can be broken down into 4 asset class categories:

- Equity

- Bonds

- REITs

- Commodities

My selection process is based on the NAOF portfolio structure (20% equity, 20% bond, 40% REITs, and 20% Gold) but one that is more localized for Singaporean investors. These ETFs also have to fulfill the criterion of high traded volume (on average more than S$1m worth traded each day).

The 4 ETFs that I have shortlisted to create a localized portfolio are:

- SPDR STI ETF – ES3 (Equity)

- ABF Singapore Bond Index Fund – A35 (Bond)

- Lion Phillip S-REIT ETF – CLR (REIT)

- SPDR Gold Shares ETF – O87 (Commodities)

This portfolio has a weighted average expense ratio of 0.42% and does not incur any dividend withholding tax.

For more information on setting up your localized portfolio of Singapore ETFs, one can refer to the article below:

Additional Reading: Best ETFs in Singapore to structure your inflation-proof passive portfolio

Conclusion

I hope that this Beginner Level Guide on ETF Investing provides you with the basic knowledge of what ETFs are all about, the benefits of investing in ETFs, and what are the key points to look out for when investing in ETFs.

I will be creating a video guide on how to partake in the various types of ETFs and the appropriate brokerage platforms or Robo Advisors to use in different circumstances.

The video guide will further touch on key salient areas such as thematic investing using ETFs, dividend investing using ETFs etc.

Do Like Me on Facebook if you enjoy reading the various investment and personal finance articles at New Academy of Finance. I do post interesting articles on FB from time to time that might not be covered here in this website.

Join our Discord channel for an active discussion on all things finance!

Join our Instagram channel for more tidbits on all things finance!

Join our Youtube channel for short and sweet videos on all things finance!

SEE OUR OTHER WRITE-UPS

- DIY OR ROBO? THE 1.6% OPPORTUNITY COST DILEMMA

- ULTIMATE ROBO ADVISOR SINGAPORE GUIDE

- CREATING THE BEST TAX EFFICIENT ETF PORTFOLIO TO INVEST IN?

- DIMENSIONAL FUNDS: ARE THEY WORTH THEIR WEIGHT IN GOLD?

- CHEAPEST WAY TO INVEST THROUGH RSP. SHOW ME HOW.

Disclosure: The accuracy of the material found in this article cannot be guaranteed. Past performance is not an assurance of future results. This article is not to be construed as a recommendation to Buy or Sell any shares or derivative products and is solely for reference only.