Robo Advisors Singapore

We know we have got to start investing. Problem is, we DON’T KNOW how to get started. That might be a problem in the past but it is no longer one with Robo Advisors coming into the picture.

What are Robo Advisors?

Robo advisors are digital platforms that use algorithms to automate your investment portfolios.

One can get started investing through a Robo Advisor pretty quickly. Your account can be set up in a matter of minutes. That is how convenient it can be.

When you sign up through the Robo online platform, all you need to do is input your risk profile (aggressive, conservative, balance, etc) and the Robo advisor will start to make a recommendation on your portfolio structure using their algorithm.

The next step is usually to fill in your particulars and provide a scanned copy of your IC as well as your banking and funding details. Once the funds are received by the Robo advisors, they will automatically invest them for you with periodic rebalancing. SIMPLE! (more details below).

For those looking for a quick example, I have written a Guide to Syfe and how to open an account in less than 10 minutes.

We present to you the ultimate Robo Advisors Singapore guide in this article. Do note that this is going to be a very long read, so have a cuppa coffee in hand.

This article was first published on 23 September 2019 and has been updated to include the latest information

Robo advisors Singapore advisory/management fees are typically 0%-1%, with many offering tiered pricing based on the amount invested.

The low-cost nature of Robo advisors, coupled with their low minimum initial investment requirement is what makes this an ideal platform for the man-in-the-street to get started on their investment journey.

What are these Robo advisors investing in?

The majority of Robo advisors in Singapore use Exchange Traded Funds (ETFs) as their investment platform. An ETF is a basket of investments, including stocks, commodities, bonds, etc that trade on an exchange, just like a stock. ETFs are generally passive and track a particular index/theme.

The advantage of buying an ETF vs. individual stocks can at times be summarized as having a diversified exposure at a low cost (total expense ratio is typically around 0.4%)

However, as can be seen, some Robo advisors invest in funds as well as a hybrid of stocks/ETFs. Typically, funds tend to have a higher total expense ratio (TER) as compared to ETFs due to the former’s active management nature.

Find out what are the fund management fees

Hence this is an area to pay attention to when investing in a Robo advisor.

Total charges = 1) Robo advisor’s management fee + 2) ETF/Fund management fee (usually not actively disclosed)

It would hence be erroneous to evaluate the fee structure of Robo advisors based on just their management/advisory fee structure and conclude that one platform is cheaper than the other.

We will need to understand their underlying investment platform (ETFs, funds, stocks, etc) and assess the expense nature of investing in these asset classes as well.

We will be providing an analysis of the individual Robo advisors base on their fee structure as well as their underlying investment platform.

But first, let’s start with some of the basics….

What happens when one wishes to invest with a Robo advisor?

In the first step, Robo advisors will construct a portfolio for you based on a few key variables such as your goals, investment horizon, risk profile, financial situation, etc.

In the second step, the investor will be allocated to one of the Robo advisor’s portfolio based on the investor’s investment profile.

In the third step, the investor can then fund the account through a lump sum investment or monthly recurring investment, similar to a regular savings plan.

In the fourth step, the Robo advisors will periodically re-balance the portfolio if required. You can easily monitor the performance of the portfolio on the spot.

Pros vs. Cons of a Robo advisor

PROS

We list down some of the benefits of Robo advisors which we think matter to investors the most. We highlight the 4 key BENEFITS of using a Robo advisor that investors should be aware of, in our view.

#Key benefit 1: Lower fees

As explained, Robo advisors typically have much lower advisory fees compared to a typical mutual fund. Robo advisor fees range from zero (less than SGD50,000 invested in Kristal.AI) to about 1.0% (SGD10,000 or less invested with Smartly).

This is compared to mutual funds that typically charge advisory fees easily in excess of 1.0%, at times trending towards the 2%-3% range. Even after including ETFs management charges, some of the more price-competitive Robo advisors still have all-in charges less than 1.0%.

#Key benefit 2: personalized diversified portfolio at a low buy-in fee

Typically to create your own personalized portfolio, that will require a substantial initial investment amount that is out-of-reach for most beginner investors. We see one of the key benefits of a Robo advisor as to the ability to create a personalized portfolio based on the risk profile of an individual.

This is also done at a fraction of a cost (low minimum investment sum) compared to typical mutual or institutional funds where the minimum sum could trend to the millions.

Not only does one get introduced to a personalized portfolio suitable to his/her risk profile, but the investments also tend to be diversified across asset classes (equities, bonds, commodities). This is an advantage over simply investing in a single asset-class ETF/stock.

#Key benefit 3: constant rebalancing to maintain ideal return/risk profile

We see the ability of Robo advisors to provide constant rebalancing of your portfolio to maintain your targeted asset class mix (eg: 60% equity/ 40% bond) as one of the key benefits.

While one could create their own “personalized” portfolio without the need of Robo advisors (use 60% of your available funds to buy equity-related products and 40% to buy bond-related products) periodic re-balancing will become a hassle on a DIY basis.

Robo advisors provide an automated basis for such re-balancing work to be done on a periodic basis. This is a much simpler process compared to manually re-balancing your own portfolio.

#Key benefit 4: ease of account setting and fund transfer

The complicated account set-up process is often the key hurdle for the novice investor to get themselves started on their investment journey. Setting up a Robo advisor account is pretty simple and straight-forward, with no requirement for document submission.

You can simply sign up online by creating your online account and transfer the funds seamlessly from your bank account to your investment account.

CONS

We list down some of the cons of Robo advisors which we think matters to investors the most. We highlight the 3 key DOWNSIDES of using a Robo advisor that investors should be aware, in our view.

#Key downside 1: Limited scope for personalization in most cases

Most of the Robo advisors are algorithm-driven, hence portfolio customization is limited at best and cannot deviate significantly from the algorithm’s parameters.

If you are a savvy investor who wishes to choose your own securities or ETFs, there are limited options. Kristal.AI is, however, one such Robo advisor that allows you to customize your own portfolio based on certain thematic ETFs.

#Key downside 2: currency fees and dividend taxes

Besides the typical advisory fees charged by the Robo advisors themselves as well as management fees incurred by the management of the ETFs, hidden fees such as currency conversion fees could eat into the returns of your portfolio.

Most of the Robo advisors invest in USD denominated ETFs. A significant depreciation of the USD against SGD will negatively impact the returns of a Singapore-based investor.

There are also withholding taxes incurred on the investor level for dividend/income funds that are domiciled in the US. This will further reduce the net returns of your bond portfolio. There are however certain exceptions for funds under the Qualified Interest Income (QII) rule which do not incur dividend withholding tax. These are generally the bond funds/ETFs such as the US Government Bond ETF, 20+ Year Treasury Bond (TLT), etc.

#Key downside 3: recurring fees from AUM

Despite the low-cost nature of Robo advisors, recurring fees will be incurred for AUM. One would have to question if such recurring expenses accruing to the Robo advisors are justified vs. a DIY approach.

Most beginning investors will, however, lack the knowledge or time to create and monitor the performance of their portfolio. Hence, despite the recurring fees of Robo advisors, it might still be a worthwhile proposition to use one.

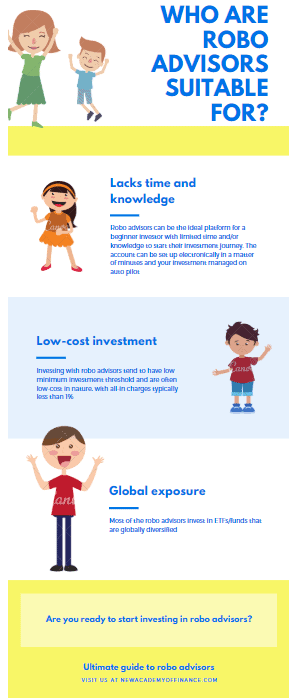

Who are Robo advisors suitable for?

#Ideal Investor 1: Someone who lacks the time and/or knowledge to manage his/her own portfolio

For someone who does not have the time and/or knowledge to create their own investment portfolio, Robo advisors will be the ideal platform to kick-start their passive investment journey.

The investment account can be set up electronically in a matter of minutes and with a click of the button, the algorithms will do the heavy lifting of investing your money.

There is no need for active management and you can monitor and track the performance of your portfolio easily through the platform at any point in time.

#Ideal Investor 2: Someone looking for a low-cost investment

Investing in Robo advisors tend to have low minimum investment threshold. More importantly, they are often low-cost in nature with all-in fees typically within the 1% region.

What you get by paying 1%/annum could at times be a dedicated investment specialist allocated to your account as well as a diversified portfolio of different asset classes that are re-balance periodically to ensure the best risk-adjusted return.

#Ideal Investor 3: Someone looking for global exposure

Most investors tend to be heavily weighted on investments from their home nation. This tends to create a geographic-centric risk that can be diversified away through a Robo advisor, which could adopt an investment strategy of geographical diversification.

Most of the Robo advisors invest in ETFs/funds that are globally diversified which might be an attractive feature for a Singapore-based investor who is currently heavily-weighted on Singapore-listed equities, for example.

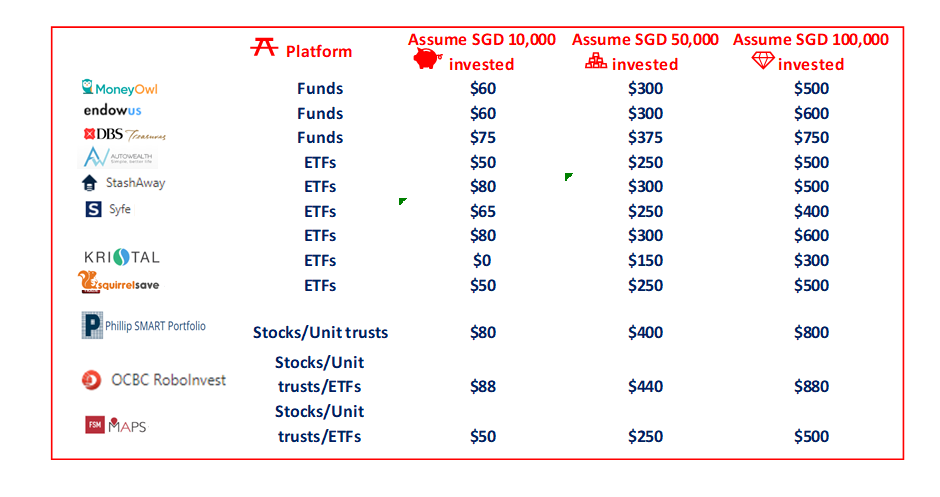

Ultimate Robo Advisors Singapore Guide

The table above shows the typical annual management fee structure of the various Robo Advisors based on the amount invested.

For a small account < $10,000, the most cost-effective Robo Advisor would be Kristal, with Autowealth, Squirrelsave, and FSM MAPS tied for second place.

For a large account > $100,000, the most cost-effective Robo Advisor would still be Kristal, with Syfe coming in 2nd place.

Robo Advisors Singapore which invests in Funds

Typically, we tend to shun Robo advisors investing directly in funds due to the higher expense ratios associated with investing in funds vs. ETFs. However, there are exceptions as seen from our analysis below.

#1 MoneyOwl

Launched in 2019, MoneyOwl is a joint venture between Providend and NTUC Enterprise. MoneyOwl offers “bionic” advice through a combination of humans and robots to deliver low-cost investment solutions with a human touch.

Portfolios offered:

- Dimensional portfolio

- WiseIncome

- WiseSaver (cash management)

Dimensional Portfolios

Under its Dimensional portfolio offering, it is further segregated into 5 portfolios: 1) Equity, 2) Growth, 3) Balanced, 4) Moderate, and 5) Conservative. Based on how aggressive or conservative one is, there will be different compositions of asset classes. For example, an Equity portfolio will be 100% vested into an equity fund while a Growth portfolio will have some components of fixed income allocated (10%) to it.

MoneyOwl invests in 4 broad Dimensional Funds:

- Dimensional Global Core Equity Fund (SGD, Accumulation) – Developed market stock fund

- Dimensional Emerging Market Large Caps Core Equity Fund (SGD, Accumulation) – Emerging market stock fund

- Dimensional Global Short Fixed Income Fund (SGD Accumulation, Hedged) – Invests in short-term high-quality bonds globally.

- Dimensional Global Core Fixed Income Fund (SGD, Accumulation, Hedged) – Invests in high-quality bonds globally

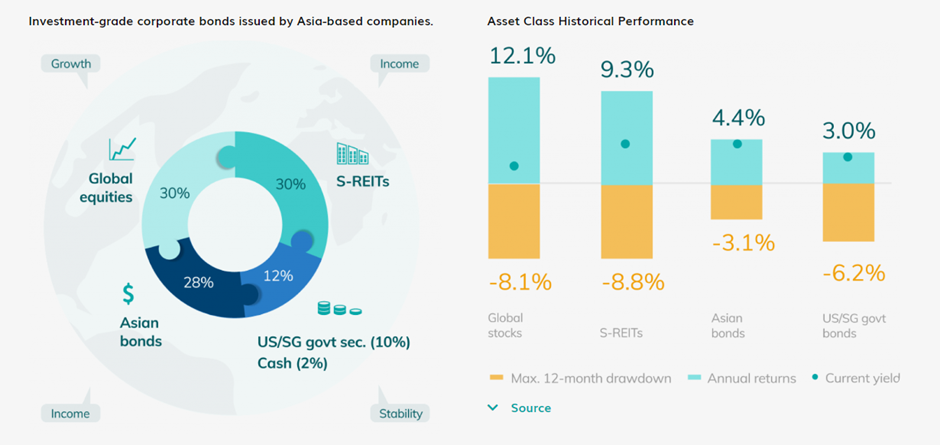

WiseIncome Portfolio

Invest in a combination of 4 asset types: 1) Global Equities, Asian Bonds, S-REITs, and US/SG government securities. One can start investing in WiseIncome with a minimum capital of $1,000, with either cash or SRS.

This is more of an income portfolio for investors who prefer to generate cash flow from their investments. This can be used to complement your payouts from your CPF LIFE in your golden years.

WiseSaver Portfolio

This is MoneyOwl’s cash management portfolio offering returns of around 2.61% as of 16 Sep 2022. Do note that capital is not protected over here although the risk is relatively low since most of the capital is invested in SGD bank deposits by local financial institutions with short-term investment-grade ratings.

One can also park his/her SRS monies into WiseSaver to generate the higher returns offered from its cash management service vs. 0% if left in one’s SRS account.

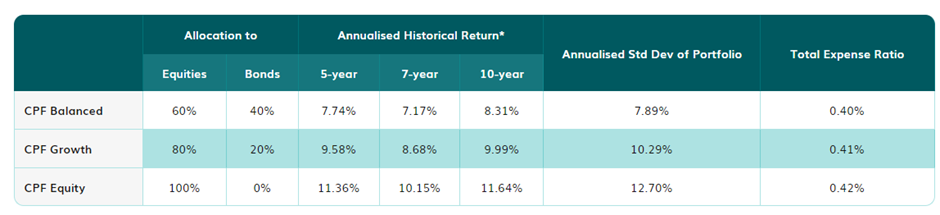

MoneyOwl’s CPF portfolio

This is something NEW offered by MoneyOwl. Previously, only Endowus offered the solution of allowing Singaporeans to invest their CPF OA funds.

CPF portfolios are categorized as such 1) CPF Balanced, 2) CPF growth, and CPF Equity and are invested into just 2 asset categories: Equities and Bonds

The equity component is vested through LionGlobal Infinity Global Stock Index Fund Share Class C and the bond component is vested through UOBAM United SGD Fund Share Class D.

Fee Structure

- Dimensional Portfolio:

0.6% per annum (up to $100,000)

0.5% per annum (Above $100,000)

- WiseIncome Portfolio:

0.6% per annum (up to $100,000)

0.5% per annum (Above $100,000)

WiseSaver Portfolio: 0%

CPF Portfolio: 0% (for 2022)

According to them, the fund TER amounts to a manageable 0.4% which brings total charges to around 1%. The low management fees of the Dimensional funds, as opposed to other more actively managed funds, is a key differentiating factor here that allows MoneyOwl to remain competitive vs. other Robo advisors. MoneyOwl’s low minimum initial investment amount of SGD100 with an option for an SGD50/month regular saving plan is ideal for the regular man in the street to kick start their investment journey.

#2 Endowus

Endowus is a Singapore-based investment platform that enables people to invest their CPF, SRS, and cash savings better at the lowest cost possible. This fee-only firm invests in institutional share classes of funds, where management fees are significantly lower.

Portfolios offered

- Endowus Core

- Endowus Income

- Endowus Satellite

- Endowus Cash Smart (Cash Management account)

- Endowus Fund Smart

- Private Wealth

These portfolios are vested into funds offered by global investment management companies such as Dimensional Fund, PIMCO, First State Investments, Eastspring Investments, Vanguard, Schroders, and others.

When you create an Endowus account, they will create a trust account in your name at UOB Kay Hian. This trust account will handle your assets and process the transactions you make on the Endowus platform.

Investing using CPF and SRS monies

The ability to use our CPF funds to invest is a major advantage that this platform has over the rest (except for MoneyOwl), in our view. However, investing one’s CPF using Endowus platform is more costly at 0.4%/annum for advisory fee vs. MoneyOwl’s current 0% fee structure

Endowus Fund Smart

This is an offering that allows a user to create his/her portfolio consisting of the various funds offered by Endowus. Investors can choose from a list of more than 150 funds. However, do note that the TER for these funds might not be cheap and that adds up to the overall recurring costs that investors might be paying.

Endowus Cash Smart

This is Endowus cash management feature. While it is marketed as allowing an investor to park excess cash and earn up to 3.8% per annum in yield, do note that capital is NOT protected, and to generate higher returns, a greater risk is typically involved.

I did not have that good an experience with their cash smart offering, with my capital down approx. 2% due to some of their holdings with China bond exposure.

Fee Structure

- 0.25% to 0.6% for investing in Endowus Core, Income, and Satellite Portfolios)

- 0.4% for investing CPF and SRS in Endowus Core, Income, and Satellite)

- 0.3% for investing cash, CPF, and SRS in Fund Smart

- 0.05% for investing cash and SRS in Cash Smart

Robo Advisors Singapore which invests in ETFs

#3 DBS digiPortfolio

DBS digiPortfolio used to be only available for DBS Treasures clients who have assets under management of SGD350,000 and above. However, DBS subsequently announced that it will be extending its DBS digiPortfolio to retail investors with a multi-currency account through the launch of two portfolios comprising Singapore and UK-listed ETFs.

Portfolios:

- Asia Portfolio

- Global Portfolio

The Asia Portfolio (SG-based ETFs) has a minimum investment sum of SGD1,000 while investors seeking global diversification can opt for the Global Portfolio (which offers UK-listed ETFs) for a minimum investment sum of USD1,000.

However, since the Global Portfolio is classified as a Specified Investment Product (SIP) and denominated in USD, investors must be willing to take on currency risk and must pass a Customer Account Review.

Unlike the offering for Treasures clients which invest in funds, the retail offering is ETFs-based digiPortfolios, but with a limited scope of SGX or UK-listed ETFs, with a collection of four to seven ETFs in total that represent between 200 and 13,000 holdings in a single transaction.

Additional benefits with DBS Multiplier Account

When you invest with DBS digiPortfolio, you can boost your interest return on your cash holdings in your DBS Multiplier Account up to 3.5%.

Lower withholding tax structure

In terms of global exposure, this DBS digiPortfolio offering for retail investors is likely at a disadvantage, given that its global exposure is only limited to a small array of UK-listed ETFs.

This could be due to tax-related purposes. UK-listed ETFs have lower withholding tax for a Singapore investor vs. US-domiciled ETFs

Most of the Robo advisors in Singapore invest in ETFs as their key investment platform, not surprising given the low-cost nature of ETF investing, which is as easily tradable as a stock.

Some ETFs such as the Vanguard ETF VOO have an expense ratio of only 0.04%, making this investment the ideal tool to track the S&P500 index. However, that excludes dividend tax withholding costs which can become rather substantial.

Fee Structure

In terms of fees, the advisory fees amount to 0.75%. A typical Singapore ETF such as the Nikko AM STE ETF which tracks the Straits Times Index (STI) has an expense ratio of 0.35%. This brings total charges to approx. 1.1%, again pretty similar to both MoneyOwl and Endowus.

#4 AutoWealth

AutoWealth is one of the pioneers of Robo advisors in Singapore, first started in 2015. Like MoneyOwl, AutoWealth has a wealth manager that is assigned to each client, hence having that bionic or hybrid touch that might be an advantage over an all Robo-only advisor (as long as we are not paying higher fees for it).

Portfolios:

- Preservation (20% equities/80% bonds)

- Conservative (40% equities/60% bonds)

- Balanced (60% equities/40% bonds)

- Long-term Growth (80% equities/20% bonds)

AutoWealth engages a passive market-returns portfolio investment approach, with essentially a two-fund portfolio. One comprising of Global Equity (MSCI Index) and the other Global Government (US + International) bonds at your desired allocation based on your risk profile to create the 4 portfolios shown above.

In terms of investing in global equity assets, AutoWealth typically invests in extremely low-cost ETFs such as Vanguard Total Stock market ETF (VTI) with 0.04% expense, Vanguard FTSE Europe ETF (VGK) with 0.10% expense, etc. On the bond side, some of the ETFs used are iShares 7-10 Year Treasury Bond ETF (IEF) with 0.15% expenses.

Passive investment style

Autowealth is likely one of the only Robo Advisors that maintain its passive investment style without many options for customization. This is both good and bad.

Good in the sense that it keeps everything super simple. One will need to just select the appropriate portfolio according to his/her risk profile and invest in equities and bonds based on the allocated ratios.

Bad in the sense it lacks customization features that more advanced investors might appreciate. However, for beginner investors who wish to keep everything simple, this might just be the kind of Robo Advisor for you.

Segregated account

Unlike some Robo advisors which pool investors’ money and invests them as a whole, AutoWealth will require investors to open a separate Saxo Capital Markets account (custodian) where client assets are held in legally segregated accounts under their name.

This means that only you have any legal claims on all your assets in all circumstances.

Fee Structure

Autowealth charges a flat advisory fee of 0.5%/annum plus USD$18 in platform fees/annum.

Coupled with its super low expense ratio for ETFs in which it is invested in, the total charges will likely be approx. 0.7%-0.8%, on our estimate, a very competitive amount compared to some of the Robo advisors which we have previously highlighted.

However, this excludes any dividend withholding tax impact.

#5 StashAway

StashAway was started back in 2016 by ex Zalora Group CEO, Michele Ferrario. The company employs a proprietary investment strategy called the Economic Regime-based Asset Allocation (ERAA) which continually monitors economic and market cycles to re-balance accordingly.

The Robo Advisor deploys a trust account with DBS and uses custodial accounts through Saxo.

Portfolios:

- General Investing

- General Investing by StashAway

- General Investing by BlackRock

- ESG Investing

- Thematic Portfolios

- Flexible Portfolio

- Income Portfolio

- StashAway Simple (Cash management)

- StashAway Reserve (Accredited investors)

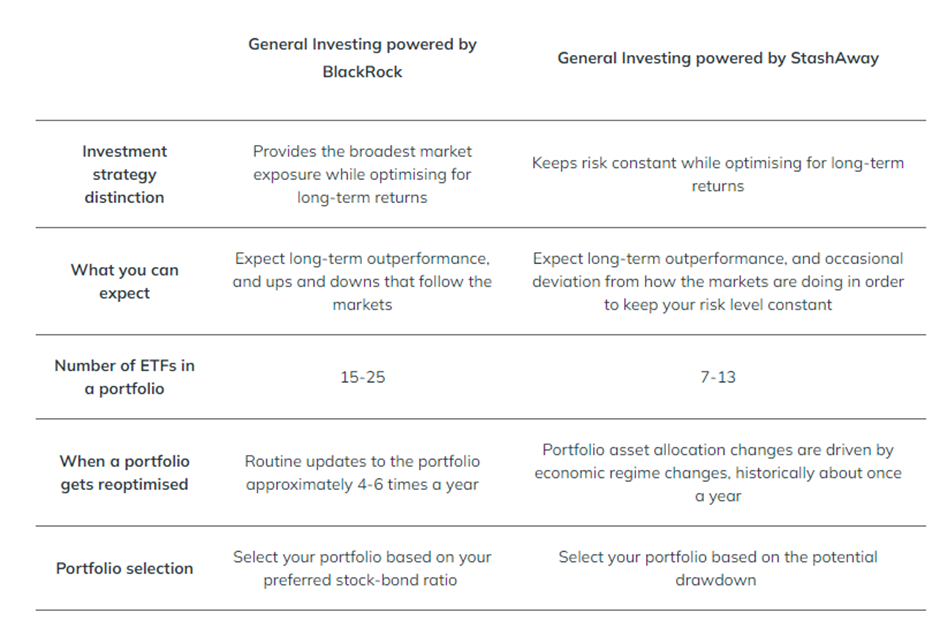

General Investing

StashAway recently introduced its General Investing concept, which is anchored by its ERAA strategy that is based on a risk approach (how your portfolio is allocated to the different assets is based on how much drawdown you are willing to accept for your portfolio).

It also introduced General Investing powered by Blackrock which enables investors to leverage insights and asset allocation guidance by BlackRock based on 4 risk levels.

There is also Responsible Investing with ESG that is based on its ERAA approach, investing in ETFs with high ESG scores.

For the full list of ETFs that these portfolios are vested in, please refer to the link here.

Thematic & Flexible Portfolios

Beyond its standard General Investing offering, StashAway is now also offering Thematic and Flexible Portfolios.

There are currently 4 thematic portfolios offered by StashAway. 1) Technology Enablers, 2) The Future of Consumer Tech, 3) Healthcare Innovation, and 4) Environment and Cleantech

StashAway recognizes that thematic investing can be of a high-risk nature, hence instead of deploying 100% of the capital into the specific basket of thematic ETFs, they reduce the risk for investors using balancing assets. So assuming you have a conservative risk profile but still wish to invest in their Healthcare Innovation Theme, 30% of capital will be allocated to the relevant ETFs in this particular theme, while the remaining 70% will be vested into balancing assets which are investments not related to that theme (for example government bonds, etc).

Its Flexible Portfolio allows investors to customize their portfolios based on 55 curated ETFs. The list is rather small in my view compared to other customized offerings such as those provided by Syfe.

Income Portfolio

Similar to MoneyOwl WiseIncome portfolio, this portfolio is focused on generating cash flow for investors. Most of the income ETFs are SG based and similar to WiseIncome, it allows one to reinvest the dividends to compound them over a longer horizon or to withdraw it to pay for daily expenses.

Do note that while other portfolios do not have a minimum investment amount, the Income Portfolio will require a minimum investment amount of $10,000.

StashAway Simple/Simple Plus

Like some of the more established Robo Advisors in this list, StashAway also offers its users cash management services.

Offering yields of 2.1% for its more conservative Simple cash management portfolio to 3.6-4.1% for its higher risk Simple Plus cash management portfolio.

Do note again that these cash management services are not capital protected and investors opting for the higher yielding solutions could see a drawdown in their portfolio capital.

My advice is to stick to the fuss-free Simple offering at a lower yield of 2.1% if investors do not wish to see any capital risks.

Additional Reading: StashAway Simple. Can you really generate 1.9% return?

SRS Investing

Similar to Endowus and MoneyOwl, StashAway offers SRS Investing (not CPF Investing) which allows one to use their SRS funds to vest in most of the portfolios offered by StashAway (General Investing, Thematic portfolios, and Income portfolios)

Fee Structure

Goal Based & Income Portfolio

First $25,000 – 0.8%

$25,000 to $50,000 – 0.7%

$50,000 to $100,000 – 0.6%

$100,000 to $250,000 – 0.5%

$250,000 to $500,000 – 0.4%

$500,000 to $1m – 0.3%

More than $1m – 0.2%

StashAway Simple – 0%

StashAway advisory fees for beginner investors with funds less than $25,000 is on the high side at 0.8%. Coupled with the expense ratios of the funds in which they are invested, which StashAway guided to be in the 0.2% region, the All-In costs could be around the 1% mark.

However, I do think the 0.2% average expense ratio for funds they are vested in is on the low side. For those seeking Flexible portfolios to invest in their curated list of 55+ ETFs, many of these ETFs have expense ratios above 0.5%.

#6 Syfe

Syfe is one of the latest digital wealth managers launched in July 2019 after raising SGD5.2m in seed funding. Funds in Syfe are held in a Trust Account with DBS Bank while investments are held in a Custodian Account through Saxo Capital.

The Robo advisor uses Automated Risk-managed Investments (ARI) strategy which automatically adjusts your portfolio to ensure enhanced risk-adjusted returns by managing your portfolio’s downside risk.

I have written quite several article reviews on Syfe, so if you are interested, do check out the links below.

Additional Reading: Syfe Select Review. Should you be investing in it?

Additional Reading: Syfe Equity100 review. Does this portfolio make sense to you

Portfolios:

- Core Portfolio

- Core Equity 100

- Core Growth

- Core Balanced

- Core Defensive

- Satellite Portfolio

- REIT +

- Themes

- ESG & Clean Energy

- Disruptive Technology

- Healthcare Innovation

- China Growth

- Global Income

- Custom Portfolio

- Fractional Investing

- Cash+ (cash management)

Core Portfolio

This is Syfe generic Robo Advisor offering where investors can invest in a portfolio that suits their risk profile and this is vested based on their ARI strategy.

To be honest, a pretty standard Robo advisory offering.

REIT+

This is where Syfe differentiates itself from the other Robo Advisory offerings. While other Robo Advisors such as those mentioned above do offer income-related portfolios, there are typically 2 layers of fees associated with them.

The first layer is the product fees (expense ratios, trust fees, etc) which can be in the region of about 0.4% and the second layer is the platform’s advisory fees which can in the region of 0.5-0.8% thereabout. Other miscellaneous fees that could be significant are the withholding taxes associated with overseas yielding assets.

As Syfe invests directly into individual REIT counters for its REIT+ portfolio, there is no first layer of charges and investors looking at high-yielding offerings only need to pay its advisory fee of 0.65% for portfolio amount < $20,000.

Thematic Portfolio

Similar to StashAway, Syfe offers a range of thematic portfolios around 1) ESG & Clean Energy, 2) Disruptive technology, 3) Healthcare Innovation, 4) China Growth and 5) Global Income.

However, there is no balancing asset feature here and hence the risk level and consequently the potential returns are higher in this case.

Custom Portfolio

Syfe’s custom portfolio has double the number of ETF holdings available for clients to select from vs. StashAway.

However, do note that the expense ratios can be relatively high over here.

Cash+ Portfolio

Syfe’s cash+ portfolio is not very exciting from the angle of its yield offering (currently at 1.9%). But that also means it is not vested into high-risk assets that could result in capital losses. The 2 funds that Cash+ is vested in are LionGlobal SGD Enhanced Liquidity Fund SGD (70%) and LionGlobal SGD Money Market Fund (30%).

There is no minimum amount for investors to start investing with Syfe. The Robo advisor charges 0.4-0.65% in advisory fees which gives you unlimited, free withdrawals and unlimited rebalancing. With ETF fees estimated at 0.15%, that brings all-in charges to approx. 0.80%.

Fractional Investing for US shares

One of the few (or perhaps only) Robo Advisor that has fractional investing solution, Syfe has evolved into an online brokerage with its Syfe Trade function that allows its clients to partake in fractional investing.

Fractional investing is where an investor can purchase < 1 share of a counter. This is very useful for beginner investors who do not have a large capital on hand to deploy.

Syfe also offers an automated dollar cost averaging feature for US stocks which is again an easy and disciplined manner for a user to start his investing journey.

Fee Structure

$20,000 and below – 0.65%

Above $20,000 – 0.5%

Above $100,000 – 0.4%

Above $500,000 – 0.35%

Syfe’s advisory fee structure is rather competitive. Including the expense ratios for its Core portfolios which Syfe guides to be around 0.15 – 0.24%, the overall annual recurring fees amount to about 0.8-0.9% which is pretty decent

#7 UTrade Robo

UTrade Robo invests in multi assets, including stocks, bonds, and commodities. It uses the Modern Portfolio Theory to allocate among asset classes to determine the maximum expected returns for a given level of risk.

Portfolios:

- Global Multi-Asset Portfolio

The Robo advisors look at ETF selections that are London-listed or Ireland-domiciled ETFs which are not subject to withholding tax at the investor level. This is similar to the DBS digiPortfolio structure that invests in mainly SGX-listed and London-listed ETFs to likely avoid the payment of withholding tax at the investor level.

Fee Structure

$50,000 and below – 0.88%

Above $50,000 – 0.68%

Above $100,000 – 0.5%

UTrade Robo has a minimum investment amount of SGD5,000 and min subsequent top-ups of $500 and their advisory fees range from 0.5% to 0.88%. Most retail investors will likely have to pay the top-end of the advisory fees of 0.88%. Add in the typical fund expense ratios of 0.13% – 0.40% and total costs could be at least 1.0%-1.4% which is on the high-end of Robo advisor charges.

#8 Kristal.AI

Kristal.AI’s proprietary AI uses an underlying genetic algorithm to choose and modify strategies from a pool of thousands of permutations. At each stage, the curated strategies are tested against user-defined objectives with only the “fittest’ strategies chosen into a risk-limiting model which optimizes asset allocation and maximizes returns.

Portfolios

- Kristal Freedom

Kristal Freedom

According to its website, Kristal only provides the Freedom portfolio for retail investors. Private Wealth solutions are available for accredited investors.

However, there aren’t many details about its freedom portfolio, with Kristal highlighting it is a digital advisory service with clients having access to thematic investments and automated portfolios.

Its thematic investments are likely vested in a selected pool of ETFs that Kristal has pre-screened. Clients can then engage in automated invested based on the different risk profiles available: 1) High Growth, 2) Growth, 3) Secure, 4) Balanced and 5) All-Weather US

The relevant ETFs tagged to the 3 key asset classes: 1) Fixed income, 2) Equities, and 3) Commodities are vested in different ratios based on your selected risk profile.

Fee Structure

Less than US$10,000 – 0%

More than US$10,000 – 0.3%

Kristal.AI stands out as the Robo advisor with the lowest management fees among its peers with no management fees for accounts of less than USD10,000. That in itself is a significant cost-savings of at least 0.5% which is the normal advisory fee for most Robo advisors.

No minimum investment amount is required.

While Kristal stands out as being the lowest cost Robo Advisory service in our list, it does seem like its target clientele is geared towards the high-net-worth, accredited investors with offers like fractional bond offerings, Pre-IPO deals, etc.

Not many details are available concerning the type of ETFs it is vested in and their associated expense ratios.

#9 SquirrelSave

SquirrelSave is a fully AI-driven investment service offered by PIVOT Fintech, a Singapore-based technology company regulated by the MAS.

An investor will first input its risk level and SquirrelSave will subsequently trawl over 2,000 diversified ETFs to design a personalized portfolio comprising a few selected ETFs whose combined risk prediction matches your chosen risk and gives the highest predicted return for the time horizon.

The minimum investment amount is $1

Portfolios:

- Conservative – You prefer to minimize risk and preserve capital

- Balanced – You value capital preservation but are willing to accept some risk for long-term asset appreciation

- Growth – You are willing to accept capital risk for higher long-term returns

- Aggressive – You are willing to accept high risks to achieve higher returns

- Very Aggressive – You believe that high risks bring potentially higher returns

These portfolios are vested into ETFs which cover developed and emerging equities, fixed income, commodities, and currencies.

Fee Structure

$0-$500,000 – 0.5%

In addition to its advisory fees, there are additional fees which consist of a 10% performance fee based on a “high-watermark” area.

These fees could be rather substantial and eat into the returns of an investor. Usually, such performance fees are only reserved for hedge funds, hence I am rather surprised that SquirrelSave has this component as part of its fee structure.

#10 SaxoWealthCare

Similar to most Robo Advisors, Saxo offers a core set of portfolios based on the client’s risk profile. The platform also allows for multiple goal settings and regular investment contributions for the investor to reach their target goal.

There is a minimum investment amount of $3,000

Portfolios:

- Global Growth

- Asian Growth

- Sustainable Growth

These portfolios invest in a combination of stock and bond ETFs.

Portfolio Protector

A unique element is its portfolio protector function. This acts as an additional safeguard against market volatility and will be activated when the portfolio value drops to a pre-set threshold. One’s portfolio will be automatically switched to a minimal-risk structure with a higher bond allocation.

Fee Structure

First $50,000 – 0.75%

$50,000 to $100,000 – 0.7%

$100,000 to $800,000 – 0.6%

$800,000 – $1m – 0.55%

Above $1m – 0.45%

Saxo highlights that its product fees range from 0.17% to 0.45% which brings the all-in cost to possibly be as high as 1.2% for the retail investors. This can be quite substantial.

Robo Advisors Singapore which invests in Unit trusts/stocks/ETFs

Some Robo advisors engage in a hybrid of assets beyond just ETFs but also using alternative investment funds etc which might increase the overall fee charges.

Unless there is a huge value proposition for such a platform, if not we believe that the total costs associated with such hybrids might not justify the returns associated with them.

#11 Phillip SMART Portfolio

Phillip SMART Portfolio uses a hybrid approach in its investment methodology. Its proprietary SMART algorithm was created in-house by the Principal Data Scientist to digest more than 1,000 data points daily. These data are then provided to their Chief Investment Officer and Investment team who will then use their wealth of industry experience and expertise to make the final decisions for the portfolios.

For their General Investing portfolios into Unit Trusts, the minimum amount to get started is S$300 while investing into its Growth portfolio consisting of US Equity will require a minimum investment of S$3,000.

Portfolios:

- Phillip Smart Portfolio

- Income

- Income & Growth

- Growth (Unit Trusts)

- Growth (Stocks)

Phillip Smart Portfolios

Phillip Smart Portfolios will be built according to the various risk profiles: 1) Low Risk to Income Portfolio, 2) Moderate Aggressive to Income & Growth Portfolio and 3) Aggressive to Growth Portfolio

Its portfolios are mainly invested in unit trusts, similar to the likes of MoneyOwl and Endowus. However, there aren’t many details as to what are the types of Unit trusts the Robo Advisor is vested in nor their associated costs.

For its growth portfolio which vests directly into US stocks, there is a minimum requirement of $3,000 to get started.

Fee Structure

0.5% – General Investing through Unit Trusts

0.8% – Growth investing through stocks

While Growth investing through stocks has a higher associated advisory fee, it does not come with the added product-related fees associated with Unit trusts. So All In costs for Phillip Smart Portfolios will be rather competitive below 1%.

#12 OCBC RoboInvest

OCBC RoboInvest was launched in August 2018, making it the first bank in Singapore to offer a Robo advisory solution.

Investors will have access to 37 thematic portfolios, specially curated by OCBC’s wealth experts. There will be automated portfolio monitoring and re-balancing on a quarterly or biannual basis.

The Robo advisors invest in predominantly ETFs but there could be occasions where there could be a combination of both ETFs and equities. Investors can choose ETFs that are geographic-centric, such as focusing only on Singapore-themed ETFs over US-based ETFs to avoid exchange-related fees.

Depending on the type of portfolio, the minimum required sum to get started is also different.

Portfolio:

- 37 thematic portfolios across 6 markets

Fee Structure

OCBC RoboInvest has the highest advisory fees among all the Robo advisors in Singapore at a flat 0.88% across all investment amounts. Adding in ETFs management fees and we are probably looking at all-in charges of approx. 1.2% or higher

There are also other fees such as Exchange Fees & charges where applicable. For example, if you trade in the Hong Kong market, there’s a stamp duty of 0.1% of the contract value and an exchange fee of 0.077% of the contract value.

#13 FSM Maps

Similar to Phillips SMART Portfolio, FSM Maps is not driven by an algorithm but managed by a team of managers and research analysts. It offers 10 portfolios with either Income or Growth objectives that are dependent on your risk profile. The portfolio may invest in balanced funds, alternative investment funds, money market funds, and ETFs.

There is a minimum requirement of $100 to get started on its Regular Savings Plans and $500 for lump sum investing.

Portfolios:

- Income

- Conservative

- Moderately Conservative

- Balanced

- Moderately Aggressive

- Aggressive

- Growth

- Conservative

- Moderately Conservative

- Balanced

- Moderately Aggressive

- Aggressive

Fee Structure

An advisory fee of 0.35%-0.5% is levied on the investments. Investors also have to fork out a transaction charge of 0.04% as well as the relevant SGX clearing and Trading fees, including GST for ETF transactions. All-in charges could amount to the region of 1.0%, based on our estimate.

Conclusion

Unfortunately, there is no Robo advisor at present that ticks all the right boxes. Our ideal Robo advisor will be one with:

All-in charges of approx. 0.8%/annum. We want a low-cost investment platform that does not eat into our returns.

Provide a cheap RSP solution. The purpose of a Robo Advisor should be a fuss-free, cheap + automated solution for a newbie investor who probably also has a limited amount of capital to get started on his/her investment journey. A low minimum investment barrier will be ideal. Concurrently, the option to invest a small amount every month on an automated basis will be welcomed as well.

A greater degree of customization. We want to have the option of choosing between a purely passive investment route like AutoWealth but yet also has customization features like that of Syfe which allows for thematic investing for more advanced investors.

Ability to invest using CPF and SRS funds. Currently, only a few Robo advisors have the option of investing using SRS funds while MoneyOwl and Endowus are the two Robo advisors to get approval for investments using CPF funds.

In a separate video guide which I will provide shortly, I will offer my assessments as to which are my preferred Robo Advisors to use in Singapore. So do look out for that upcoming Robo Advisor video guide.

Do Like Me on Facebook if you enjoy reading the various investment and personal finance articles at New Academy of Finance. I do post interesting articles on FB from time to time that might not be covered here in this website.

Join our Discord channel for an active discussion on all things finance!

Join our Instagram channel for more tidbits on all things finance!

Join our Youtube channel for short and sweet videos on all things finance!

SEE OUR OTHER WRITE-UPS

- DIY OR ROBO? THE 1.6% OPPORTUNITY COST DILEMMA

- CREATING THE BEST TAX EFFICIENT ETF PORTFOLIO TO INVEST IN?

- DIMENSIONAL FUNDS: ARE THEY WORTH THEIR WEIGHT IN GOLD?

- CHEAPEST WAY TO INVEST THROUGH RSP. SHOW ME HOW.

Disclosure: The accuracy of the material found in this article cannot be guaranteed. Past performance is not an assurance of future results. This article is not to be construed as a recommendation to Buy or Sell any shares or derivative products and is solely for reference only.