JP Morgan recently came out with a Singapore Property sector report which I like to share some of the key salient points with everyone. You can find the PDF report at the end of this article.

Following that, I will like to also share an article from Stuart Chng on whether to buy or not to buy a property during this period.

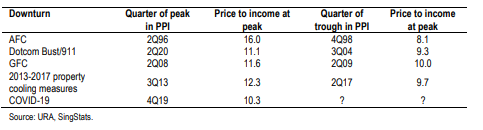

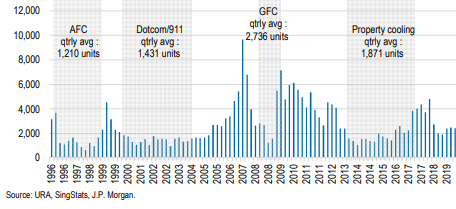

Residential prices could fall by 10% over the next two years

In that report, it was highlighted that residential prices are expected to fall by 10% over the next two years due to the current recession. However, the fall in prices will not be as drastic as past property downturns such as those witnessed during the Asian Financial Crisis and Dotcom bust due to three factors: 1. Median household income has been on the rise, 2. The upcoming supply is not as significant and 3. Potential for policy relaxation.

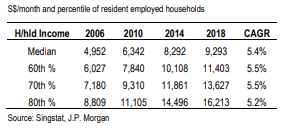

With median household income rising over the last few years and property prices only experiencing a modest increase since then, the price to median household income is at the lowest level heading into a recession over the last 25 years and this should mitigate any potential price falls.

Assuming flat median household incomes and price to income falls to troughs experienced in previous down cycles, residential prices could fall 3-22%.

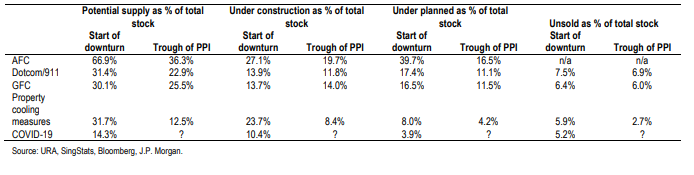

However, given significantly less percentage growth in upcoming supply compared to the Asian Financial Crisis period, as well as robust government support for the economy as seen from the various budgets dished out since March 2020 plus potential additional fiscal stimulus packages ahead, the JP Morgan team does not expect a 20%-plus fall in property prices.

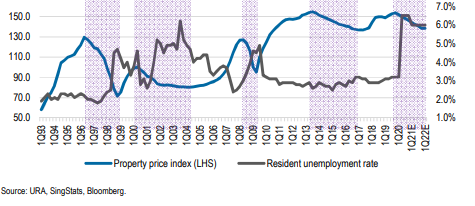

Overall the expectations are for property prices to correct by around 10% over the next two years. While the unemployment rate could spike to 6.0-6.5%, strong government support through wage subsidies and stimulus as well as mortgage deferrals will help temper distressed selling and price falls.

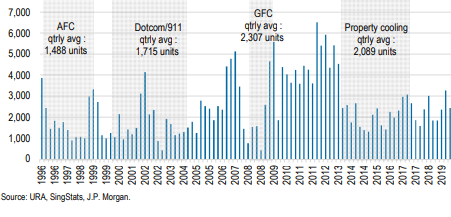

Sales volume to bottom in 2Q20

With the peak of the circuit breaker in 2Q20, JP Morgan expects volumes to bottom out in the quarter with new sales volumes to track below 1,000 units.

Looking ahead, developers will start to offer discounts to stimulate demand. JP Morgan believes this is especially for projects that are approaching the five-year ABSD deadline, the first tranche hitting in 2H21 or early 2022 after the temporary six-month delay offered by the government arising from disruptions to the industry from the two-month circuit breaker.

Probability of policy relaxation

With property prices only just starting to fall, down c.1% during 1Q20, JP Morgan does not expect major policy relaxation in the near term. They expect the total debt servicing ratio to remain in place for the foreseeable future to ensure borrowers remain prudent.

A potential reversal of the lower loan-to-deposit ratios and additional stamp duty imposed in July 2018 may happen if there is a rapid decline in property prices approaching the 5-10% levels. Any policy relaxation measures would be focused primarily on genuine buyers rather than supporting speculative investments given the low-interest-rate environment.

Deposits for first-time home buyers were raised to 25% from 20% in 2018 and this could be reversed.

As many developers have yet to cut their prices, there is no urgency for the government to act and would rather take a “wait and see” approach unless heavy price discounting happens, causing a severe negative feedback loop as we approach 2H21, when the first tranche of properties approach the five-year deadline.

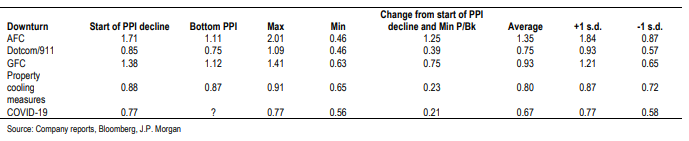

How do developers trade in a declining price environment before a recovery?

In prior downturns, P/Bk multiples drifted lower and only bottomed out 4, 11, 4, and 22 months ahead of the lows of PPI during the AFC, Dotcom bust, GFC and 2013-2017 downturn, respectively. P/Bk multiples fell by 0.21 to 1.25 points.

With their expectations of a 10% decline in property prices, they believe the most comparable episode would be 2013-17, rather than AFC, Dotcom and GFC downturn where they experienced a 20-45% decline in prices.

Given developers on average have already corrected by around 0.2 P/B points, consistent with what they observed during 2013-2017, they believe that developers are likely to trade within a range until they get closer to a bottom of the property market, potentially in 2022 as developers discount prices to clear inventory.

New launches in 2020

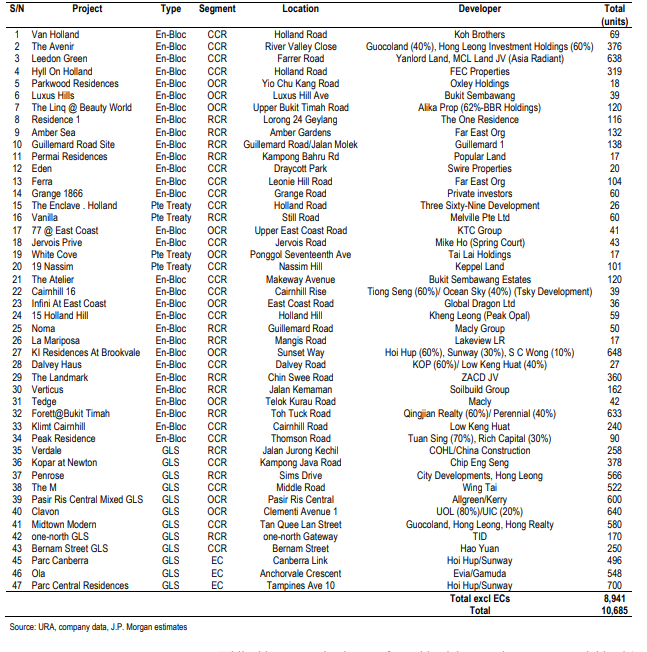

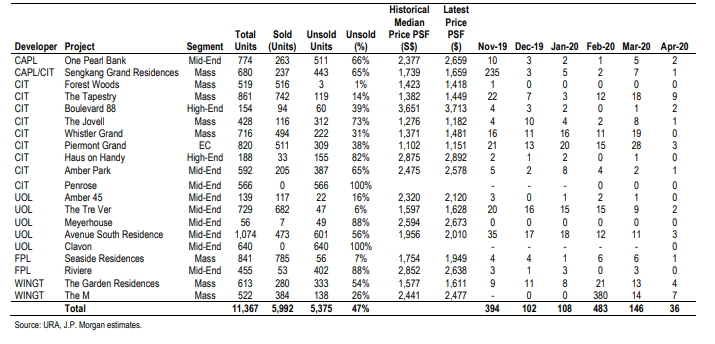

Over 40 new launches totaling c.9,000 units expected in 2020. JP Morgan believes those most at risk are projects in the Core Central Region (CCR) where only 12% of the top 33 CCR projects have been sold.

Rise in median household income to support properties in the OCR and RCR region

While JP Morgan expect property prices to correct by 10% over the next two years, they believe OCR and RCR could potentially outperform CCR due to more resilient HDB upgrader/owners occupier demand.

This relative strength arises mainly from rising income levels. These higher household incomes led the government to raise the higher HDB income ceiling by S$2,000 to S$14,000 in 2019 and follow the four-yearly increments in 2011 and 2015.

This brings the proportion of households eligible for public housing to 74% of residents, up from 67% at the previous S$12,000 income ceiling. Strong HDB upgrader demand has resulted in underlying demand of ~10k units per annum from residents (i.e. citizens and permanent residents), which is equivalent to the underlying demand for public housing.

COVID-19 Phase 2: To Buy Or Not To Buy Property, That Is The Question

The following content is written by Stuart Chng

Finally, today at 715pm, the announcement of Singapore entering Phase 2 of Circuit Breaker re-opening was made!

How wonderful that we finally will be getting back much of our freedom – the simple joys in life from eating our food at a coffee shop to bringing our kids to the playground.

While this news has brought about much-needed cheer and optimism, many property investors waiting on the sidelines caution that this does not fundamentally change the fact that we are heading into uncharted waters in lowered GDP and unemployment figures.

By now, it is clear that the world is going through a crisis that’s bigger than anything seen since the Great Depression.

This message has been echoed by many authorities from our Prime Minister and cabinet ministers, the World Bank and IMF and it doesn’t take a genius to point out the obvious implications.

So begs the question:

Where in the world is it economically safe from COVID-19?

Does it automatically mean that any country becomes attractive as an investment destination just because it has COVID-19 under control?

I would like to preface my sentiments with a short macro market outlook that i shared with my team back in Dec 2019, when the first signs of the virus emerged.

A Constant State Of Disorder

It occurs to me that the world is in a constant state of conflict – At any point in time, somewhere in the world, a major conflict is bubbling and threatening global trade and oil prices.

By now, if you are in your 30s or older, you should have seen enough and gotten used to this fact of life.

In more recent times, apart from the COVID-19 situation, we are spectators to the US-China escalated tensions and blame games, the never-ending Taiwan drama-esque titled “BREXIT”, the bitter rivalry and trade tensions between Japan and Korea, and the revolution in Hong Kong.

In the midst of these chaos in major economies around the world, massive money supply still exists and continue to be created as we speak, as a result of low interest rates and the stimulus that has hit the world since 2008.

Sadly, as history has shown, the wealth divide gets wider during such times and the rich will get richer, and the poor poorer as a result of asset bubbles where too much money chases after too little assets.

In stormy seas, capital seeks safe harbours – safe assets which help preserve capital and prevent erosion from volatile markets or inflation.

What then are classified as safe assets?

By Investopedia’s definition,

Safe assets are assets, which do not carry a high risk of loss, across all types of market cycles.

Common types of safe assets include government bonds, USD and Yen currencies, treasury bills, money market funds and you probably saw it coming, real estate.

For Singaporeans and PRs, i find that one of the best risk-free investments we have is our CPF Special Account that pays us at least 4% per annum in good times or bad.

I know some of you might debate this on the basis of opportunity costs as we cannot touch the funds till retirement.

But we shouldn’t deny that for many people, preventing access to funds might actually be doing them good.

Plus, how many of us have a track record of making at least 4% returns per annum over a sustained period of time?

Now, back to the topic, if you have capital on the sidelines and are waiting to pull the trigger on property investments, the 3 questions you should ask yourself today is:

- Is Singapore real estate a high risk investment?

- Will its value go to zero?

- What other investments in the world can give you a similar risk-reward ratio?

Let me share my point of view briefly.

Is Singapore Real Estate A High Risk Investment?

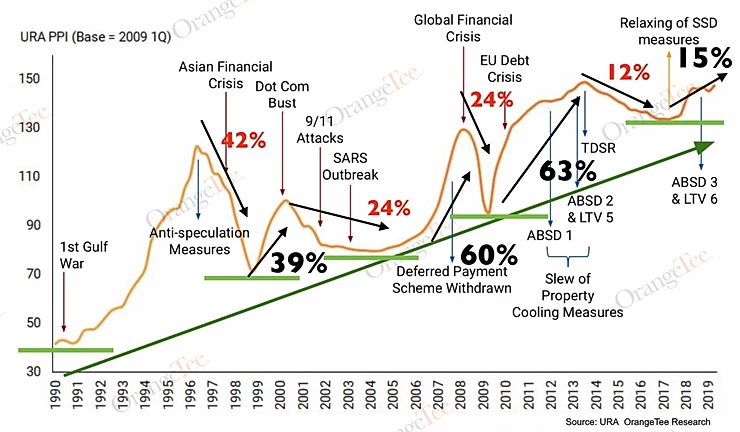

You may have seen this chart in various iterations.

This chart shows us how historically Singapore private property prices touches new highs and corrects to higher lows in almost every cycle.

Behind the upwards trend in prices are fundamental reasons that i pointed out in my previous article – Key factors that have driven up property prices in Singapore over the past decade

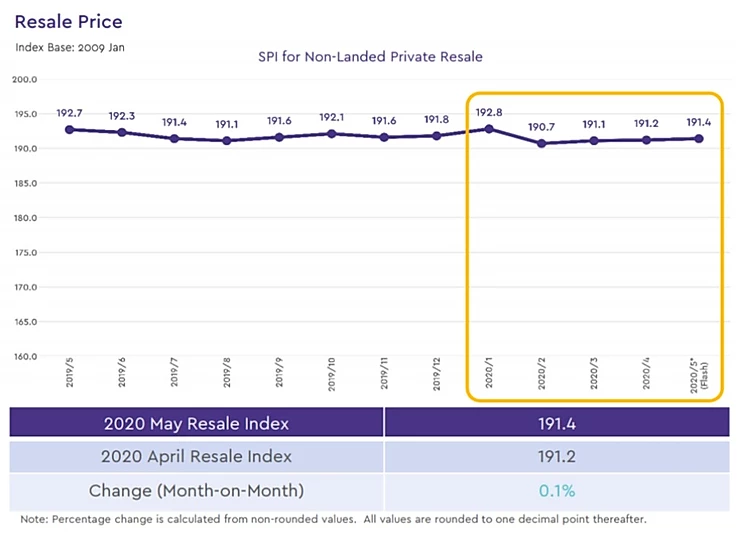

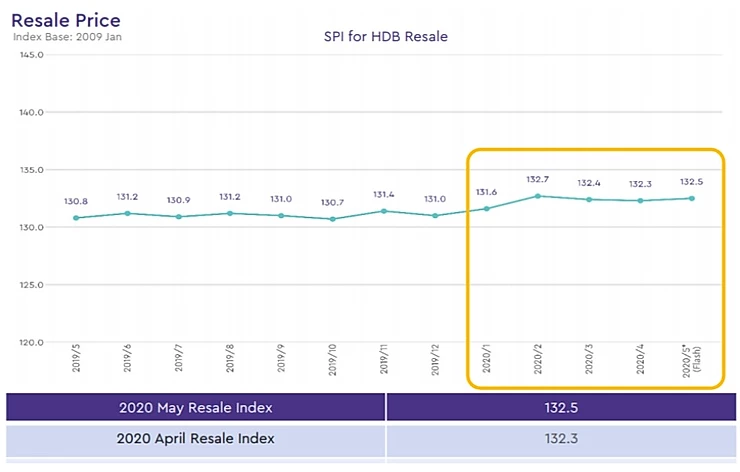

More importantly since Feb 2020, we have seen how the Straits Times Index corrected 20% year to date and yet the HDB and private property market index held itself steady despite unprecedented market volatility.

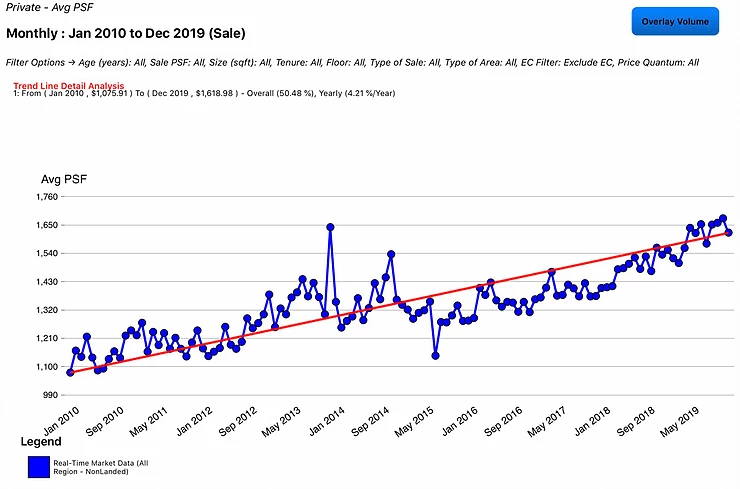

Recent Private Non-Landed Resale Price Trends

Recent HDB Resale Price Trends

Is there any connection between the government’s efforts to prop up the economy and the real estate market’s resilience?

Perhaps the multiple property market stabilizers put in place since 2009 and the recent temporary relief measures are alot more effective than we all have time to look into right now.

Will Real Estate As An Investment Go To Zero?

This is an easy answer. The answer is no. Real estate investments, at least in Singapore, typically do not go to zero.

I know that very rare cases do occur, like in the case of Sycamore and Laurel Tree by Astoria Development.

Or if you buy into a property with a short remaining tenure and hold it till its expiry;

but in which case, you should be rewarded with a relatively high rental yield and enjoy a fairly good return on investment.

What Other Investment Options Can Provide You A Similar Risk-Reward Ratio?

Let’s take a look at the top 10 blue chip stocks (By market cap) in Singapore obtained from TheFifthPerson.com.

According to the source, if we had invested in each of them equally, our CAGR would have been 6.9% per annum, including dividends.

Given the same time period, let’s take a look at how the Singapore private non-landed market performed.

In the same period, the private non-landed market (Excluding ECs) grew by 50.48% or 4.21% per annum.

Bear in mind that this assumes zero leverage which is unusual for property investments.

Assuming a conservative 50% loan, and 20% for tax, expenses and interest repayments, the capital growth rate would have been an estimated 80.8% or 6.1% per annum without accounting for rent received. Adding in a market average rental yield of 3% would bring an investor an almost 10% return per annum.

The cynical ones might now be thinking, can real estate perform the same way as it did over the past 10 years?

Well, no one can guarantee that. But neither can one guarantee the same performance for any stocks they buy.

Now, the question is, which investment has a higher probability of being affected by market forces?

Remember the once invincible giants – Kodak, Nokia, Dell, Toys R Us, Hyflux and Yahoo among others.

In their hey days, many believed that they were robust companies with a great future just like what the market believes about FAANG stocks today.

But can we honestly predict how these shares will turn out a decade or more from now?

Will they retain their competitive edge or will they cease to exist like some of these once-greats?

With that in mind, how does the risk-reward ratio now look when comparing STI blue chips and property investments?

Remember, with properties, there’s hardly a chance of disruption or human mismanagement that would cost it to go to zero as long as we make simple prudent decisions well.

The Singapore Dollar – A Safe Haven Currency?

Over the past decade, the SGD is one of the only 4 currencies globally to have appreciated against the USD, till date still the reserve currency of the world. (Source: XE.com)

The other 3 currencies being the Swiss Franc, Thai Baht and Israeli Shekel.

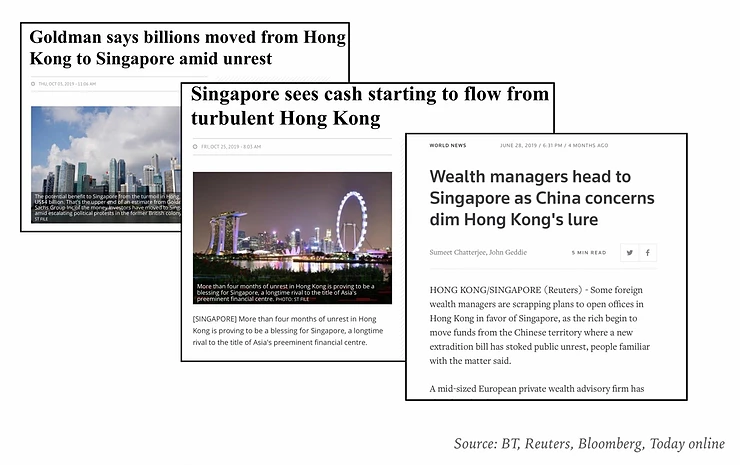

This wealth preservation aspect of our Singapore currency is one of the major factors why notable high networth individuals continue to migrate here and make us their base of operations and home, on top of the other fundamental attractiveness of our nation.

Despite our government’s diplomatic and gentlemanly claims that there isn’t a rising influx of funds, it appears that market stakeholders are reporting different experiences as evident below.

So If Real Estate Is A Choice Investment Vehicle, Why Not Look Around?

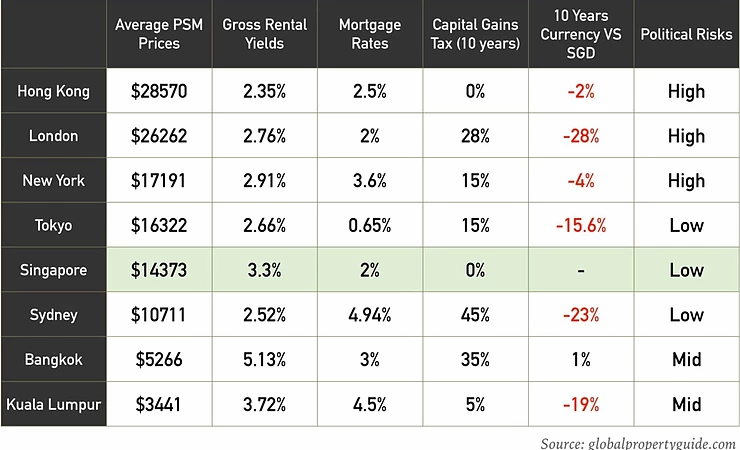

Fair enough and let’s take a look at the most popular real estate markets for Asian investors.

Although we are not the cheapest or offer the highest rental yields, Singapore is in a sweet spot that anyone with sufficient research would have to agree, puts our country’s real estate market in a very enviable position today.

I know there are those who continue to disagree that Singapore real estate is a safe haven, because perhaps in their definition, a safe haven is a mythical place where investors are completely sheltered from market forces.

That is a logical fallacy as all investments carry risks. In fact, uninvested funds carry its own risks as well.

A safe haven, is what it should be. A place where wealth is preserved amidst stormy seas, in preparation for exciting times when clear skies return.

Hence, I believe that the more chaotic the world is, the more attractive Singapore becomes.

And it is not just because i am a Singaporean or a property agent blinded by my own biases that i say this, but because, Singapore’s destiny as a safe haven asset class on a global stage has already been cemented in the minds of many top money managers around the world many moons ago.

Perhaps on hindsight, the majority will see more clearly. And hopefully, by then, they would still enjoy ample runway to benefit from the growth that’s yet to come.

JP Morgan Singapore Property Report

Do Like Me on Facebook if you enjoy reading the various investment and personal finance articles at New Academy of Finance. I do post interesting articles on FB from time to time which might not be covered here on this website.

SEE OUR OTHER STOCKS WRITE-UP

- TOP 10 SINGAPORE GROWTH STOCKS FOR 2020 [PART 1]

- DIVIDEND INVESTING STRATEGY: COMBINING KEY RATIOS WITH ECONOMIC MOATS

- VALUE INVESTING IN SINGAPORE: 10 SG VALUE STOCKS THAT MIGHT MAKE SENSE

- ULTIMATE GUIDE TO REITS IN SINGAPORE (2020)

- SPH REIT: MASSIVE DPU CUT. IS IT ATTRACTIVE NOW?

- 10 GREAT REASONS TO BUY REITS AND 3 REASONS TO BE CAUTIOUS [UPDATE 2020]S IT A GOOD BUY NOW?

Disclosure: The accuracy of material found in this article cannot be guaranteed. Past performance is not an assurance of future results. This article is not to be construed as a recommendation to Buy or Sell any shares or derivative products and is solely for reference only.