Is McDonald a good investment now? To answer that question, I look to evaluate the company based on Warren Buffett’s methodology as described in the best-selling book Buffettology which some of you might be familiar with.

This will be the first of many stocks that will be evaluated using Buffett’s methodology of stock investing using a 2-step process:

First evaluating the stock’s business fundamentals. If the company’s fundamentals warrant the case for an educated “guess” of its future earnings potential due to the stability of its business, we will then proceed to the second step which is Pricing Analysis.

Bottomline: A good stock at an expensive valuation will not make a good investment. Hence regardless of how stable a business like McDonald might be (has been in operation for close to eight decades), we will only initiate a position for our portfolio at the right price.

This series of analysis is meant to be a structured process that will help the beginner investors avoid the many potholes likely present in his/her investing journey.

It is not meant to be comprehensive, nor does it cover the latest developments of the company on an in-depth basis. However, with a long-term view in mind, these “Buffett-approved” stocks are unlikely to be at risk of becoming obsolete over the next decade.

McDonald’s business analysis

Before we begin our price analysis, there are 9 questions that one would have to ask pertaining to the company’s business operations:

Does the company have any identifiable consumer monopolies or brand name products?

Most people would have eaten a McDonald burger. My 3 years old kid definitely has his fair share of Happy Meals. In fact, you will be hard pressed to find anybody who hasn’t eaten a McDonald burger.

They are the largest fast-food chain in the world and as at the end of 2018, McDonald operates 37,855 restaurants in over 120 countries, serving on average 68m customers each day.

Richard and Maurice McDonald founded this amazing company 79 years ago on May 15 1940 and since then McDonald fast food has been a household name and will likely to remain one for many years to come.

So Yes, the company definitely has got an identifiable consumer-monopoly brand-name product. While there is no short of competition, with Warren Buffett actually invested in one of its key rivals, Restaurant Brands International (owner of Burger King), it is unlikely that any restaurant chains will usurp McDonald’s dominance as the “King of Fast Food” over the next decade, on our view.

Is the company conservatively financed?

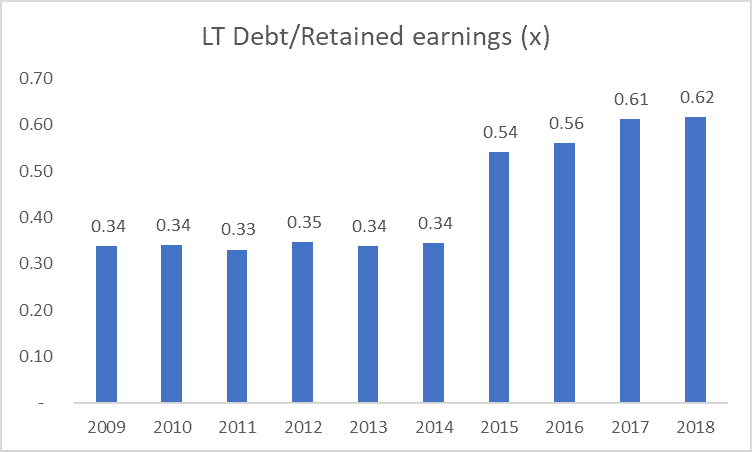

The company has got approx. USD31bn in long-term debt. It is in a unique position of being negative equity, hence the net debt/equity ratio isn’t very relevant in this scenario. We will explain more of this negative equity phenomenon in the following segment.

For now, we based McDonald’s equity on its retained earnings which amounted to USD50bn as of end-2018. Hence net debt/equity is approx. 62% which is below our maximum threshold of 1x or (100%).

We believe McDonald has been using cheap debt to finance the purchase of its share buy-backs. This is not a major concern at present, in our view. However, if cost of debt starts creeping up, this will become a point of contention.

However, given McDonald’s illustrious history and exposure to the generally recession-proof fast food industry, it is highly unlikely that its bankers will bail on it.

Are the earnings strong and do they show an uptrend?

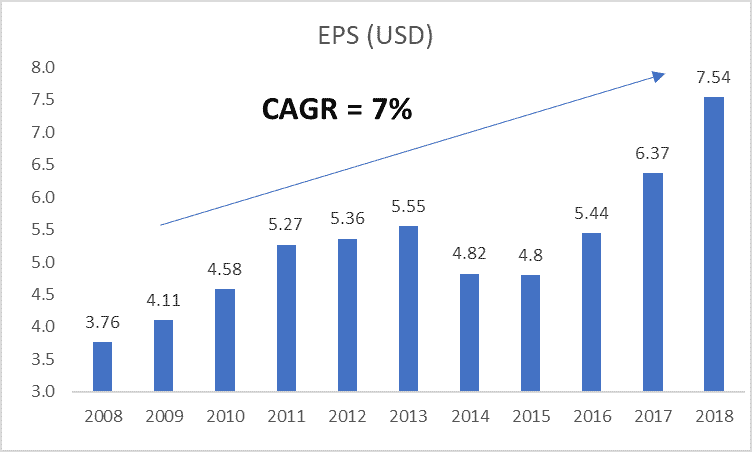

A check of McDonald’s per share earnings indicate that they have been growing at a rate of 7.2% compounded annually for the period 2008-2018. Earnings can be considered rather consistent and generally on an uptrend.

Is the company allocating capital to its realm of expertise?

The company is allocating capital only towards expanding its fast food restaurant business. We don’t see the company allocating capital into the real estate or the energy business, do we?

In fact, due to its franchising model, the burden of restaurant expansion falls on the franchisee and not on the company itself, hence, capital expenditure is typically very manageable. We will touch on this topic in a later segment.

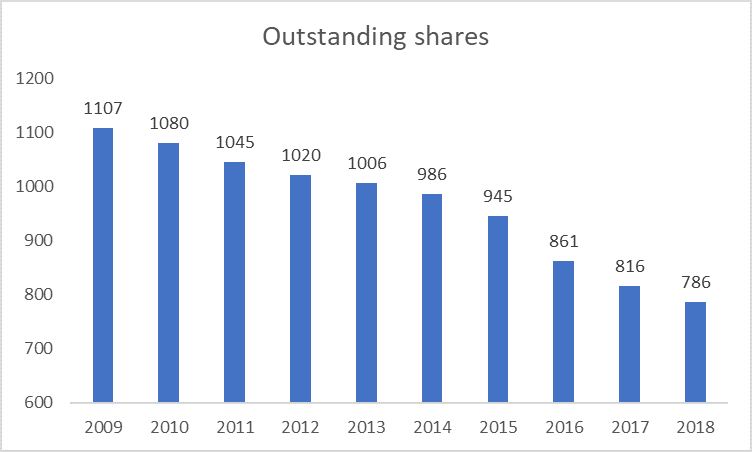

Is the company doing share buy backs?

The company has been consistently buying back its shares over the past 10 years. In fact, McDonald’s 3-year average share buyback ratio is ranked higher than 95% of the 246 companies in the restaurant industry.

Is the company increasing shareholders’ value?

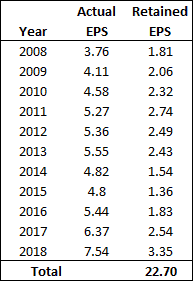

The company has generated a total of USD22.7/share in retained earnings over the period of 2008-2018. During this period, earnings per share (EPS) grew by USD3.78 from USD3.76 as of end-2008 to USD7.54 as of end-2018.

Thus we can argue that the retained earnings of USD22.7/share produced in 2018, an after- corporate tax return of USD3.78/share, which equates to a rate of return of 16.7%.

Rate of return = 3.78/22.70 = 16.7%

This indicates there has been a profitable allocation of retained earnings and a corresponding increase in earnings per share.

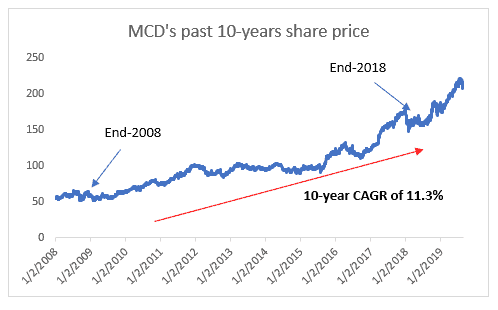

This has caused a similar increase in the market price for McDonald’s stock, from approx. USD60 as of end-2008 to USD175 as of end-2018. Currently, the share price of McDonald sits at USD211.

What is the ROE of the company?

McDonald is in a unique position where it has negative total equity. Normally, a share that exhibits negative total equity, where its total liabilities exceed its total assets, is generally one in financial distress where the company has racked up significant accumulated losses over time.

However, in McDonald’s case, the major driver in the significant equity change is the fact that they have bought back more than USD20bn in stocks over the past four years, which reduces both its assets and equity component. This demonstrates the financial strength of McDonald.

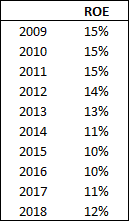

Hence, we will not be able to compute its ROE, looking at its total equity component. Instead we will use retained earnings as the equity base to compute adjusted ROE.

Adjusted ROE ranges between 10-15% with the latest ROE figure at c.12%. Not the best-case scenario where we will like its ROE to be in excess of 15%.

Is the company free to adjust prices to inflation?

Well, as we all know, the price trend of burgers is one directional, UP. How about the size of the burger? DOWN. There you go.

Do operations require large capital expenditure?

McDonald’s operations do not require large capital expenditure as franchisee are responsible for costs of building most of the restaurants. Nor does the company have to spend large amounts of money upgrading their plant and equipment.

The company generates about USD6-7bn/annum in operating cash flow while capital expenditure typically hovers in the region of USD1.6-2.5bn. This leaves plenty of free cash flow available for dividend payments.

Based on the above business assessment, we can safely say that McDonald is one of those stocks that fits nicely in what Buffett might term as stocks with “high earnings visibility”.

The low variability of the company’s earnings as illustrated over the past decade makes it a candidate for us to “credibly” forecast its earnings trend over the next 10-years.

We hence proceed to our Price Analysis segment.

McDonald’s Price Analysis

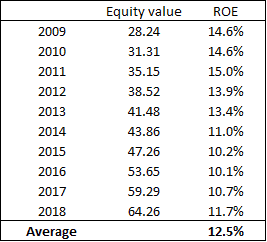

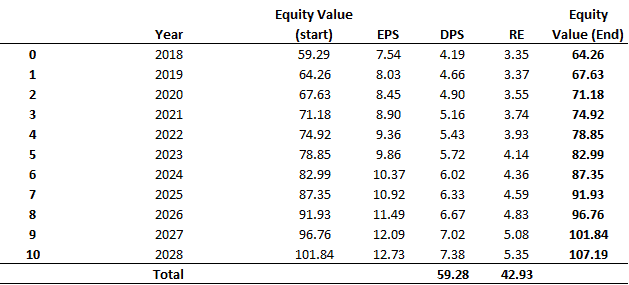

From a ROE standpoint, we can argue that as of end-2018, McDonald has a per share equity value (retained earnings/outstanding shares) of USD64.26. The company’s 10-year average ROE is at 12.5%.

If McDonald can maintain its 10-year ROE at 12.5% and retain approx. 42% of that return, with 58% being paid out as dividend, then McDonald’s/share equity value should grow at an annual compounding rate of 5%. Not very exciting in our view.

McDonald’s equity value in 2028

Based on such a forecast, the company will generate a per share equity value of c.USD101.84 by 2028. If the company is still earning an ROE of 12.5%, then McDonald should report an EPS of USD12.73.

EPS = Equity value per share * ROE (assume fixed at 12.5%)

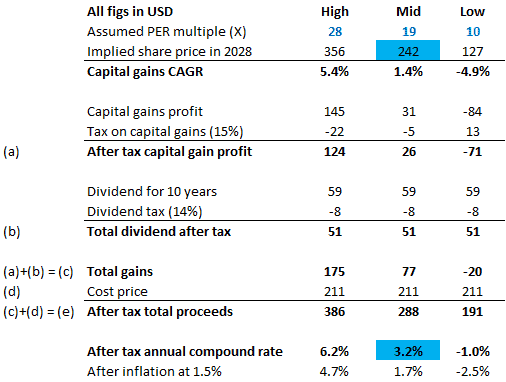

Assuming entry price of USD211/share. At a PER of 19x which is the average of the current high multiple of 28x and the low of 10x, the implied share price of McDonald in 2028 will be at USD242.

The after-tax annual compound return inclusive of dividends is at 3.2% (see below table for calculation). After a 1.5% inflation adjustment, that returns fall to a meager 1.7%.

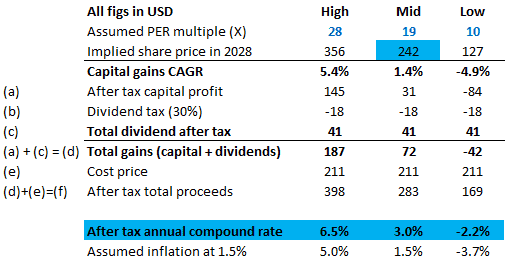

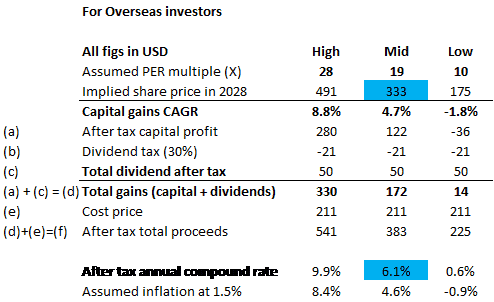

For overseas investors, the after-tax compound rate of return is slightly lower at 3.0% as no capital gain tax is required. This is however partially offset by 30% on dividend withholding tax.

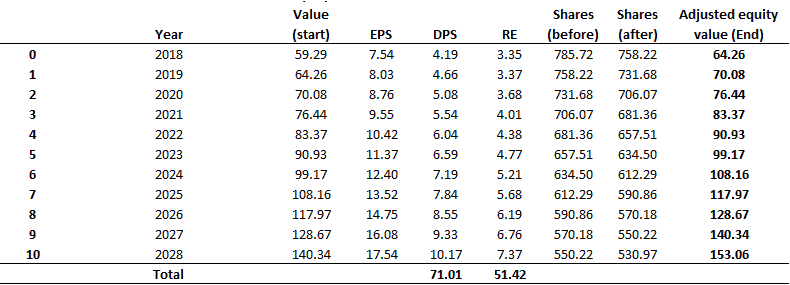

However, the above analysis takes into assumption a constant share-base. McDonald’s outstanding share base has in fact been declining at an average clip of 3.7% over the past 10 years.

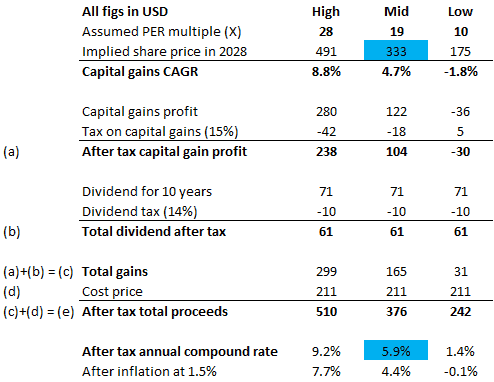

Assuming a 3.5%/annum decline in share count base (strong free cash flow used for share buy-back), our analysis shows that McDonald’s equity value will be growing at a rate of 9.1%/annum vs. the original 5.3%.

McDonald’s equity value in 2028 (w share buy-back)

The forecast equity value per share equate to USD140.34 by 2028. Based on the same ROE rate of 12.5%, EPS in 2028 is forecasted to be at USD17.54.

Based on our base case PER multiple of 19x, that translates to an after tax annual compound rate of 5.9%. Taking into account 1.5% inflationary effect, the after-inflation CAGR is reduced to only 4.4%.

If the PER multiples remain at the current elevated rate of 28x, that will generate an after inflation annual compound rate of 7.7% for US investors and 8.4% for overseas investors.

However, as we will like to play it conservatively, we will NOT be making our financial decision based on what we deemed as a “Bullish” scenario, one which we believe McDonald’s valuation is currently at.

Our ideal entry price, based on our current assessment of the stock is at USD170/share. At this level on our base case scenario, the after-tax annual compound rate is at 8.1% (6.6% after inflation) for US investors and 8.5% (7.0% after inflation) for overseas investors.

Over the very long run, the stock market has had an inflation-adjusted annualized return rate of between 6-7%. This will be our benchmark rate moving forward and most of our stocks for portfolio consideration will have to generate a minimum of 6.5% inflation-adjusted long-term return.

Conclusion

McDonald fits the Buffett criteria as one stock that has strong earnings visibility where earnings can be “accurately predicted” due to the stable nature of its operations.

While it scores highly (8 out of 9) in terms of the business assessment of the stock (only its historical ROE component was less than our ideal minimum target of 15%), its current share price does not yet warrant an entry.

This is simply the case of a good business at the wrong price.

We will put the counter in our watch list and might engage in some put option selling at a strike price of USD170/share to collect premiums as we wait for the market to “adjust” its share price to our ideal target level.

Take a look at our other investment coverage

We have previously also written on Straco which is a strong cash-flow generating SGX-listed stock that is also currently in our watch-list, with a target entry level of SGD0.70/share.

Disclosure: The accuracy of material found in this article cannot be guaranteed. Past performance is not an assurance of future results. This article is not to be construed as a recommendation to Buy or Sell any shares or derivative products and is solely for reference only.

3 thoughts on “Buffett series: McDonald”

1. Negative equity might be because they did so much buybacks

2. Another possibility might be that one of their main assets – their brand – is not reflected in their assets as their brand is homegrown

3. More details on negative equity here: https://www.wallstreetmojo.com/negative-shareholders-equity/

4. Maybe can look at ROIC instead of ROE in this case … then back out the debt from EV/EBIT multiple?

Hi,

Thanks for sharing. Yes you are right that negative equity is generally due to their share buy back policy that increases their treasury share holdings. ROIC is possible as well. In fact ROIC generally tends to be a better measure of returns when we take their usage of debt into consideration as well.