SG stocks to buy: Upgrades/Downgrades by analysts

Can we trust analysts’ reports? Throughout the years, we occasionally see analysts flip-flopping between BUY and SELL calls within several weeks. As investments are highly subjective to one’s view, the difference in perspective is understandable. However, it led to certain controversies as investors argue that there may be a hidden agenda behind them.

A recent example would be in March 2021 when the market was hit with fears of higher interest rates. I recalled analysts at JP Morgan issuing an “underweight” position on both S-REITs and industrial REITs. This fuelled the fear in investors and caused a further sell-off in REITs. However, some investors saw it as an opportunity to “buy the dip” and the counters such as Mapletree Industrial (SGX: ME8U) swiftly rebounded by 7% the following week!

Analyst reports provide you with a useful source of information but investors should not solely rely on them to make investment decisions! In this series, we’ll look to analyze three upgrades/downgrades made by analysts in the current month.

Summary of picks for July

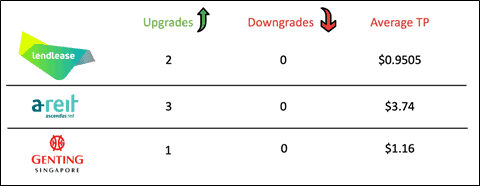

For our July picks, these are the stocks that we will be analyzing – Lendlease REIT (SGX: JYEU), Ascendas REIT (SGX: A17U), Genting Singapore (SGX: G13). This is a quick summary of the analyst buy and sell calls for July. As shown in the picture below, analysts were generally upbeat on the counters as our economy moves towards the next phase. Comparing the three, Genting Singapore provides the highest upside for investors base on the target prices.

Here’s our breakdown of the analyst reports:

Lendlease REIT (SGX: JYEU)

Quick Introduction to Lendlease REIT

Listed at the end of 2019, Lendlease REIT is one of the newer retail REITs offered in the Singapore market. Despite being a smaller-cap S-REIT, they are backed by one of Australia’s largest construction companies – Lendlease Group. Their sponsor owns key assets in Singapore such as Parkway Parade, JEM, and Paya Lebar Quarter.

This can potentially allow Lendlease REIT to unlock future value by acquiring them. Currently, the REIT owns 313@Somerset, Sky Complex in Italy, and a 5% stake in JEM. It was announced early this month that Lendlease is looking to increase its stake in JEM to 31.8%.

Here is a quick summary of the company:

Financial Performance

- Remains resilient amidst the pandemic due to strategic location of assets

- Like other retail REITs, it underperformed against forecast due to Covid-19 and rental waivers

- Comparing 1H of 2021 and 2020:

- Distributable income up by 1.4%

- Dividend per unit up by 0.8%

Portfolio Performance

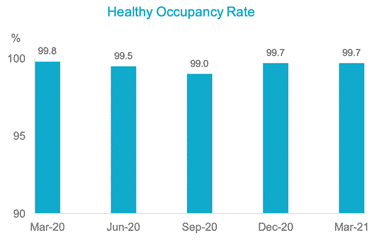

- As of March FY20/21, average portfolio occupancy stood at an impressive 99.7% despite the pandemic.

- Healthy portfolio weighted average lease expiry (WALE) of 9.3 years with Sky Complex leased to Sky Sports with WALE of 11.4 years

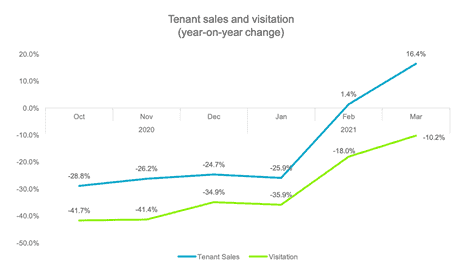

- Growing footfall and tenant sales recovering 94% of pre-pandemic levels

- Healthy gearing of 35.5% with space for further acquisition

Acquisitions

- In June 2021, the company announced an approximate $200million deal to increase its stake in JEM to 31.8%

- The acquisition is expected to be DPU accretive with Pro-forma DPU expected to rise by 3.6%.

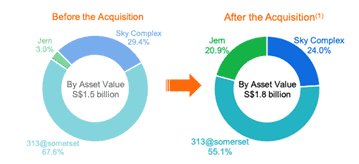

- Increases the company’s exposure to suburban retail and reliance on 313@Somerset will be reduced from 67.6% to 55.1% of AUM

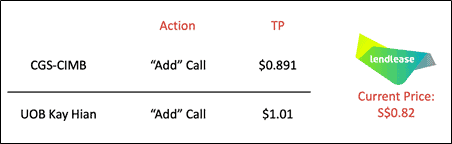

Recent Upgrades / Downgrades by Analysts

For June, analysts are generally buoyant on Lendlease REIT. In the next section, we’ll analyze their key rationale.

Key Rationale of Analysts and My Views

The Attractiveness of JEM (Kicking off potential acquisitions)

Jem is an integrated office and retail establishment strategically located at the heart of the nation’s next CBD. It is highly accessible with direct connectivity to Jurong East MRT, bus interchange, and Ng Teng Fong hospital. For its retail component, Jem is one of Singapore’s largest suburban mall homes to tenants such as IKEA and Don Don Donki. On the other hand, its 12 levels of office space are fully leased to the Ministry of National Development with a long WALE of 24 years.

On top of what JEM offers, the mall is set to gain a boost from several developments in the region. For example, the Jurong Innovation District and Tengah Town are set to offer 95,000 new jobs and 42,000 new homes respectively. In total, it is expected to provide an estimate of 1.1 million in catchment.

The acquisition of a larger stake in JEM provides Lendlease with strategic pre-emptive rights to further acquisitions. Lendlease REIT can also tap on its sponsor’s sizable portfolio with assets such as Paya Lebar Quarter. However, I’m personally expecting a round of equity financing through Private and Preferential placements for the REIT to maintain its low gearing level.

Grange Road Carpark

Located next to 313@Somerset, the carpark is set to complete in 2022 with an expectation to boost the REIT’s DPU by 10%. Lendlease has received several leasing inquiries and two-thirds of the space has already been leased to Live Nation. It is set to rejuvenate the Orchard Area by offering concerts, films, and unique hawker stalls for the public.

I’m personally excited about the developments of the carpark as it is highly accretive for the REIT. It was mentioned by the CEO that Lendlease was the 2nd lowest bidder for the land with an offer that was four times lower than the top bidder!

Higher liquidity

In March 2021, Lendlease was added to iEdge S-REIT Leader Index and iEdge S-REIT Index. The former is highly liquid and often used as an S-REIT benchmark. As a member of the indexes, it is expected to enhance the liquidity and visibility of Lendlease to investors and funds. At the end of 2020, Lendlease was also included under CPF’s Investment Scheme through one’s ordinary account.

To date, Lendlease is part of these indices:

- MSCI Singapore Small Cap Index

- FTSE ST Small Cap Index

- FTSE ST Singapore Shariah Index

- iEdge S-REIT Leader Index

- iEdge S-REIT Index

- GPR APREA Investable REIT 100 Index

The negative impact of potential rental waivers

Despite the positives of Lendlease, Singapore is still not out of the woods concerning Covid-19. With prolonged Work From Home arrangement and potential shutdowns, Lendlease is still susceptible to potential outbreaks. For example, CIMB expects FY21 DPU to fall by 5.8% should the REIT provide a month of rental rebates to all tenants at 313@Somerset. However, it is to note that the REIT has resisted providing rental rebates since July 2020.

Will I buy Lendlease REIT?

I agree with both analysts that Lendlease is fundamentally undervalued, trading at a discount to its NAV/Unit of S$0.85. As our economy progressively opens up with higher vaccination rates, Lendlease will benefit from both higher domestic consumption and tourism.

For your referral, below is a picture of JEM I’ve taken in June right before lunch hour. It is a reality that retail malls are still suffering and footfall has yet to recover. However, I believe that the market is always forward-looking and such scenarios are priced in.

Ascendas REIT (SGX:A17U)

Quick Introduction to the Ascendas REIT

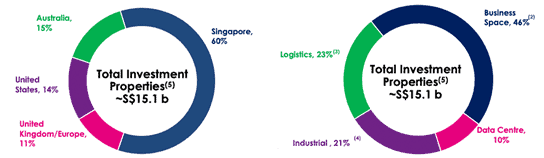

Ascendas REIT is a large-cap S-REIT and the largest industrial REIT listed in Singapore. Backed by CapitaLand – majority-owned by Temasek, Ascendas has an Asset Under Management (AUM) of S$15.1billion in 209 properties across regions and asset classes. The REIT remains resilient amidst the pandemic and they’ve completed a 75% acquisition of Galaxis in June 2021.

Here’s a quick summary of the REIT:

Financial Performance

- Remains resilient amidst the pandemic with a strong balance sheet

- Year on Year Performance:

- Gross revenue up by 13.6%

- Distributable income up by 6.7%

- DPU dropped by -6.1%

- Performance was slightly tapered down due to S$19.5million in Covid Grants for FY20/21

Portfolio Performance

- As of Q1 FY21 average portfolio occupancy dipped from 91.7% to 90.6%. This was mainly attributed to non-renewals. However, there was a positive rental reversion of 3%

- Healthy WALE of 4.1 years

- Gearing stood at 38% with room for further acquisitions

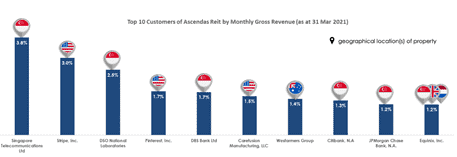

- Low tenant concentration as largest tenant contributes to only 3.8% of gross rental revenue

Acquisitions

- In June 2021, the company announced a S$543.8million acquisition of the remaining 75% interest in Galaxis

- The acquisition is expected to be DPU and NAV accretive. Pro-forma DPU and NAV is expected to rise by 0.46% and 0.9% respectively

- However, some investors were skeptical over the acquisition as Ascendas acquired 25% of Galaxis in March 2020 at a lower valuation

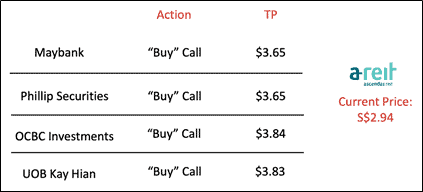

Recent Upgrades / Downgrades by Analysts

For June, there were four analyst reports on Ascendas REIT with all issuing a “buy” call. In the next section, we’ll analyze their key rationale.

Key Rationale of Analysts and My Views

Accretive Acquisition

Although the private placement closed on the lower end, the acquisition is both DPU and NAV accretive for investors. The occupancy rate at Galaxis business park stood at 98.6% with renowned tenants such as Sea, Canon, and Oracle.

Here are the benefits of the acquisition:

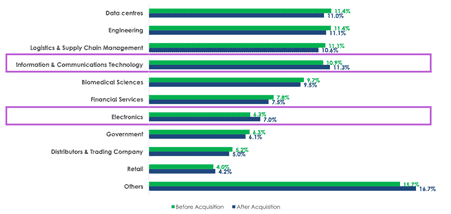

- Income from top 10 tenants reduced from 19.3% to 18.5%

- Higher rental contribution from both Information & Communication Technology and Electronics sector

- Capitalizing on a rare opportunity to acquire full control of a business park with a remaining lease of 51 years. Currently, the Industrial Government Land Sales Programme is only releasing shorter tenure land between 20 to 30 years

Ability to capitalize on potential opportunities

Ascendas announced their intention to divest three Australian logistic properties in June. Expected to complete by 3Q21, sales proceeds are 16.8% higher than market valuation. As a result, gearing is expected to fall to 37% with debt headroom of S$4billion for expansion.

Valuation

Industrial REITs tend to trade on a premium due to the resilient nature of business parks, logistics, and data centers. At its current price, Ascendas is currently trading at a Price/Book ratio of 1.29x which is below the average of over 1.36x for Industrial REITs. I believe that Ascendas is currently undervalued as Mapletree Industrial REIT (SGX: ME8U) is currently trading at a Price/Book of 1.7x.

Will I buy Ascendas REIT?

At the current price, investing in Ascendas will provide a dividend yield of 5.4% to 5.7%. With the size and track record of the REIT, I believe that it provides more value than other industrial REITs. An example would be Mapletree Industrial that is trading at a premium with a lower dividend yield. Overall, I share the same view as the analysts and remain bullish on Ascendas REIT.

Genting (SGX: G13)

Quick Introduction to the Genting Singapore

Genting Singapore owns one of the largest Integrated Resort (IR) in Asia – Resort World Sentosa (RWS). Their portfolio spans from Universal Studios Singapore, casino, SEA aquarium to hotels, MICE, and retail outlets. Being a staple of the Straits Times Index, they are one of the largest companies in Singapore by market cap.

Here’s a quick summary of Genting Singapore:

Financial Performance

- Being part of the tourism sector, the company is greatly affected by the pandemic.

- Recorded the worst financial performance since 2010

- Year on Year comparison:

- Gross Profit declined by 76.8% from S$1billion to S$231.9million

- Net Profit declined by 90% from S$688.6million to S$69.2million

- FY2021Q1 performance:

- Profit fell by 26% on a quarter on quarter comparison

- Earnings would have declined more without Government aid

Recent Upgrades / Downgrades by Analysts

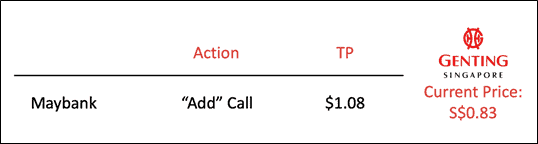

In June, Maybank issued a “buy” call with considerable upside. In the next section, we’ll analyze the key rationale of the analysts.

Key Rationale of Analysts and My Views

RWS 2.0 Expansion Plans

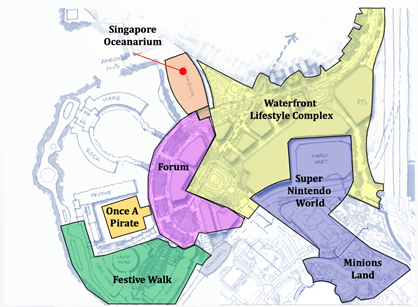

In 2019, Genting Singapore unveiled an RWS 2.0 expansion plan with an investment of S$4.5billion. It is set to enhance RWS’s gross floor area by 50% with an additional 164,000 square meters of leisure and entertainment space. This will be the first expansion of Universal Studios Singapore with “Minion Park” and “Super Nintendo World”.

Further, Genting Singapore is planning to build additional MICE facilities along with an expansion of the SEA aquarium. RWS 2.0 is set to play an integral part in the future Greater Southern Waterfront and rejuvenate RWS.

Japan Integrated Resort Opportunity

In June, a consortium led by Genting Singapore submitted their proposal to build a gambling resort in Yokohama. With only two applicants, they will have a straight fight against Melco Resorts. A key reason for Maybank’s upgrade is their belief that Genting Singapore would clinch the deal. Based on their estimates, the Yokohama IR will generate US$2.7billion in net profit and accretion of S$1.8billion to Genting Singapore. The boost in value has yet to be factored into the current market price of S$0.83.

However, there is an upcoming mayor election in the Japanese city that can change the sails in Yokohama. Out of the six mayoral candidates, at least four have indicated their intention to stop the bid. Therefore, this would be a tactical buy as an anti-IR Yokohama mayor might be elected.

Will I buy Genting Singapore?

I believe that an investment in Genting Singapore solely on the Yokohama IR would be similar to playing a game of chance. However, it doesn’t rule out the possibility of them going for another IR deal. On the other hand, the RWS 2.0 expansion is exciting as a part of the Greater Southern Waterfront.

However, tourism is highly dependent on other factors and returns may fluctuate. Genting might be a good recovery play as the economy opens up but I wouldn’t be as bullish as Maybank.

Conclusion

These stocks are the latest upgrades made by the street. Do note that this article is “For Your Information” only and not an inducement to BUY or SELL any of the stocks mentioned in this article. Please do your own due diligence.

Among the 3 stocks, I believed that Ascendas REIT presents the most “value” while Lendlease REIT currently has strong positive momentum. I have done up a video on Lendlease REIT to provide more information on the counter.

At NAOF, we will be looking to provide monthly analysis on analysts’ reports to help you in your investment decisions! Stay tuned and all the best in your investments!

Do Like Me on Facebook if you enjoy reading the various investment and personal finance articles at New Academy of Finance. I do post interesting articles on FB from time to time which might not be covered here in this website.

Join our Instagram channel for more tidbits on all things finance!

SEE OUR OTHER WRITE-UPS

- Best Performing Singapore REITs [Update June 2021]

- Merger between Keppel Corp and Sembcorp Marine

- Top 3 SG Blue Chip Stocks with Most BUY Calls by Analysts

- Best ETFs in Singapore to structure your Inflation-Proof passive portfolio

- SIA MCB: A Great Way to Financial Engineering?

- 7 Singapore Blue-Chip stocks still yielding more than 4% [June 2021]

Disclosure: The accuracy of the material found in this article cannot be guaranteed. Past performance is not an assurance of future results. This article is not to be construed as a recommendation to Buy or Sell any shares or derivative products and is solely for reference only.