I talked about Idexx laboratories (Idexx) back in October 2019 when the counter was trading at USD272/share and was valued at close to 60x PER. My conclusion then was that despite its hefty valuation, the counter can still generate an after-inflation return of 7.6% on my base/mid-case scenario using Buffett-style analysis and deserve an entry. The counter is now trading at USD325/share or a close to 20% return from 9 months back.

Is there still a business case for getting into Idexx? Apparently Motley Fool US believes so as it is one of their latest Best Buy recommendations. I will look to evaluate the company using a similar style that I have done previously to see if its current price of USD325/share remains an attractive one. Before that, let’s briefly take a look at what the company is all about.

Idexx has also been featured a number of times in my other write-ups:

8 OUTPERFORMING STOCKS TO BUY NOW (PART 2)

10 “MUST-HAVE” STOCKS FAVORED BY MOTLEY FOOLS US

Idexx Laboratories: Market Leader in Pets Diagnostic Tests

Idexx is the leading global manufacturer of diagnostic tests, equipment, and services for the veterinary, livestock, poultry, dairy, and water testing markets. Idexx has a presence in over 175 countries around the world.

With about a 70% share of the US pet diagnostic test market, it has a big paw print – not just in providing both common and specialty tests, but also in creating the hardware, software, supplies and clinic laboratories used to analyze them.

The company works like a “razor and blade” model. Once a veterinary practice has invested in a piece of IDEXX equipment, it must purchase the consumables from IDEXX as well. This results in a healthy flow of recurring revenue.

Of the US$2.4bn in revenue that the company reported in 2019, a massive 89% of it is recurring in nature, coming from its large installed base of VetLab equipment.

Idexx is already a top dog in its field but there is a potential for it to run even further ahead of the pack as it moves more equipment from reference labs into vet offices, stretches out internationally, and introduces new products.

Big Fish in a growing pond

For most owners, pets are another member of the family – ones we like to stay with us as long as possible. That bond is the foundation of a health care system very different from its human counterpart. Veterinary devices and diagnostics are largely unregulated, giving innovators the ability to move quickly.

Veterinary care is driven by cash payment and owners tend to give their pets great care even in economically lean times. The dynamics of this system favor for a nimble and strong leader with a knack for staying ahead of the market.

While COVID-19 has introduced some uncertainty on companion animal clinical visits due to stay-at-home policies implemented, the long-term outlook of this market is undoubtedly a growing one.

According to the company’s estimate, the companion animal diagnostic testing market will grow at a CAGR of 8% from 2018 to 2043, with the market worth US$29bn by the end of the forecast period vs. current level of close to just US$4bn. Idexx has consistently grown faster than this background rate, with revenue climbing at an average annual pace of 10.7% over the past 3 years and earnings per share rising by 14.1% a year, thanks to improving margins and stock buybacks.

One of the reasons Idexx can stay on this growth path and continue delivering market-beating returns is that it is providing a win-win for vets, pet owners, and ultimately shareholders.

Mega Innovator

Idexx has been an innovator in creating new products for the pet health care market. The company previously estimates that its research budget represents about 80% of all global R&D that goes into companion animal diagnostics. As a result, Idexx is way ahead of the competition in terms of tests, instruments, and service.

Within 8 years, the company has developed 8 new different test equipment for the different organs and diseases such as tests for diabetes, inflammation, kidney, thyroid, and the latest being the liver.

Vets love this for a few reasons. New tests mean new services they can offer customers and better care for animals. Diagnostic represent about 15% of revenue for the typical vet and best practices, that figure should hit approx. 25%. Moreover, getting results quickly, thanks to in-house analyzers like Idexx’s Catalyst One system, means they can give feedback to owners instantly. That in turn means better compliance with follow-up treatment.

The company also continues to find new customers. According to their analysis, they estimate 72,500 additional worldwide catalyst placement opportunities, with the majority coming from international expansion.

Idexx’s Business Analysis

Before beginning out price analysis, there are 9 questions that one would have to ask on the company’s business operations:

Does the company have any identifiable consumer monopolies or brand name products?

According to Idexx, the company is the largest spender among its peers in terms of R&D investment. This consistent investment in innovation creates a growing proprietary competitive gap between themselves and peers, thus driving growth for the organization.

Based on a 2017 report by Technavio, Idexx is one of the top 5 veterinary diagnostics market vendors in the world. The other 4 players are Abaxis, Heska, Thermo Fisher Scientific, and Zoetis. Zoetis acquired Abaxis back in Mid-2018 and is currently the largest producer of medicine and vaccinations for pets and livestock.

So based on market cap, the company is likely ranked No.3 in this industry, behind both Thermo Fisher Scientific (much broader business scope) and Zoetis.

The brand of Idexx is well-known within the veterinary diagnostic industry.

Is the company conservatively financed?

The company has about USD$1 billion in terms of debt on its balance sheet. Given that its equity is negative (similar to McDonald and Disney which we have previously analyzed using this same methodology), the usage of the debt-equity ratio is not very meaningful.

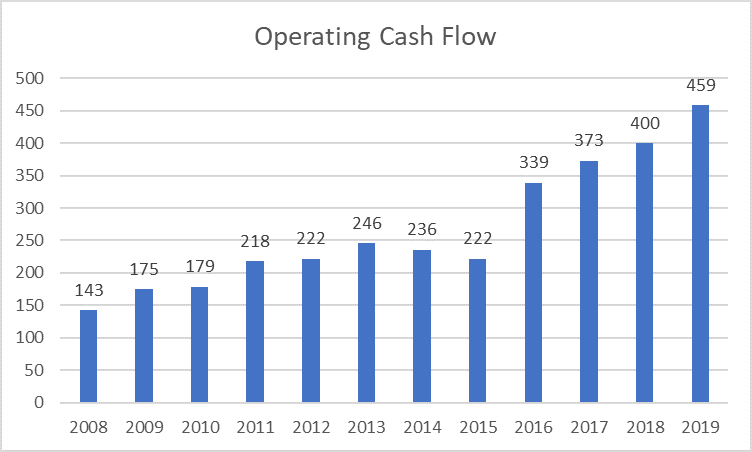

What is more meaningful is looking at the amount of operating cash flow that the company generates each year. That has been showing a very consistent uptrend alongside profit growth, the ideal scenario we will like to observe.

Based on its operating cash generation profile, it will take the company only 2 years to cover all its debt obligations.

Hence, I do not foresee any debt-related issues for the company

Are the earnings strong and do they show an uptrend?

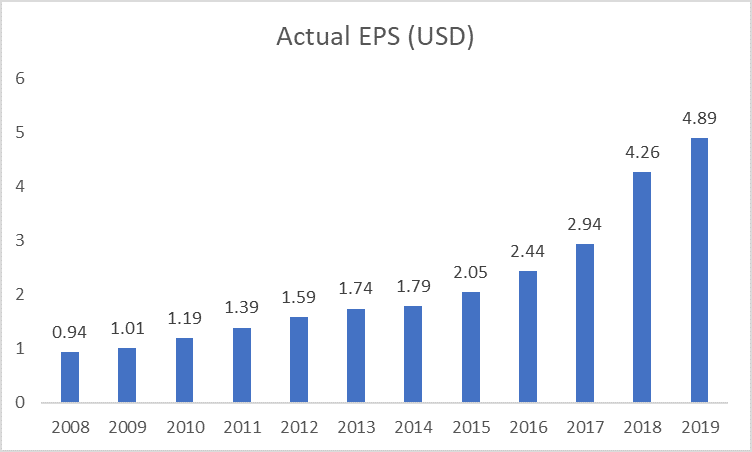

The earnings of Idexx are extremely impressive, to say the least. That is, in fact, the very reason that caught our attention and have us investigate the company a little further.

Its EPS has grown every single year for the last 10-years. It has been growing every year for the last 15-years. An extremely impressive feat. No wonder the company is trading at 60+x PER. A good company ain’t cheap in this case.

Is the company allocating capital to its realm of expertise?

The company is one of the market leaders when it comes to allocating resources towards expanding its proprietary knowledge vs. its competitors. This could be a double-edged sword, one which requires constant R&D spending to stay ahead of the game.

In the case of Idexx, its strong operating cash profile affords the company the luxury to reinvest its capital into relevant proprietary knowledge that will remain with the company for a long time.

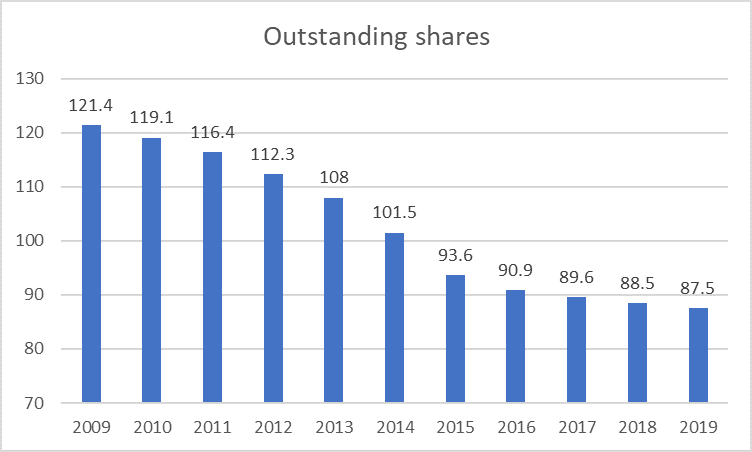

Is the company doing share buybacks?

Shares outstanding reduced from 121m back in the end-2009 to 87.5m in end-2019. So yes, while the company does not pay a dividend, it is returning its capital to shareholders indirectly in the form of active share buy-backs.

However, given the elevated price of the company, share buyback activities might start to taper over the coming years. This is unless management believes that the intrinsic value of the company remains well above the current level.

Is the company increasing shareholders’ value?

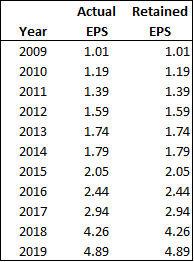

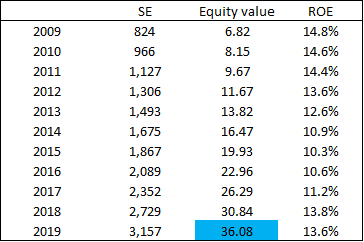

The company has generated a total of USD24.28/share in retained earnings for 2009-2019. During this period, earnings per share (EPS) grew by USD3.88 from USD1.01 as of end-2009 to USD4.89 as of end-2019.

Thus we can argue that the retained earnings of USD24.28/share, produced in 2019 an after- corporate tax return of USD3.88/share, which equates to a rate of return of 16%.

Rate of return = 3.88/24.28 = 16%

This indicates there has been a profitable allocation of retained earnings and a corresponding increase in earnings per share.

This has caused a much larger increase in the market price for Idexx’s stock, from approx. USD16 as of end-FY2008 to USD265 as of end-FY2019. Currently, the share price of Idexx sits at c.USD325.

What is the ROE of the company?

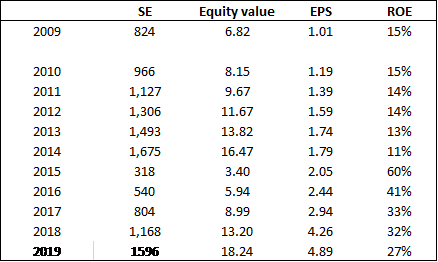

Idexx does not have an ROE figure as its equity is negative due to a significant amount of share buybacks over the years which resulted in the accumulation of treasury shares.

Using retained earnings, Idexx’s ROE is at an elevated level of 27% based on 2019 figures. This is almost double our benchmark of at least 15%.

Is the company free to adjust prices to inflation?

According to management, the company can adjust its price by approx. 2-3% per annum based on the current trend that it is seeing. In total, the company expects its recurring revenue for CAG Diagnostic (the main segment which encompasses c.76% of Group’s revenue) to be increasing at a rate of 11%.

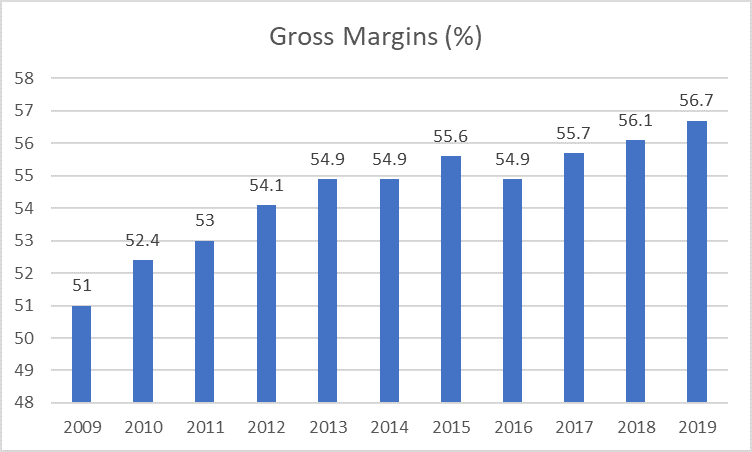

An alternative way would be to look at the company’s gross margins. Idexx’s gross margins have increased from 51% in 2009 to 56.7% in 2019. The improvement in gross margins over this period could indicate a certain level of pricing power.

Do operations require large capital expenditure?

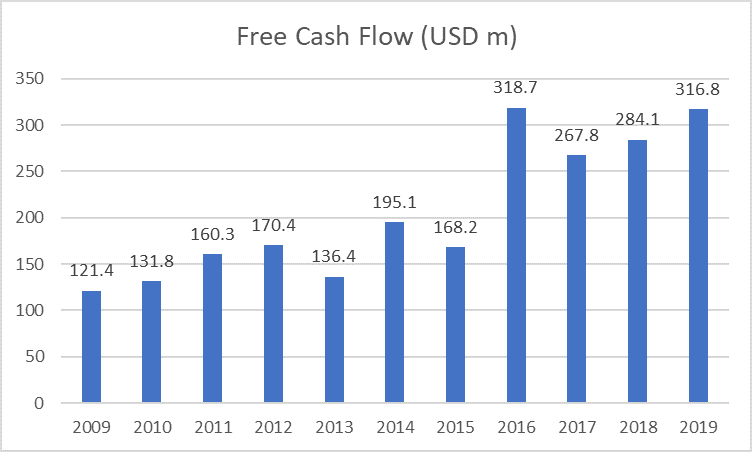

The only significant capital expenditure for the business is R&D related expenses. The company generates strong free cash flow of close to USD$300m each year which offset concerns over high CAPEX resulting in cash flow constraints.

Idexx’s price analysis

Idexx’s current adjusted ROE stands at approx. 27% based on our computation using retained earnings.

We use an adjusted figure of $36.08/share as its equity value based on EPS generated. This differs from the actual equity value as we exclude out the cancellation of treasury shares.

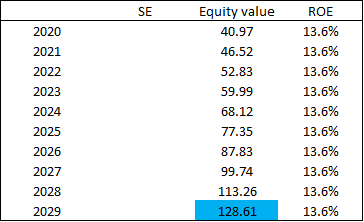

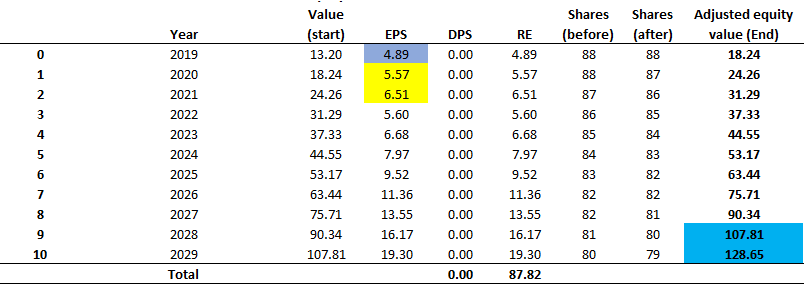

That would have translated to a more normalized ROE figure of approx. 13.6%. We assumed a 13.6% ROE rate over the next 10 years which will translate to an end-2029 equity value of $128.61/share.

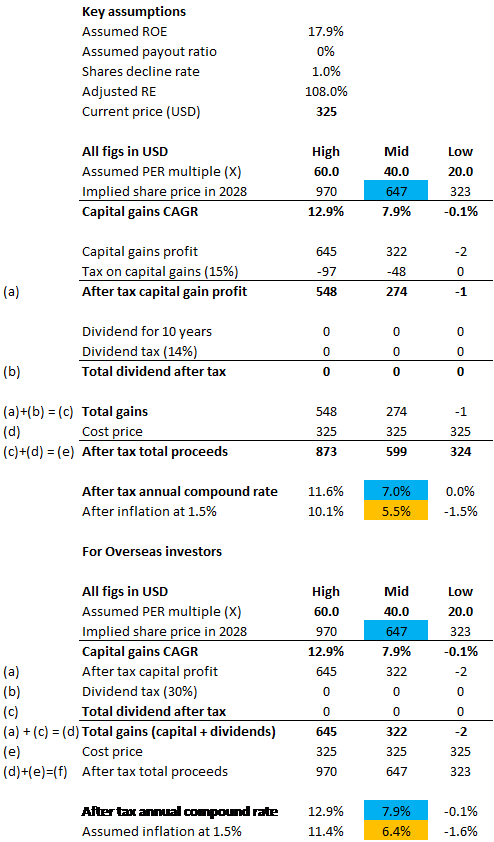

With that end-figure in mind, we work backward to derive a more appropriate ROE figure of 17.9% (using reported shareholder equity figure instead of the adjusted figure).

Based on those numbers, we derived an after-inflation 10-year CAGR of 6.4% for an overseas investor (do not need to pay capital gain tax) based on today’s entry price of USD$325/share.

This is a decline from our previous analysis of 8.7% for an overseas investor and slightly below our required benchmark of 6.5%

This is based on a PER assumption of 40x PER. If the company can maintain a 60x PER, that compounded return would be closer to 11.4% for an overseas investor and 10.1% for a US investor. An attractive return using those multiples.

Conclusion

I like Idexx for its resilient business nature, one that might be affected due to COVID but its long term outlook remains bright, especially for a business that has close to 90% of its turnover on a recurring nature basis. That increases earnings visibility and gives us more confidence that its earnings forecast will not deviate significantly from our internal assessment.

Nonetheless, its current share price does not leave much room of error and I will be looking for a price pullback for a more progressive entry.

Do Like Me on Facebook if you enjoy reading the various investment and personal finance articles at New Academy of Finance. I do post interesting articles on FB from time to time which might not be covered here in this website.

Join our Telegram broadcast: https://t.me/gemcomm

SEE OUR OTHER WRITE-UPS

- 1Q 2020 TOP HEDGE FUND LETTERS TO SHAREHOLDERS

- 8 OUTPERFORMING STOCKS TO BUY NOW (PART 2)

- 8 OUTPERFORMING STOCKS TO BUY NOW (PART 1)

- 4 RECESSION-RESISTANT STOCKS WITH A FORTRESS BALANCE SHEET

- 4 STOCKS WITH MORE THAN 80% RECURRING REVENUE OWNED BY GURUS

- A LIST OF “BEST” DIVIDEND GROWTH STOCKS

Disclosure: The accuracy of the material found in this article cannot be guaranteed. Past performance is not an assurance of future results. This article is not to be construed as a recommendation to Buy or Sell any shares or derivative products and is solely for reference only.