Singapore Blue Chip Stocks with notable upgrades/downgrades by analysts

Can we trust analysts’ reports? Throughout the years, we occasionally see analysts flip-flopping between buy and sell calls within several weeks. As investments are highly subjective to one’s view, the difference in perspective is understandable. However, it led to certain controversies as investors argue that there may be a hidden agenda behind them.

A recent example would be in March 2021 when the market was hit with fears of higher interest rates. I recalled analysts at JP Morgan issuing an “underweight” position on both S-REITs and industrial REITs. This fuelled the fear in investors and caused a further sell-off in REITs. However, some investors saw it as an opportunity to “buy the dip” and the counters such as Mapletree Industrial (SGX: ME8U) swiftly rebounded by 7% the following week!

Analyst reports provide you with a useful source of information but investors should not solely rely on them to make investment decisions! In this series, we’ll look to analyze three Singapore blue chip stocks upgrades and downgrades made by analysts in the month of May.

Is there an early opportunity to invest in these gems? I will look to provide a quick summary of the rationale behind the upgrades or downgrades made to these stocks by the respective brokerage houses as well as chip in with my own 5 cents view.

Singapore Blue Chip Stocks to Watch for May

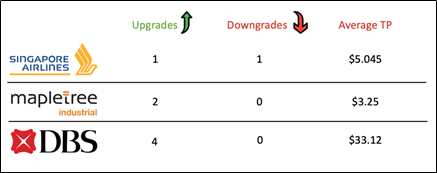

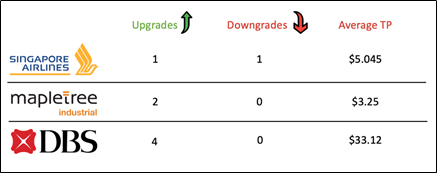

For our May pick, these are the stocks that we will be analyzing – Mapletree Industrial (SGX: ME8U), Singapore Airlines (SGX: C6L), DBS (SGX: D05). This is a quick summary of the analyst buy and sell calls for the month of May. As shown in the picture below, most counters scored well but I was most intrigued by CIMB’s “Add” call to Singapore Airlines.

Here’s our breakdown of the analyst reports:

Singapore Blue Chip Stock to Watch #1: Singapore Airlines (SGX: C6L)

Quick Introduction to the Singapore Airlines

Our nation’s carrier is no stranger to Singaporeans and they operate in one of the worst-hit industries due to Covid-19. With three carriers under its name – SIA, SilkAir, and Scoot, it magnifies the impact of the pandemic. To cushion the financial burden, the company sold and leaseback its aircraft while announcing its second round of funding via mandatory convertible bonds (MCB).

Here is a quick summary of the company:

Financial Performance

Reported a record net loss of S$4.3billion for the last financial year, comprising of a S$214million loss on fuel hedging ineffectiveness and derivatives

Passenger traffic

- Passenger traffic plummeted by 97.9% due to global restrictions on travel

- Passenger revenue declined by 94.7% year on year

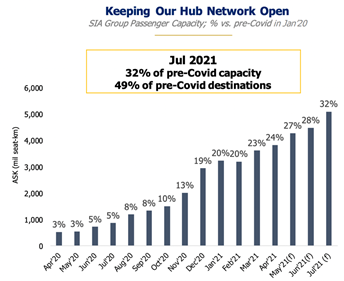

- The carrier is expected to reach 32% of its pre-covid capacity by July 2021

Cargo Traffic

- This was the only positive for SIA as they leveraged on high cargo demand

- Revenue increased by 38.8% year on year.

Recent Upgrades / Downgrades by Analysts

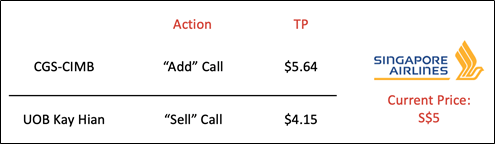

For the month of May, there are two contrasting analyst reports for Singapore Airlines.

With a large monthly cash burn of S$100million to S$150million, uncertain travel outlook, and high debt levels, I was personally surprised by CIMB’s “Add” call! In the next section, we’ll analyze the key rationale of the analysts.

Key Rationale of Analysts and My Views

Cash Burn

Both analysts were positive about the considerable reduction of SIA’s monthly cash burn since the start of the pandemic. From S$350million last year, the figure was reduced to S$300million by September 2020, and further cut to S$250million by February. Today, the cash burn is reduced to a figure between S$100million to S$150million.

On this front, CIMB appears to be more optimistic. Barring some one-off factor, they believe that SIA should be able to move in the right direction. However, UOB Kay Hian sees a potential upward reversion of cash burn due to a possible reduction of grants or delay in the opening of borders.

Strong Access to Capital

Unlike many other airlines that went under due to the effects of Covid-19, SIA has strong access to capital in both the debt and equity markets. The prominent funding includes:

- June 2020 – Raised S$8.8billion of equity capital comprising of a rights issue and MCB

- May 2021 – Announced an additional S$6.2billion of MCBs

With Temasek’s commitment to subscribe on a pro-rata basis and taking up any public shortfall, SIA will certainly be able to receive the necessary funding. Despite poor financing showing, SIA’s cash balances rose from S$2.7billion in March 2020 to S$7.8billion in March 2021. Net gearing of the firm also fell from 98% to 41% on a year-on-year basis as of March 2021. The healthy cash level will provide SIA with some breathing space to navigate through the pandemic.

Valuation

Although both the right issue and Mandatory Convertible Bonds (MCB) provide SIA with certain headspace, it is also highly dilutive to shareholders. As for the latter, it will be converted to ordinary shares (for S$4.84) on 8 June 2030 unless redeemed by the company. The key difference between the analyst reports rests heavily on the perception of the MCBs.

CIMB’s View:

They believe that SIA will redeem half of the MCB before 2030 or refinance through other alternatives. Further, they omitted the increase of shares in the derivation of SIA’s target price as conversion will only take place in 2030. At the moment, any access to cash is an advantage and 9 years is beyond the decision-making horizon of many investors.

As SIA’s BVPS comes at an average of 0.93x since 2011, CIMB values the firm at a P/BV of 1.06x which is +1 s.d. above the mean. This is due to the analyst’s optimism towards international travel which amounts to their target of S$5.64 per share.

UOB Kay Hian’s View

Conversely, UOB carried a lower degree of optimism towards SIA’s operations. Instead of factoring half of the MCB, they factored in annual dilution from the accrued interest of the bonds. Instead of valuing the firm at PV/B of 1.06x, UOB is valuing it at 1x PV/B which amounted to S$4.15 per share.

Will I buy SIA?

I agree with UOB’s view which carried a lower degree of optimism towards the aviation industry. Unlike many other international airlines, SIA does not have any domestic flights to rely on and has to depend on the resumption of international travel. The International Air Transport Association (IATA) forecasted 2021’s air traffic to only be 52% of 2019’s level. Air traffic is only expected to recover fully in 2023 which will be a painful and expensive wait for SIA.

Due to the recent uptick of Covid-19 cases in the region, SIA has also seen green lanes being suspended. The outlook of the industry is highly unpredictable and I believe that the market can sometimes stay irrational longer than investors can stay solvent. With the dilution of shareholdings, instead of investing in SIA, I will look to take profits and divest my holdings if I’m an investor.

Singapore Blue Chip Stock to Watch #2: Mapletree Industrial (SGX: ME8U)

Quick Introduction to the Mapletree Industrial

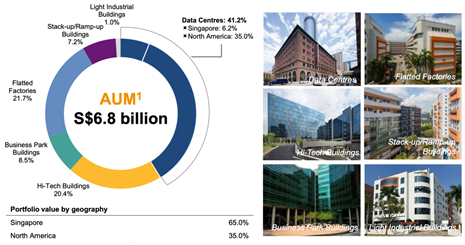

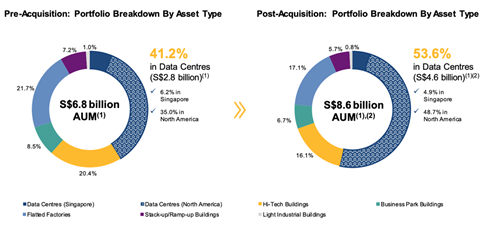

Mapletree Industrial is a large-cap S-REIT and the third-largest industrial REIT listed in Singapore. Backed by Mapletree Investments – wholly owned by Temasek, Mapletree Industrial has an Asset Under Management (AUM) of S$6.8billion in 115 properties across 6 segments. Despite Covid-19, the company was able to provide stellar performances. Just several weeks ago, they are looking to raise S$800million to fund their acquisition of data centers.

Here’s a quick summary of the REIT:

Financial Performance

- Performed well amidst the pandemic mainly due to contribution from data centers acquired

- Year on Year increase:

- Distributable income up by 11.3%

- Dividend per unit up by 2.5%

- Performance was slightly tapered down due to S$12.7million in rental relief for FY20/21

Portfolio Performance

- As of Q4 FY20/21, average portfolio occupancy increased quarter on quarter from 93.1% to 93.7%

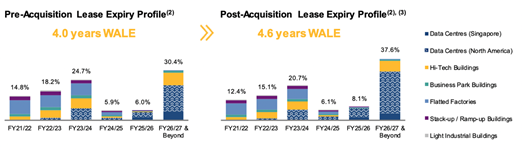

- Healthy portfolio weighted average lease expiry (WALE) of 4 years

- Low tenant concentration as largest tenant contributes to only 7.3% of gross rental income

- Gearing of 40.3%, set to reduce after equity financing.

Acquisitions

- In May 2021, the company announced a USD1.32billion acquisition of data centers in the United States.

- The acquisition is expected to be DPU and NAV accretive on a 60/40 debt-equity structure. Pro-forma DPU and NAV is expected to rise by 3.3% and 6%

Recent Upgrades / Downgrades by Analysts

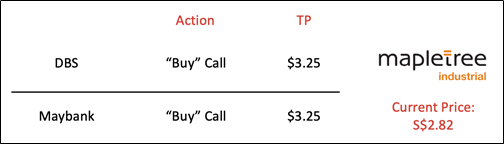

For the month of May, there were two analyst reports on Mapletree Industrial and both issued a “buy” call. In the next section, we’ll analyze the key rationale of the analysts.

Key Rationale of Analysts and My Views

Accretive Acquisition

Unlike recent private placements from its peers, the exercise was a success for Mapletree Industrial with a 3.1x oversubscription from institutions. This is a sign of confidence that retail investors can take with them.

Here are the benefits of the acquisition:

- In line with the REIT’s target to have data centers taking up 2/3 of the portfolio

- Post-acquisition WALE is extended from 4 years to 4.6 years

- Income from top 10 tenants reduced from 33.3% to 30.6%

- Data Centre’s CAGR projected at 9.2%

- The proportion of freehold properties to increase from 55.9% to 65.8% by NLA

- Occupancy of new data centers is at 87.8%, there is considerable room for growth if the manager can deliver.

Prolonged slowdown in economic activity and rise in interest rates

Despite what the acquisition brings to the table, the portfolio’s performance is still highly dependent on economic activity. Any slowdown activity can result in lower occupancy and rental rates. As seen with several local retail malls, any spike in cases or clusters can result in deep cleaning of properties. The uncertainty may dampen the confidence of tenants and hurt rental yields.

Further, any sharper than expected rise in interest rates can increase the cost of debt and lower the earnings of REITs like Mapletree Industrial. With talks from the FED about transitionary inflation, this is expected to put some pressure on the treasury yields.

Should interest rates rise across the board, it might put some pressure on premium REITs such as Mapletree Industrial that already offer a lower yield than its peers.

Will I buy Mapletree Industrial?

At the current price, investing in Mapletree Industrial will provide a dividend yield of 4.5% to 4.6%. Moreover, investors will be paying a P/BV of almost 1.7x at S$2.82 per share which is above the average of 1.36x for industrial REITs. If investors are comfortable with the valuation, I believe Mapletree Industrial is a good investment at the current price. I will be waiting for potential dips before entering this counter.

Singapore Blue Chip Stock to Watch #3: DBS (SGX:D05)

Quick Introduction to the DBS Bank

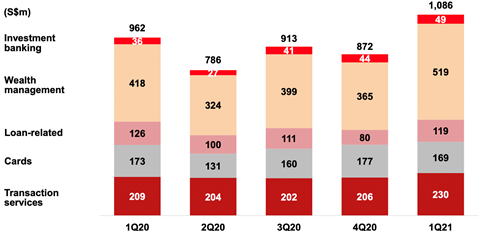

DBS is the largest bank in both Singapore and South East Asia in terms of total assets. Just in 2021 Q1, the bank’s quarterly net profit crossed the S$2billion mark for the first time outperforming the $1.44billion expectation from analysts. The bank’s earnings were predominately boosted by writebacks which resulted in only S$10m in impairments for the first quarter. Here’s a quick summary of the bank:

A surge in Non-Interest Income

- Fees income grew by 15% quarter-on-quarter due to an increase in wealth management and transaction fees.

- Other non-interest income grew by 101% quarter on quarter with an increase in customer flow

Net Interest Margin (NIM)

- Margins stabilized and loans grew by 4.1% for the bank on a quarter on quarter basis

- Non-performing loans dropped to 1.5% for DBS, showing signs of economic recovery

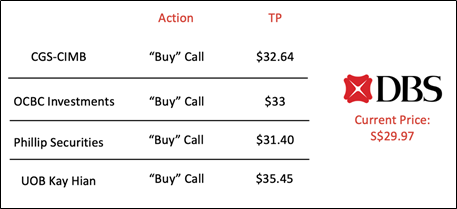

Recent Upgrades / Downgrades by Analysts

For the month of May, there were four analyst reports on DBS that issued a “buy” call. In the next section, we’ll analyze the key rationale of the analysts.

Key Rationale of Analysts and My Views

Improving Economic Outlook

Banks are set to capitalize on the improving economic outlook with the re-opening of economies and the global vaccination exercise. In Q1 2021, Singapore’s economy grew at its fastest quarter-on-quarter rate of 1.3%. With other advanced economies registering strong growth, banks are also bullish on the economy and raised their loan growth forecasts. Coupled with their growing non-interest income, the outlook for banks is rather positive.

Some central banks are also beginning to pull back their bond purchases which will increase the treasury yields. As per UOB’s report, countries such as the UK will be reducing their bond purchase programs. A higher treasury yield will benefit banks as interest income will increase in tandem.

Uneven Pace of Recovery

With the uncertainty surrounding Covid-19, banks have also acknowledged an uneven economic recovery. With the recent rollback of Phase 3 in Singapore, any movement restrictions can have a direct impact on the asset quality of banks. On the extreme end, any further waves of Covid-19 can also result in government intervention such as loan forbiddance or higher provisions.

Will I buy DBS?

I believe DBS is at the forefront of digitalization and they have been aggressively expanding through acquisitions in China and India. If I were to invest in a Singapore Bank, DBS will be my choice of investment. However, with the recent developments regarding Covid-19, I believe that the MAS’ dividend cap may be eased gradually but not anytime soon. At the current price, dividend yield stands at 2% and there might be better investments in the market.

However, Piyush Gupta, the bank’s CEO has been warning investors about an upcoming market crash since last year. Furthermore, he sold S$11million worth of stocks in May which is never a good sign for a company! With this, I’ll wait for a market dip before investing in DBS.

Conclusion

Among the 3 Singapore Blue Chip Stocks to watch this month, with significant changes in analysts’ calls, I believe that SIA is the most controversial one. Despite record losses announced for 2020 and a recent fundraising in the form of the second tranche of MCBs, the stock is still hovering near its all-time high price. This seems rather perplexing and the only rationale reasoning is that the street believes that SIA will have unwavering financial support from the government to tide it through the COVID-19 crisis, even if the global travel recovery might take much longer vs. initial expectations.

From a trading angle, I believe that Mapletree Industrial Trust might be worth a closer look although now might not be the ideal time. I earlier highlighted that I will be buying the counter on dips as I hold a long term positive view on the stock but from a trading perspective, the stock is not yet demonstrating the positive momentum that I will like to see as shown by the TradersGPS system.

![3 Singapore Blue Chip stocks to watch [May 2021] 1](https://newacademyoffinance.com/wp-content/uploads/2021/05/image-210-1024x558.png)

The TradersGPS system is a proprietary system developed by Collin Seow and his team and allows one to easily identify trending stocks to enter in the early stage. For example, it is likely a tad too late to be entering DBS from a trading angle currently, with the system providing an early entry signal back in late March 2021 to enter at a price of around $28.74, translating to a c.10% return if held till now.

![3 Singapore Blue Chip stocks to watch [May 2021] 2](https://newacademyoffinance.com/wp-content/uploads/2021/05/image-211-1024x552.png)

For those who are interested in checking out the TradersGPS system and its respective Systematic Trading Course which is voted the No. 1 investing course by users in a Seedly review, do check out the FREE online session by clicking on the link below

Click on the link to find out more.

Do Like Me on Facebook if you enjoy reading the various investment and personal finance articles at New Academy of Finance. I do post interesting articles on FB from time to time which might not be covered here in this website.

Join our Instagram channel for more tidbits on all things finance!

SEE OUR OTHER WRITE-UPS

- Motley Fool review: Getting multi-bagger ideas the easy way

- Hang Seng Tech Index: A deep dive into the hottest tech stocks of Asia

- Best Stock Brokerage in Singapore

- Syfe Equity100 review: Does this portfolio make sense to you?

- Tiger Brokers review: Possibly the cheapest brokerage in town. Is it right for you?

- FSMOne Singapore: Step-by-step guide to open your FSMOne account and start trading

Disclosure: The accuracy of the material found in this article cannot be guaranteed. Past performance is not an assurance of future results. This article is not to be construed as a recommendation to Buy or Sell any shares or derivative products and is solely for reference only.