Brief background summary

By now, most of you would probably have been aware of Singapore Airlines’ (SIA) plight and the need to do a massive fund-raising exercise, fully-backed by Temasek. This means that if Singaporeans are not willing to support our national carrier by subscribing to those new shares, Temasek will come in to backstop 100% of the issue.

SIA looks to raise a total amount of S$15bn (SIA Rights), through a combination of S$5.3bn in Rights Shares issuance and S$9.7bn via Rights mandatory convertible bonds or MCB for short.

S$15bn looks like a HUGE amount of equity to be raised, particularly when one compares with SIA’s key competitor Qantas which, a few days prior to SIA’s announcement, highlighted that it has managed to secure ONLY A$1.05bn in collateralized (against its fleet of 7 Boeing 787 aircraft) debt funding at an interest rate of 2.75%. Qantas share price appreciated by 26%.

Unlike SIA which has been levering up on its balance sheet to make new aircraft purchases, Qantas, on the other hand, has maintained a steady net debt balance of A$3bn over the past 3 years. Comparatively, SIA’s net debt balance has ballooned to S$8bn (including lease liabilities) as at end-2019 as a result of their aggressive fleet renewal plan.

So, Qantas (with a market cap of A$5bn) requires an additional A$1bn to tide over this major aviation crisis (for now perhaps) while SIA (now with a market cap of S$7bn) requires a potential total of S$15bn (plus S$4bn in bridging loan) and one can see the huge disparity in terms of capital management.

With that notion in place, let’s evaluate the two Rights issuance, first the SIA Rights Share followed by the SIA Rights Mandatory Convertible Bonds.

I will then follow up with 4 scenario analysis for a potential SIA shareholder and calculate what might the market value of the SIA Rights Shares and SIA Rights MCBs be worth when they start trading.

Scenario 1: Bought SIA at S$5.80 and subscribe for Rights Shares

Scenario 2: Bought SIA at S$5.80 and subscribe for Rights MCBs

Scenario 3: Bought SIA at S$5.80 and subscribe for Rights Shares + Rights MCBs

Scenario 4: Purchase Rights Shares and Rights MCBs on the open market

Issuance of SIA Rights Shares

SIA will be issuing up to 1.78bn rights shares at an issue price of S$3.00 for each right shares.

This is on the basis of three (3) Rights Shares for every two (2) existing ordinary shares in the capital of the company. As of end-2019, SIA has got 1.18bn outstanding shares (excluding treasury shares), so the calculation is (1.18bn/2 ordinary shares * 3 rights shares = 1.78bn new right shares)

At S$3/rights shares, this is a 53.8% discount to the last transacted price of S$6.50 before the announcement was made. The calculated theoretical ex-rights price (TERP) is S$4.40 per share.

How does one calculate the theoretical ex-rights price? At S$6.50/share with 1.18bn of outstanding shares, the market cap of SIA is S$7.67bn.

With the issuance of 1.78bn rights shares, total number of shares will increase to 2.96bn. Total amount of capital raised = 1.78bn * S$3.00 = S$5.34bn

So post rights issuance market value of SIA = (existing market cap (S$7.67bn) + new cash raised (S$5.34bn)) / total number of new shares (2.96bn) = S$4.40/share.

These rights will be renounceable. This means that existing SIA shareholders can actually sell their rights on the open market if they do not wish to pay S$3.00/share to subscribe to it. This will, however, mean dilution to the shareholder. How much can they sell for? We will touch on this later.

With that, let’s move on to the Rights MCB which is slightly a little more complicated.

Issuance of SIA Rights MCBs

SIA plans to raised c.S$3.5bn from the first tranche of Rights MCBs. If insufficient, the company could raise a further S$6.2bn to bring the total Rights MCBs amount to S$9.7bn!

The Rights MCBs are proposed to be offered, also on a renounceable basis, and issued in the denomination of S$1.00 for each Rights MCB, on the basis of 295 Rights MCBs for every 100 existing ordinary shares.

These Rights MCBs pay zero-coupon and will mature on the 10th anniversary year of the date of issue. When they mature, these Rights MCBs will be converted into shares.

However, the catch here is that there is no certainty that SIA will convert these Rights MCBs into shares upon maturity as there is an option for them to redeem the Rights MCBs in whole or in part on every six-month anniversary of the issue date. More on this later.

Given that there are 1.18bn ordinary shares, the total number of Rights MCBs will be equal to 3.48bn (1.18 existing ordinary shares / 100 * 295). At S$1 each, the total amount of gross proceeds will be equal to S$3.48bn.

So what happens after 10 years when the Rights MCBs mature?

S$1,000 invested in the Rights MCBs will grow into S$1,806.11, according to SIA’s calculation. This translates to a 10-year CAGR of 6.09%. A YTM of 6.09% looks pretty attractive but this return is NOT Guaranteed

The amount of S$1,806.11 will translate to 373 shares, based on a conversion price of S$4.84/share as mandated by SIA (S$1,806.11 / S$4.84/share = 373 shares). Your cost price is the S$1,000 you have paid / 373 shares = S$2.68/share.

You make a return of 6.09% per annum if SIA’s share price is at S$4.84 on maturity while you breakeven if the share price is S$2.68 on maturity and you start losing money if SIA’s price is below S$2.68 on maturity.

In this Rights MCBs exercise, every S$1,000 raised (a total of S$3.48bn will be raised) will translate to 373 shares upon maturity.

This means that a total of S$3.48bn/S$1,000 * 373 shares = 1.3bn shares will be raised from the Rights MCBs.

Recall two things: 1. The total number of shares from Rights Shares = 2.96bn and 2. Total number of shares from Rights MCBs = 1.3bn

Total number of shares after all conversion = 2.96bn + 1.3bn = 4.26bn shares.

So after this whole exercise, SIA will raise a total of S$5.34bn (Rights shares) + S$3.48bn (Rights MCBs) = S$8.8bn. With a current market cap of S$7bn (at S$5.80), which brings the total value of SIA to S$15.8bn. The theoretical ex-rights price after all conversion = S$15.8bn / 4.26bn shares = c.S$3.68

Scenario analysis to calculate the ex-rights price for each scenario

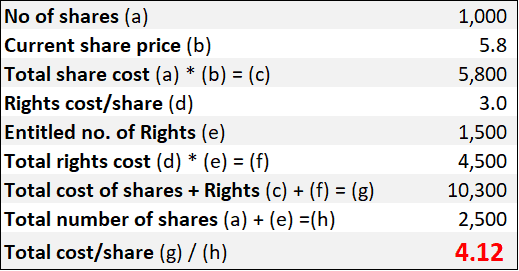

In the scenarios 1-3, we will assume that 1,000 shares of SIA were purchased at the current market price of S$5.80. This will entitle the investor to 1,500 Rights Shares and 2,950 Rights MCBs.

Scenario 1: Purchase SIA shares at S$5.80 and subscribe for Rights Shares

Based on the current market cap of S$7bn or at S$5.80/share, the theoretical ex-rights price will be closer to S$4.12/share. This means that when the rights are being issued to eligible shareholders, we should expect SIA’s price to fall closer to the S$4.12 level if the current price of S$5.80 holds.

See the table below for the calculation. We ignore the Rights MCBs in this scenario although there will be a market value for it.

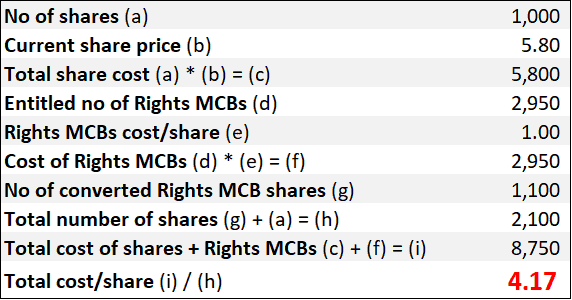

Scenario 2: Purchase SIA shares at S$5.80 and subscribe for Rights MCBs

What if the SIA shareholder decides to forgo his Rights Shares (again we ignore its market value) and just exercise his Rights MCBs?

The table below calculates the theoretical ex-rights price. That figure comes out to S$4.17 which is slightly higher than that of Scenario 1.

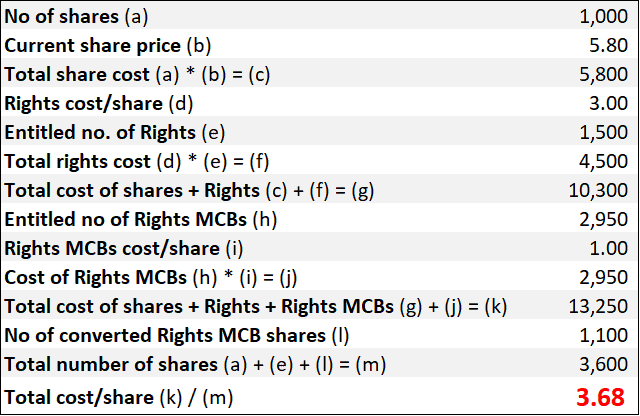

Scenario 3: Purchase SIA shares at S$5.80 and subscribe for both Rights Shares and Rights MCBs

Again, we use the table below as an illustration.

In this scenario, we see that the ex-rights cost of SIA is the lowest at S$3.68 as we have previously highlighted above based on S$15.8bn as the total SIA value / 4.26bn share base = S$3.68.

It seems to make sense for an SIA investor to subscribe to both rights. However, we have ignored the potential income from the sale of both rights which will go towards reducing the ex-right cost of Scenario 1 and 2.

We can see in Scenario 3 that for 1000 SIA shares, the investor is entitled to 1,500 Rights Shares and 2,950 Rights MCBs.

Back to Scenario 1, if he is only subscribing to the 1,500 Rights Shares and selling the 2,950 rights MCBs, his total cost will be S$10,300 or S$4.12/share (based on 2,500 shares). How much do his 2,950 Rights MCBs need to be sold for such that it brings down his cost per share to S$3.68?

The answer is: (S$10,300 – (S$3.68 * 2,500 shares)) / 2,950 shares = S$0.37/Rights MCB.

[Update]: A reader has highlighted that the S$0.37/Rights MCB does not make sense which I concur on second thoughts. It does not make sense for an investor to purchase each right MCB for S$0.37, pay S$1 to convert it for a total cost of S$1.37, and risk having the MCB being bought back by SIA at S$1.02, 6 months later. It is highly likely that the cost of the Rights MCB is closer to zero.

Similarly for Scenario 2, if he is only subscribing to the 2,950 Rights MCBs and selling the 1,500 Rights Shares, his total cost will be S$8,750 or S$4.17/share (based on 2,100 shares). How much do his 1,500 Rights Shares need to be sold for such that it brings down his cost per share to S$3.68?

The answer is ($8,750 – (S$3.68 * 2,100 shares)) / 1,500 shares = S$0.68/Rights Share.

Scenario 4: Subscription of Rights Shares and Rights MCBs on the open market

We know that the exercise price of a Right Share is S$3.00. Let say if there is minimal market value to the Right Share (S$0.10), an investor can purchase this Right Share at S$0.10 and exercise it at S$3.00 for a total cost of S$3.10.

This will be like an arbitrage. However, we have calculated that a Right Share is worth S$0.68 in the market. Total cost will hence be S$3.00 (exercise price) + S$0.68 (market price) = S$3.68

[Update] The rights price will be dependent on what the mother share is trading at that point in time. S$0.68/rights is assuming that SIA price remains at its calculated ex-right price of S$3.68.

This will bring it to parity with Scenario 3.

Likewise, for a Rights MCB, it will be worth S$0.37 each. At an exercise price of S$1/Right MCB, the total cost will be S$1.37. However, since its not a 1 for 1 conversion rate (Note: we previously calculated that 2,950 Rights MCB will translate to 1,100 shares upon maturity). We need to multiply it by the ratio of 2950/1,100 * S$1.37 to get a value of S$3.68.

So if the price of SIA remains around S$5.80/share, I will expect each Right Share to be trading at c.S$0.68 while each Rights MCB to be trading at S$0.37.

Option for SIA to redeem Rights MCBs

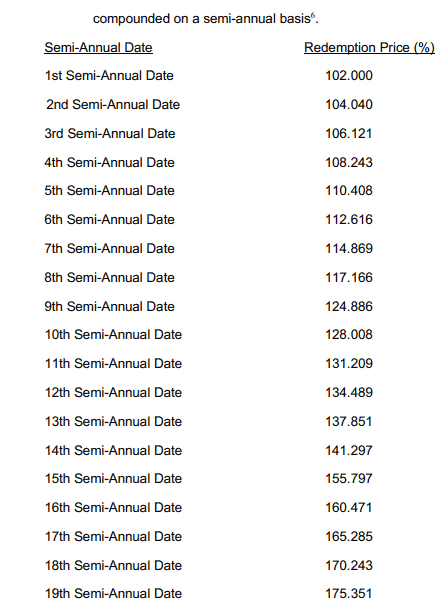

The Rights MCBs will mature after 10 years. However, during this 10-year period, the Rights MCBs may be redeemable at the option of SIA in the whole or in part on every six-month anniversary of the issue date at the relevant accreted principal amount as at such semi-annual date.

The Yield to call is 4% for the first 4 years, increasing to 5% for the next 3 years and for the last 3 years, it will be at 6%. Hence you can see that there is a spike on the 9th semi-annual date and the 15th semi-annual date above. We have calculated previously that the YTM is at 6.09%.

What will incentivize SIA to exercise its call option?

The cost of funding for this Rights MCBs is theoretically at 6.09% if held to maturity. If the overall operating environment improves and SIA can get a cheaper source of bank funding, say at 2.5%, then it might make sense for SIA to “lever” up and pay back the Rights MCB holders.

By exercising its option to redeem, SIA will need to cough out the principle * redemption price amount.

Say, for example, assuming SIA decides to redeem the Rights MCBs on the 10th semi-annual date, the company will need to fork out S$3.48bn * 128.008 = S$4.45bn. While this might be a significant upfront cost for SIA, the “total cost”, if held to maturity, would be S$3.48bn * 1.806 = S$6.28bn (not cash cost).

By refinancing it after 5 years with bank borrowing at 2.5% interest/annum, the total cost savings is S$6.28bn – S$4.45bn – (S$4.45bn * 2.5% * 5 years) = S$1.27bn. This will also prevent further dilution of the shareholding base upon the 10th year maturity.

If SIA’s share price appreciates significantly from Year 0 to year 10, say to S$5/share, the total VALUE of the 1.3bn converted shares (from the Rights MCBs) will be equivalent to S$6.5bn. This will be more than the max value calculated above at S$6.28bn.

As such, there will be an incentive for SIA to “call back” the Rights MCB.

How does this fund-raising exercise impact SIA’s gearing level?

SIA’s net debt stood at approx. S$8bn as of end-2019. With an equity base of S$12.5bn, the net debt to equity ratio is 0.64x which doesn’t seem overly “excessive” to start off with. However, the company was in a net cash position just 2 years ago and with over S$20bn in “committed Capex” for fleet expansion, the company’s net gearing will continue to climb.

With the latest fund-raising exercise, the company would have raised an initial capital amount of S$8.8bn, bringing SIA into a slight net cash position. Its equity base will also increase to c.S$20bn (from the current S$12.5bn due to cash addition).

However, with a projected Capex commitment of close to S$24bn over the coming 5 years (assuming they are not being deferred or canceled), it is not surprising that SIA might have to raise additional capital ahead, either through the next tranche of Rights MCBs or increases its bank borrowings.

The company will also need to aggressively reduce its variable cost.

Having said that, I believe the near-term credit risk of SIA is now significantly alleviated. Post this equity raising exercise, the company will still have an additional S$6.2bn in Rights MCB to tap on (but that could mean more dilution).

Net gearing post this exercise will drop to zero and even if the company needs to gear up further, it can still get the support of its bankers, potentially to the tune of S$20bn before hitting the net gearing level of 1.0x.

The key concern right now which the market has is SIA’s cash burn at almost zero passenger revenue. Revenue will not be at zero for the Group as there will still be Cargo revenue (approx. 11-13% of Group’s revenue) which is now benefitting significantly from higher freight charges.

Conclusion

Post these two rights exercises, SIA will see its total outstanding share base increase from 1.18bn to 4.26bn, assuming the conversion of Rights MCBs upon 10th-year maturity.

The NAV of SIA, currently at S$10.25/share as at end-2019, will drop to S$5/share after the increase in share base.

At a share price of S$5.80/share, SIA is trading at a PBR of 0.57x currently. On our theoretical ex-rights price of S$3.68, the counter will be trading at a PBR of 0.74x.

There might be significant price discrepancy to capitalize on when the Rights Shares and Rights MCBs start trading. Do note that my calculation above is just for your reference and there is no guarantee of its accuracy.

Do Like Me on Facebook if you enjoy reading the various investment and personal finance articles at New Academy of Finance. I do post interesting articles on FB from time to time which might not be covered here in this website.

Join our Telegram broadcast: https://t.me/gemcomm

SEE OUR OTHER WRITE-UPS

- DIVIDENDS ON STEROIDS: A LOW-RISK STRATEGY TO DOUBLE YOUR YIELD

- STASHAWAY SIMPLE. CAN YOU REALLY GENERATE 1.9% RETURN?

- WHY I AM STILL BUYING REITS EVEN WHEN THEY LOOK EXPENSIVE

- TOP 10 FOOD & BEVERAGE BRANDS. ARE THEY WORTHY RECESSION-PROOF STOCKS?

- THE BEST PREDICTOR OF STOCK PRICE PERFORMANCE, ACCORDING TO MORGAN STANLEY

- TOP 10 HOTTEST STOCKS THAT SUPER-INVESTORS ARE BUYING

Disclosure: The accuracy of the material found in this article cannot be guaranteed. Past performance is not an assurance of future results. This article is not to be construed as a recommendation to Buy or Sell any shares or derivative products and is solely for reference only.

3 thoughts on “SIA Rights issue: Debunking the complication behind the maths”

I think your scenario “ SCENARIO 3: PURCHASE SIA SHARES AT S$5.80 AND SUBSCRIBE FOR BOTH RIGHTS SHARES AND RIGHTS MCBS” is incorrect in the sense that mcb shares are not acquired now but rather 10 years later.

If you ascribe a value of 0.38 to each mcb right to get a present cost base of 3.68, the effective return is 2.5% at the end of 10 year assuming 4.84 terminal.

I will posit that the tangible value of the mcb right is currently near null and it increases over the years according to its accrued redemption value to factor in expected holding cost. One cannot be expected to pay 38c and risk collecting back 2c in event of a redemption call 6 mths later

Hi Terry,

Thanks for the comment. Great catch. For Scenario 3, I am assuming that the MCBs are converted immediately to calculate the ex-rights price even though they are only converted 10 years later, assuming no redemption. I believe that SIA also accounts for the MCB as equity, even though it is a bond, if I am not mistaken?

I think you are correct. At 0.37/right MCB, it translates to a CAGR of only 2.7%, assuming 4.84 is the terminal value.

The MCB rights might be worthless in the current context.