Lion-Phillip S-Reit ETF is one of the only 3 REIT ETFs available here in Singapore. Given its 100% focus on Singapore REIT counters, it is not surprising that Singapore investors have a natural preference over this Reit vs. its two predecessors: Phillip SGX APAC Dividend Leaders REIT ETF and Nikko AM REIT ETF, both of which are more geographically diversified.

Before I dive deeper into the fundamentals of Lion-Phillip S-Reit ETF and its peers, let me just do a brief introduction of what an S-REIT is.

What is an S-REIT?

S-Reit is a collective term used to describe Singapore-listed REITs. According to data from reitas.sg, there are a total of 43 S-Reits and property trusts listed here in Singapore, with a total market capitalization of S$110bn.

S-Reits have become a very popular investment instrument over the past decade due to their strong capital appreciation track-record as well as their high yielding nature, which many investors views as an attractive passive income source.

In the past, investing in Reits can only be done on a DIY basis by purchasing individual Reit counters. However, since 2016, investors have an alternative option to invest in Reits. That is through a REIT ETF.

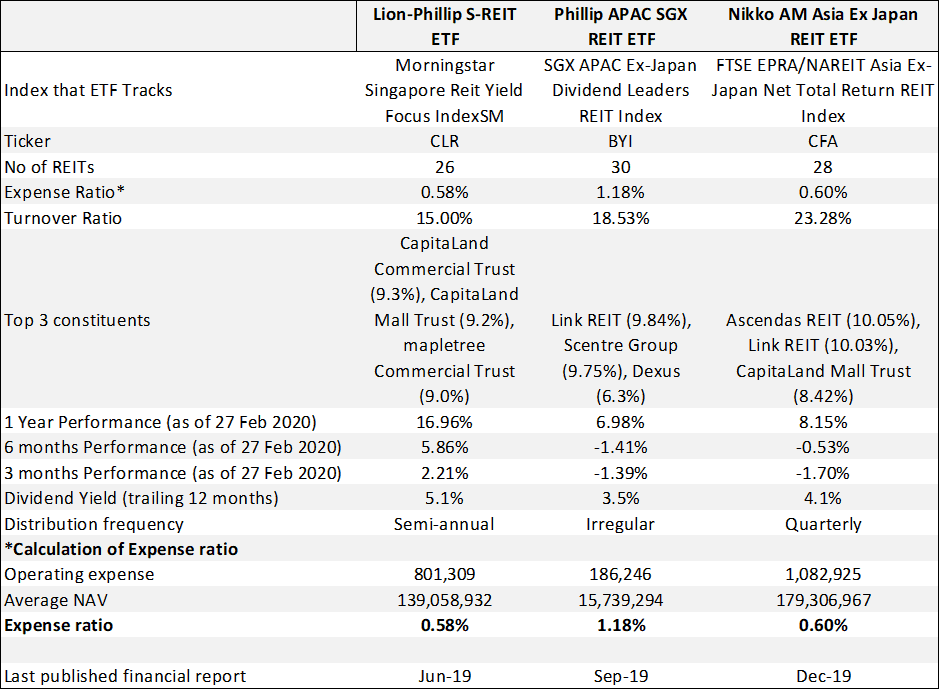

Lion Phillip S-Reit comparison

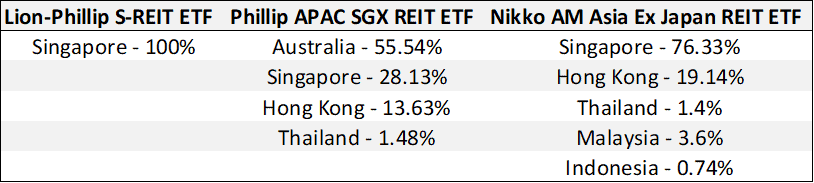

The table below summarises the geographical diversification of the 3 REIT ETF counters.

Concurrently, we also provide a brief comparison between the 3 REIT ETFs.

[supsystic-tables id=2]

Some pretty interesting insights that one can derive from the table above.

For one, I do like to comment that it has been quite a chore to get the information of Lion-Phillip S-REIT ETF as their reports are NOT published on their website and I have to access their latest financial report, which is the June-2019 Semi-annual report on the SGX website.

That aside, Lion-Phillip S-REIT ETF does have the lowest expense ratio at 0.58% with and Nikko AM REIT ETF at 0.60%. What is really surprising is that Phillip SGX APAC Dividend Leaders REIT ETF has an atrocious annualized expense ratio of 1.18%!

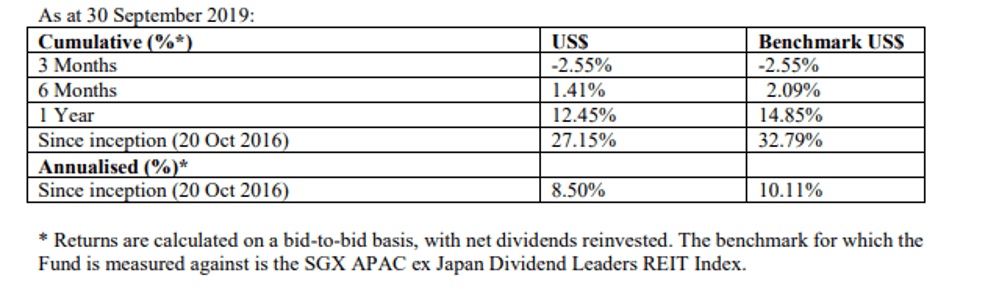

This is likely attributable to economies of scale, or the lack of it. The average NAV of Phillip SGX APAC Dividend Leaders REIT ETF, based on their last financial reporting date at Sep 19 stands at only S$15.7m. The huge variance between Phillip SGX APAC Dividend Leaders REIT ETF NAV vs. its two peers, Lion-Phillip S-REIT ETF at S$139m and Nikko AM REIT ETF at S$179m came as a real surprise to me.

On a turnover basis (half yearly), Lion-Phillip S-REIT ETF has the lowest turnover ratio among the 3 REITs at 15%. This could explain its slightly lower expense ratio vs. Nikko AM REIT ETF.

Coming to their recent performance history (based on information from FSMOne), it does seem like Lion-Phillip S-REIT ETF has been the strong performer, with outperformance recorded on a 1 year, 6-months and 3-months time-frame vs. its peers. This is likely due to the more resilient nature seen in S-REITs vs. Hong Kong and Australia REITs.

Last but not least, the trailing 12-months yield generated (past 12-months distribution per share / current share price as of 2 March 2020) for Lion Phillip S-REIT ETF (semi-annual distribution) is also the highest at 5.1% vs. 3.5% for Phillip SGX APAC Dividend Leaders REIT ETF (distributions have been irregular with distribution compressed by Australian taxes) and 4.1% for Nikko AM REIT ETF (distributions on a quarterly basis).

Based on the preliminary conclusion, it does seem like Lion-Phillip S-REIT ETF is the better buy compared to the other two REIT ETFs available to Singaporeans.

Let’s go into more detail.

4 things you should be aware of Lion-Phillip S-REIT ETF before you consider a purchase

1.Pure Singapore REIT Exposure but not pure Singapore asset exposure

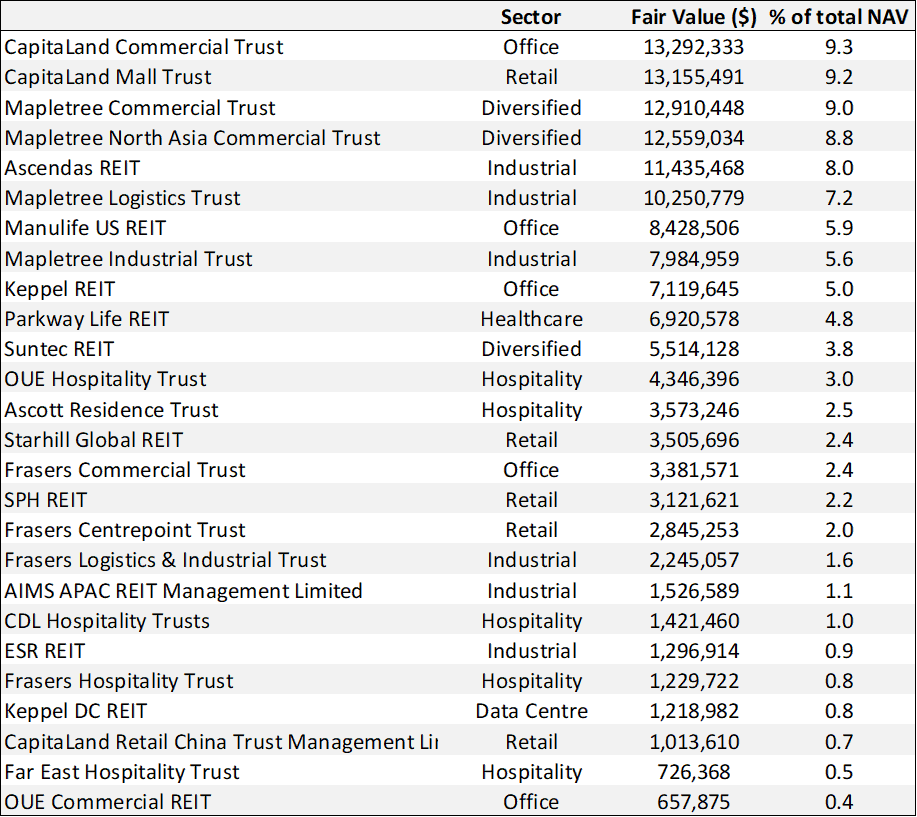

This ETF has 26 SG REIT counters in its portfolio as of Jun 19. According to management disclosure, that figure has increased to 28 SG REIT counters as of Dec 19.

The maximum weight for a single REIT component is 10% and the moment that counter exceeds the 10% threshold, it will be re-balanced. Re-balancing is done on a semi-annual basis.

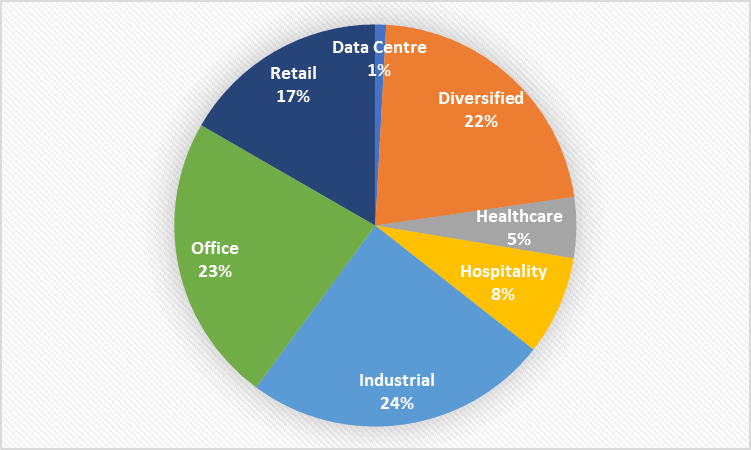

On a sector allocation basis, Lion-Phillip S-REIT ETF has the greatest exposure mainly to 3 sectors: Industrial, Office, and Diversified.

While this ETF invests only in Singapore-listed REITs, it is useful to note that in terms of assets held under these REITs, they are geographically diversified (of course SG will still encompass the bulk of assets). Take, for example, Frasers Logistics & Industrial Trust (which is currently under a process to merge with Frasers Commercial Trust), an SG-listed REIT but have no properties based in Singapore, with the bulk of its assets located predominantly in Australia (remaining in Germany and Netherlands).

Hence, one will not have pure SG-assets exposure by investing in Lion-Phillip S-REIT ETF which is not exactly a bad thing, taking into consideration the rather depressed capitalization rates of properties here in Singapore.

Reits such as Manulife US REIT will also give the ETF access to US-based properties where the rental lease nature or weighted average lease expiry (WALE) of the properties tend to be longer than those in Singapore, giving a certain level of income visibility to the Reit.

2. Lion-Phillip S-REIT ETF is meant to be a Passive ETF

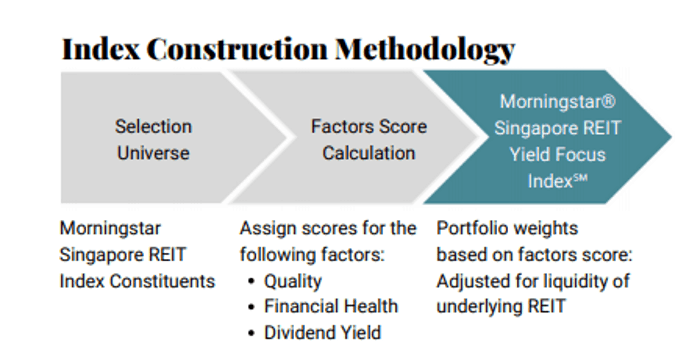

According to the portfolio manager, Lion Global, the ETF is designed to provide investors with low-cost access to 28 (as of end-2019) high-quality S-REITs that offer a sustainable income stream. It is passively managed to fully replicate the Morningstar® Singapore REIT Yield Focus Index℠ (Index).

The index construction methodology is highlighted in the diagram below:

For those who are interested to know more about the index construction methodology, you can refer to the link here. Just be prepared to read plenty of mind-boggling formulas.

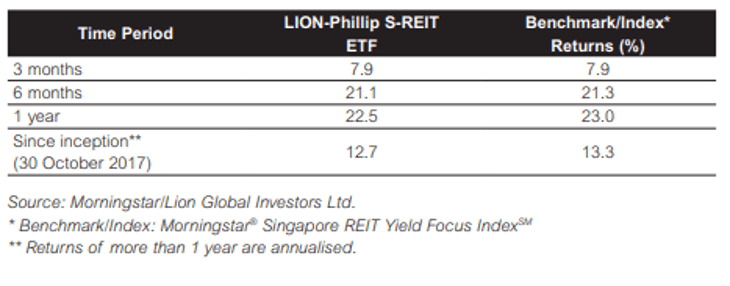

So as a passive ETF, does it really justify the 0.58% expense ratio that investors are paying. To potentially answer that question, we can track the difference between the index performance relative to Lion-Phillip S-REIT ETF performance to see how big a variance that might be.

Based on the information provided by the ETF in their semi-annual report as of June-2019, their performance relative to the index is as such:

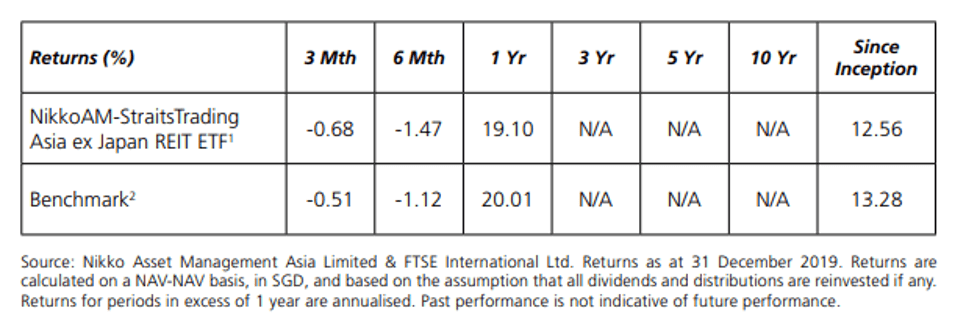

In terms of tracking the index, Lion-Phillip S-REIT ETF has done an OK job. Compared to Nikko AM REIT ETF (performance summary as of 31 Dec 2019), Lion-Phillip S-REIT ETF tracking error is slightly better.

Phillip SGX APC Dividend Leaders REIT ETF has the worst tracking performance.

Overall, I would think that the tracking error of the ETF is acceptable, with its 1 year return only a 0.5% difference vs. the index. The difference could be due to a myriad of factors such as expenses, transaction costs, liquidity, the timing of purchases etc.

So in all consideration, paying the 0.58% expense ratio (while seemingly high compared to other global passive tracker funds) is still acceptable based on the ETF current performance, in my view.

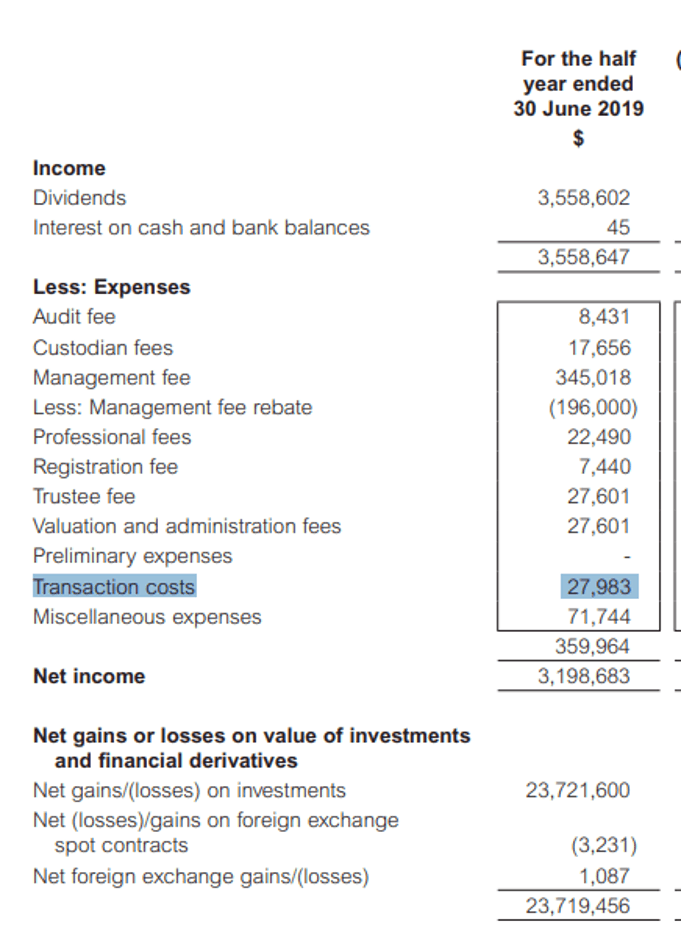

Some would also comment that the expense ratio of 0.58% for Lion-Phillip S-REIT ETF does not fully account for all costs, as total operating expenses do not include brokerage and other transaction costs, performance fees, interest expense, distribution paid out unitholders etc.

Assuming we annualized the fees associated with transaction costs (S$28k * 2) and divide it by the average NAV of the fund, that will add approx. 0.04% to the expense ratio of the fund, bringing the total portfolio costs to approx. 0.62%.

I believe that as the fund starts to stabilize and possibly with growth in NAV, the turnover ratio will decline further, resulting in lower transaction costs (relative to NAV) for the ETF.

All said and done, the current total expense ratio of 0.58-0.62% for Lion-Phillip S-REIT ETF might seem high to some on a standalone basis, given that this is a passive tracker fund with little scope of significant outperforming its index.

Consequently, the actual dividend of the ETF will be lower than the gross dividend the ETF received from all the REITs. What this means is that the actual dividend yield received will be lower than the gross dividend yield published by the ETF.

A more enterprising investor might choose to avoid paying this expense ratio and select REITs on a DIY basis.

3. Singapore Budget 2018 accorded tax transparency status for REIT ETF

The Singapore Budget 2018 extended the tax transparency treatment to REIT ETFs. This means that distributions from S-REITs to ETFs, previously subjected to a 17% tax treatment, will now no longer be subjected to a 17% withholding tax for individuals for both Singaporeans and foreigners.

This essentially means there is no more difference between investing in REIT ETFs and directly in REITs, in terms of dividends received.

This is probably a major win for a REIT ETF as it increases the yield appeal for investing in the ETF vs. purchasing individual REITs on a DIY basis which might not be a feasible solution for those who wish to have a broad-base diversification or just avoid the hassle of managing individual REIT counters (one might be subjected to significant unsystematic risks if their REIT portfolio only consists of a small number of holdings).

4. Do REIT ETFs like Lion-Phillip S-REIT ETF subscribe for rights or get diluted?

As some might be aware, REITs typically pay out the majority of their distributable income and hence when it comes to acquisition, they tend to go to the equity market to raise funding through a rights issue from investors.

So for a REIT ETF manager, do they also subscribe for the rights or get diluted? If it is the former, where is the capital coming from as ETFs do not typically issue rights?

I believe that financialhorse has previously covered this topic pretty well in this article. The gist, if I may summarise from the reply he has gotten from Nikko AM REIT ETF is that the portfolio manager of the ETF will subscribe to the rights by selling other REITs in the portfolio.

The understanding here is that once an index constituent does a rights issue, its weight in the benchmark will increase as its market cap rises with more shares (is it always the case?). Hence the weighting of the other index constituents will fall and the portfolio manager will sell these constituents and use the proceeds to subscribe for the rights issue.

My first thought is that it doesn’t sound right. If doing a rights issuance ALWAYS results in a rise in market cap, then ALL REITs will be doing rights issuance all day long as a way to boost their market capitalization. Wonderful isn’t it?

Typically for a normal company, doing a rights exercise is seen as “a potential problem” as the company needs to raise capital to buff up its balance sheet. However, for Reits, rights issuance is typically associated with acquisitions and if the market believes that the acquisition is yield accretive, they might be in favor of it and consequently pushes the price of the REIT counter up.

However, doing a rights issue and assuming that translates to higher market capitalization right at the onset shouldn’t be the typical understanding.

Financialhorse highlighted the issue that in a global financial crisis such as the one we faced back in 2008, a REIT counter might be forced to do a rights issue as they are not able to obtain refinancing from banks. In this case, the issuance of equity is not used for yield accretive acquisition but instead to pay down “low-cost” borrowings.

If portfolio manager subscribes for the rights of this “financially-distressed” Reit counter, they might be forced to sell other “fundamentally strong” Reits which are trading at depressed prices due to weak market sentiments so as to “balance the ETF according to the Index composition”.

There is no IDEAL solution to how the rebalancing should be done in the scenario and the “problem” pertaining to rights subscription by a REIT ETF remains a pertinent issue.

Conclusion

In this article, I covered briefly the key information pertaining to the 3 REIT ETFs available for Singaporean investors.

The preliminary conclusion was that Lion-Phillip S-REIT ETF is the superior of the 3, based on expense ratio, portfolio turnover, their 1 year performances as well as overall portfolio yield.

I proceeded to take a more in-depth look at Lion-Phillip S-REIT ETF, covering 4 key points which investors should be aware of before making a purchase decision, 2 of which are unique to Lion-Phillip S-REIT ETF while the other 2 factors are more generic in nature, affecting all 3 REIT ETFs in general.

Should one be invested in this REIT ETF? I believe that Lion-Phillip S-REIT ETF is still attractive for those who wish to invest in a portfolio of predominantly blue-chip REIT counters, achieving diversification in the process. For those who are not able (possibly due to compliance issue) or not willing to invest in individual REIT counters, investing in a REIT ETF might be the solution, although that entails paying a recurring fee of c.0.60%/annum.

An alternative solution might be to invest in REIT counters through SYFE REIT+ portfolio, an area which I have written previously in this article: Guide to Syfe and how to open an account in less than 10 minutes. One will still have to pay a recurring platform (Robo-advisor) charges of 0.4-0.65%/annum but save on brokerage charges and SGX fees etc associated with purchasing a REIT ETF through SGX platform.

For those who wish to invest limited capital using a dollar-cost averaging approach on a monthly basis, investing through SYFE REIT+ portfolio is likely the cheapest solution as the Robo fees are all you pay without having to incur expensive commission fees (particular on small investment amount). FSMOne, while providing a cheap regular savings plan approach, does not have Lion-Phillip S-REIT ETF as part of its product offering, hence investors can only choose to invest in Nikko AM REIT ETF.

Do Like Me on Facebook if you enjoy reading the various investment and personal finance articles at New Academy of Finance. I do post interesting articles on FB from time to time which might not be covered here in this website.

Join our Telegram broadcast: https://t.me/gemcomm

SEE OUR OTHER WRITE-UPS

- GUIDE TO SYFE AND HOW TO OPEN AN ACCOUNT IN LESS THAN 10 MINUTES

- ARE YOU OVERPAYING YOUR REIT MANAGER? WHICH S-REITS HAVE THE “HIGHEST” MANAGEMENT FEES?

- WHICH S-REITS HAVE THE BEST RECORD OF DIVIDEND GROWTH?

- 10 GREAT REASONS FOR REITS INCLUSION IN YOUR PORTFOLIO AND 3 REASONS TO BE CAUTIOUS

- WHY I AM STILL BUYING REITS EVEN WHEN THEY LOOK EXPENSIVE

Disclosure: The accuracy of the material found in this article cannot be guaranteed. Past performance is not an assurance of future results. This article is not to be construed as a recommendation to Buy or Sell any shares or derivative products and is solely for reference only.

1 thought on “Lion-Phillip S-Reit ETF: Should you be buying this REIT ETF?”