Quick summary

In a move that caught the market by surprise, Temasek announced that it will make a partial offer to acquire an additional 30.55% of Shares in Keppel.

If successful, the partial offer will result in Temasek owning an aggregate 51% of Keppel.

Given that the Offer Price of S$7.35 is a hefty 26% premium over the last traded price, we believe it is likely that the offer will go through if the pre-conditions are being met. Keppel will remain as a listed entity, albeit at a lower free-float.

Keppel will likely see its price traded up close to the offer price when the stock resumes trading on 22 Oct. Is there more upside from the offer price? What other listed-entities could be in play?

For more detailed information of the offer, do refer to the SGX listing announcement.

Is this a good price for Temasek?

Keppel’s price has been relatively lacklustre in 2019 as we have previously highlighted in our earnings preview article.

In April when Keppel announced its 1Q19 results, the company highlighted that its own internal RNAV of its property division, including Tianjin Eco-City works out to S$6.54/share.

At the offer price of S$7.35, it seems to imply that the rest of the business (O&M + Infrastructure + Investment/ex-Tianjin) is only valued at S$0.81/share or just c.S$1.5bn.

Its Infrastructure division alone has generated S$145m in profits on a 9M19 basis. Adding up contribution from its Investment division which generated S$25m (excluding M1 charges and Tianjin profits) in 9M19 and both these entities generate close to S$230m on an annualised basis.

That implies a PER of only 6.5x for these two business entities and you are getting its O&M division for FREE!

Well that is based on the assumption that the RNAV of its property division is its fair value. In most circumstances, the market will ascribe a certain level of discount between 10-20%.

At a 20% discount to its property’s RNAV, the fair value of the rest of the business is approx. S$3.86bn (based on offer price). Assuming that we value its infrastructure business at 10x (c.S$200m annual profits) and investment business at 15x (c.S$33m in annual profits, excluding Tianjin), that will imply (S$2bn + S$0.5bn = S$2.5bn) in total Infrastructure and Investment divisions valuation, leaving its O&M business valued at only S$1.36bn (sounds cheap?). Read on.

Rationale for the offer

There is no intention for Temasek to delist Keppel but instead to pursue a thorough strategic review of the company which may result in:

- The Company refocusing on and strengthening certain business and/or

- Potential corporate actions including, but not limited to, joint ventures, strategic partnerships, acquisitions, disposals, mergers or other transactions involving the company

as per management’s own words

This is a significant event, in our view, which could be a prelude to future mergers and divestments undertaken by both Keppel and/or Temasek to further stream-line the corporate profiles of key Temasek entities in Singapore.

Market is smelling a potential deal with Sembcorp Group.

Following the announcement of the partial offer which will see Temasek becoming the majority shareholder (if the deal is concluded) of Keppel, the market is now “speculating” a potential deal with Sembcorp Group. Sembcorp Industries -SCI’s (49%-owned by Temasek) share price was driven up by 10% while its 61%-owned marine business under Sembcorp Marine (SembMarine) was up almost 12% on the day of this partial offer announcement.

The logic here is that Temasek, now the controlling of shareholder of Keppel, can embark on a series of deals, such as streamlining its O&M division. This can be done through a potential divestment and subsequent merger with Sembcorp Marine to form a single-dominant O&M entity that can rival its larger peers in Korea.

Such a combination has been well-speculated by the market over the years but today’s event further strengthened the notion of a likely combination, which is only possible if Temasek is spearheading the charge.

What could happen next?

If we are to render a guess, the next step could be for Temasek to start consolidating both Keppel and SCI’s O&M business.

That will entail ascribing a certain valuation to both Keppel’s O&M business as well as SembMarine.

Based on what the market is currently valuing SembMarine (market cap of S$2.8bn as of last closing) vs. what the implied value of Keppel’s O&M business might be (we previously calculated at S$1.36bn) and there seems to be a significant discrepancy.

Is Keppel’s O&M division undervalued or is the market’s current valuation of SembMarine seemingly an overly rosy one? That is something for the market to make a judgement. If it is the former, then there could be even more upside to Keppel’s share price from the current offer.

Ultimately, we believe it makes economical sense for SCI to deconsolidate its marine business to be a pure energy company that will result in significant valuation re-rating, in our view.

Our logic is that the marine business has continuously bogged down SCI Group’s bottom-line, with no light at the end of the tunnel. A clean divestment will monetize the value of its marine business (over-valued perhaps?) and recycle funds back into its core energy business, particularly on renewable.

Telcos consolidation on the radar?

If the partial offer for Keppel is successful, Temasek will become an indirect significant shareholder of M1, in addition to its current 51.2% stake in SingTel.

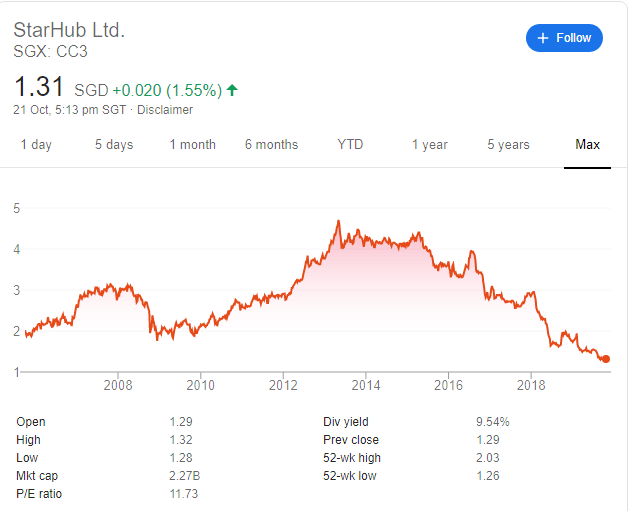

Might a consolidation with Starhub also be a long-term strategy of Temasek in-lieu of significant 5G capex?

Share price of Starhub has been beaten down to an all-time low level? Might it be the time to look at bottom fishing?

Once again, please do your own due-diligence when it comes to dealing in the shares of the entities highlighted above. New Academy of Finance does not own any shares of the above entities as of this writing.

SEE OUR OTHER STOCKS WRITE-UP.

- VENTURE CORP DECLINED BY 4% DESPITE SOLID PHILIP MORRIS 3Q19 RESULTS. HERE’S WHY.

- KEPPEL IS SET TO RELEASE ITS RESULTS TOMORROW. WHAT SHOULD YOU BE EXPECTING?

- 46 STOCKS IN BUFFETT PORTFOLIO

- STRACO: IS IT A GOOD BUY NOW?

Disclosure: The accuracy of material found in this article cannot be guaranteed. Past performance is not an assurance of future results. This article is not to be construed as a recommendation to Buy or Sell any shares or derivative products and is solely for reference only.