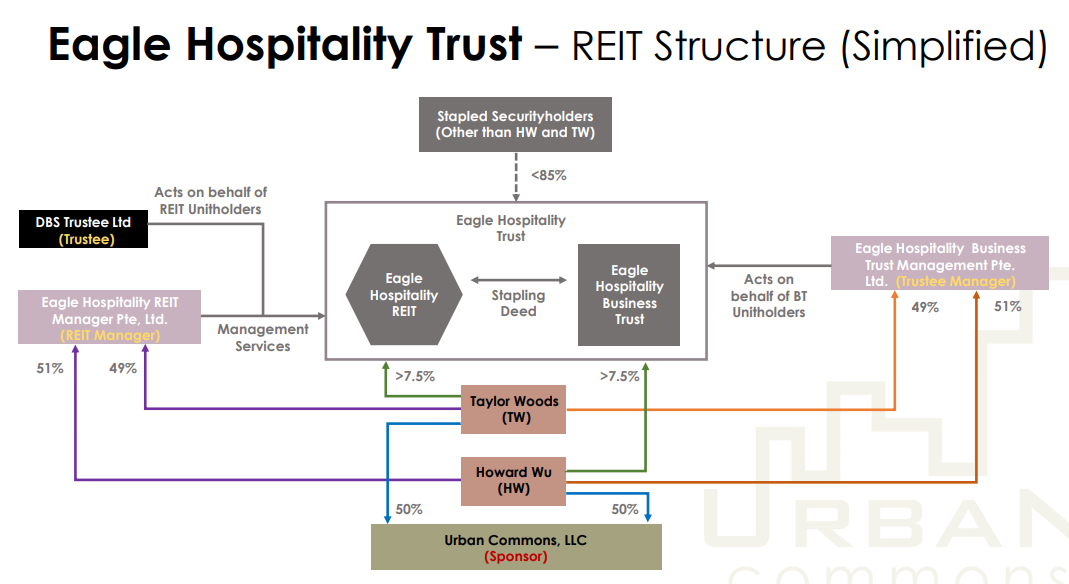

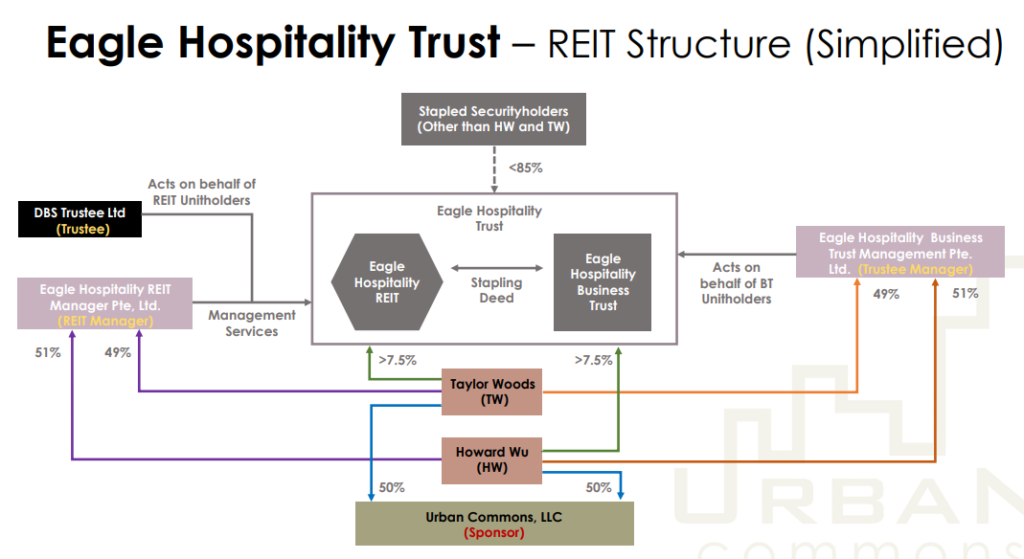

Eagle Hospitality Trust (EHT) is a business trust that was listed back in May 2019. Many investors will likely be familiar with the trust, one which promises high recurring yield with its master lessee structure. Alas it did not turn out according to investors’ expectations and the trust was bogged by issues in its very first year of listing and subsequently suspended from trading in March 2020.

In this article, I will provide a quick overview of the problems faced by Eagle Hospitality Trust in the first part of the article, followed by a write up on Urban Common, Eagle Hospitality Trust’s sponsor side of the story. Readers can also download a pdf version of a summary PowerPoint on what exactly happened, from the viewpoint of Urban Common, found in the latter part of the article.

Eagle Hospitality Trust problems

Problem #1: The Queen Mary

One of Eagle Hospitality Trust’s key assets, The Queen Mary, received a lot of attention back in late-2019, all for the wrong reason. It was reported in The Edge Singapore that the condition of the ship was bad based on inspection reports. According to a survey report, the total cost of ship repairs could range from USD$235m to USD$289m. In addition, it estimated that the work would take approx 5 years to complete, with some 75% of repairs deemed “urgent”.

According to Eagle Hospitality Trust’s IPO prospectus, The Queen Mary has been valued at USD$159.4m and had an occupancy rate of 69.8% as at FY18. The operating condition of this asset was a huge uncertainty that could adversely impact Eagle Hospitality Trust’s performance in its very first year of listing.

The Queen Mary remains closed to the public due to the coronavirus pandemic, with no indication of when it will reopen based on the latest information.

Problem #2: Major shareholders exiting in drove

Major shareholders have been reducing their stakes which weren’t a show of confidence in both the outlook of the trust as well as its management. While there can be many reasons why shareholders are reducing their stakes, a substantial reduction is always a cause for concern.

For example, major shareholders such as Norbert Shih and Frank Shih reduced their double-digit stakes to less than 5% and they might no longer hold stakes in Eagle Hospitality Trust anymore. Substantial shareholder Qian Jianrong also reduced its stake. Gordon Tang, the founder of Sing Haiyi, was the only party that increases his stake in the Trust.

Problem #3: COVID-19 hit the hospitality industry badly

The COVID-19 pandemic hit the global hospitality industry badly. SG Hospitality REITs were not spared either with many tumbling by approx 50% from recent peak to trough.

Eagle Hospitality Trust was the worst performer within the hospitality trust category, with its share price collapsing almost 70+% since the global market peak on 19 Feb to its trough sometime in mid-March. There is no clear explanation of why Eagle Hospitality Trust performed so badly beside the fact that one of its key property is The Queen Mary which is “viewed” as a cruise vessel. We all know what happened to the cruise industry. There was widespread fear that being confined in congregated spaces onboard a cruise vessel out in the open sea is “asking for trouble”. The Queen Mary, though permanently moored since 1967, apparently was classified in the same category.

This was also despite the fact that Eagle Hospitality Trust has 17 other hotels which are not vessels.

Problem #4: Urban Common default on its rental obligations

On 24 March 2020, Eagle Hospitality Trust voluntarily suspended trading of its unit when its master lessee, Urban Commons could not fulfil its rent obligations. When the REIT manager of Eagle Hospitality Trust tried to draw down US$12.5m of the US$28.7m security deposit to increase liquidity and remedy delinquencies, it triggered Bank of America to issue a notice of default and an acceleration of the USD$341m that the trust had borrowed to fund the property acquisitions to be immediately payable.

Eagle Hospitality Trust was barred from distributing dividends because of the default. Investors were left in a bind as they can no longer sell their shares due to the suspension. Neither can they receive any dividends.

It might seem that the problem started with Urban Common defaulting on its rental obligations. However, it is probably not uncommon for a property lessee to be missing rental payments during this critical COVID-19 period.

Why wasn’t there any communication between lessee and lessor?

What exactly went wrong which resulted in this disappointing outcome with the REIT being suspended since March with shareholders clamoring for answers that no one seems to be able to provide.

Urban Commons: Their side of the story

Urban Common, on 12 August, issued notices of breaches to Eagle Hospitality Trust, claiming that funds it had injected into Eagle hospitality Trust are outstanding and due for repayment.

In a media release, Urban Commons claimed it had provided Eagle Hospitality Trust with “millions of dollars in excess of the audited hotel income” to subsidize rent and other reserves paid by the hotels under the master lease agreements.

So the saga seems to continue, with Urban Commons now claiming that Eagle Hospitality Trust owes them money, instead of what we thought was the other way round.

One of the key items in the media release was that Urban Commons claimed to have a plan to provide financial support to Eagle hospitality Trust but has been unable to implement this plan because of a lack of cooperation from Eagle Hospitality Trust’s trustee (DBS), the special committee negotiating with lenders and Eagle Hospitality Trust’s third-party advisors and consultants.

Urban Commons also claimed that the hiring of these advisors and consultants is costing Eagle Hospitality Trust millions of dollars of unitholders’ cash.

So beyond the fact of whether Urban Commons owe Eagle Hospitality Trust money or the other way round, why was Urban Commons proposal to “help” rescue the trust being ignored by DBS Trustee and the special committee?

From a layman’s perspective, it is easy to understand why. Would you let someone who “stab” you in the back subsequently becoming your savior? I am not saying that this IS the reason why Urban Commons’ proposal was not being entertained. I don’t have access to the thoughts behind the trustee’s action. However, if there is no clear party who can save the trust till date, is it only reasonable that every possible solution to help save the trust be considered?

This will be in the best interest of shareholders. How comprehensive Urban Commons plan is or NOT, is up to all relevant parties and stakeholders to contemplate and come to a conclusion.

I have attached the pdf version of the powerpoint presentation here.

Key summary of Urban Common defense

Payment affected by outbreak of COVID

Master Lessees has made full payment till Dec 2019, paying for repairs on damages to the properties due to hurricane damage first, even when it’s the responsibility of the REIT.

For the January rent which was due in February 2020, while the payment of rent was affected by the impact of COVID-19, this was offset by the amount the Master Lessee had over-funded EHT by paying its full rent in accordance with the MLA – even though the Orlando properties of EHT were impacted by hurricanes in late 2019.

Funded the necessary capital (in advance for EHT) caused by a category 5 hurricane, which caused damage to EHT’s largest hotel in Orlando. The master lessee has also continued to pay for fixed rent of approximately US$3 million for Holiday Inn in Orlando, Florida, despite damages to the property.

For the February rent which was due in March 2020, the fixed rent payments are covered by the Force Majeure situation, directly attributed to COVID-19. March 2020 income came in at negative US$4 million compared to fixed rent due to almost non-existent occupancy levels, and therefore income, as a result of the global pandemic.

Contributed approximately US$10 million more to the REIT than hotel-level generated income to support EHT.

Forensic Accounting Investigation damage the reputation of Urban Commons

Given Urban Commons’ voluntary efforts to support the hotels financially and the master lessees full compliance with their reporting obligations under the MLA, Urban Commons believes that the advisory firm appointed by EHT’s demand for additional information and the threatened forensic accounting investigation are bad faith efforts to damage the reputation of Urban Commons by attempting to create some appearance of wrong-doing.

Attempt to talk to trustee and advisors being ignored

Since April 2020, Urban Commons has attempted to engage with the Trustee and its advisors on restructuring/recapitalizing EHT on multiple occasions. However, the Trustee does not respond and there is no call or meeting with the Trustee until 22 July 2020 regarding the RFP progress.

What exactly went wrong?

The notice of default was the crux leading to the current crisis of EHT. This is due to several factors.

• COVID-19 having a huge fiscal impact on the global tourism industry, resulting in a precipitous fall in occupancy rates and operational performance of EHT properties.

• This triggered the REIT Manager to try to draw down US$12.5 million of the security deposits to increase the liquidity of EHT and remedy delinquencies in rent payments from the master lessees

• This, in turn, brought the rental delinquencies to the attention of its lenders, which led to the lenders issuing a notice of default and acceleration on a US$341 million loan, and the subsequent voluntary suspension of the REIT.

For further information on the timeline of the events that happen, please refer to the PDF attached.

Conclusion

This article aims to highlight the issues with Eagle Hospitality Trust which some might say is already water under the bridge. More importantly, what is the solution that is in the best interest of EHT’s unitholders.

Can the REIT be salvaged at the end of the day through the collaborative efforts of all parties?

Urban Common might be portrayed as the “villain” in this whole saga due to its rental default which essentially triggered a notice of default from EHT’s creditors. Are they however, the only party to be blamed?

I don’t have the full picture at this juncture to make a conclusion.

This article is mainly to provide a background of EHT’s problems as well as its sponsor side of the story.

I hope to update readers on more information pertaining to EHT or Urban Commons when they are made available.

Do Like Me on Facebook if you enjoy reading the various investment and personal finance articles at New Academy of Finance. I do post interesting articles on FB from time to time which might not be covered here in this website.

Join our Telegram broadcast: https://t.me/gemcomm

SEE OUR OTHER WRITE-UPS

- IS TIME RUNNING OUT FOR KEPPEL AND SEMBCORP MARINE AS OIL COLLAPSES BELOW ZERO?

- SEMBCORP INDUSTRIES 4Q19 BETTER THAN EXPECTED. SHENG SIONG MARGINALLY DISAPPOINTS

- SEMBCORP MARINE 4Q19 LOSSES EXCEEDED EXPECTATIONS. WHAT YOU SHOULD KNOW

- SEMBCORP INDUSTRIES: PROFIT WARNING A PRELUDE TO MORE PAIN IN 2020?

- SEMBCORP MARINE 3Q19 LOSSES BALLOONED TO S$53M. WHAT YOU SHOULD KNOW

- TOP 5 UNDERVALUED SINGAPORE DIVIDEND STOCKS (2020)