This is an article that Syfe wrote and I thought it will be interesting to share with readers of NAOF. I have previously written what i believe is a non-biased review of the investment methodology behind Syfe’s ARI algorithm. I then followed up with a step-by-step account opening process which took me less than 10 minutes. In this article, I will also showcase how my REIT+ portfolio has performed since inception on 27 Feb as well as detail Syfe’s possible outperformance against similar peers.

Without further ado, the first portion of this article is written by Syfe which I believe presents an easy to comprehend logic behind its ARI algorithm.

Market Whiplash: How Syfe’s ARI Algorithm Reacted

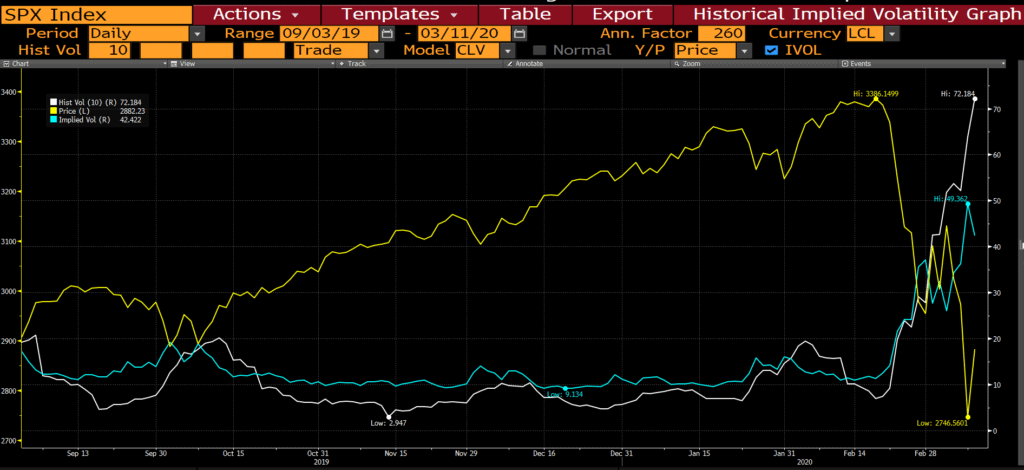

After a spectacular year for the stock markets in 2019, the first two months of 2020 started off promisingly. In fact, the S&P 500 index hit an all-time high on February 19. But developments over the past weeks – mounting coronavirus cases across the world and the split between key oil producers Russia and Saudi Arabia – have sent stocks on a dizzying roller-coaster ride.

So how did Syfe’s automated risk-managed investing (ARI) algorithm deal with the wild market swings? The chart below offers some insight. It illustrates that the recent increase in market volatility (blue line) occurred abruptly, shooting up quickly from previously low levels in a matter of days. The sustained increase in volatility during the initial days of the market drop from 19 to 25 February further indicated that market risks will remain high in the near future. As such, our ARI algorithm adjusted asset allocations to reduce risk across all portfolios.

By decreasing the share of equities and increasing the share of lower-risk bonds and commodities, Syfe’s rebalancing returned the risk levels of each portfolio back to their target downside risk levels. After the S&P 500 posted its worst one-day percentage drop since the 2008 financial crisis on Monday (9 March), this risk-based rebalancing we conducted helped cushion the impact of that drop on portfolio values.

How Our Rebalancing Helped Investors Weather Market Turbulence

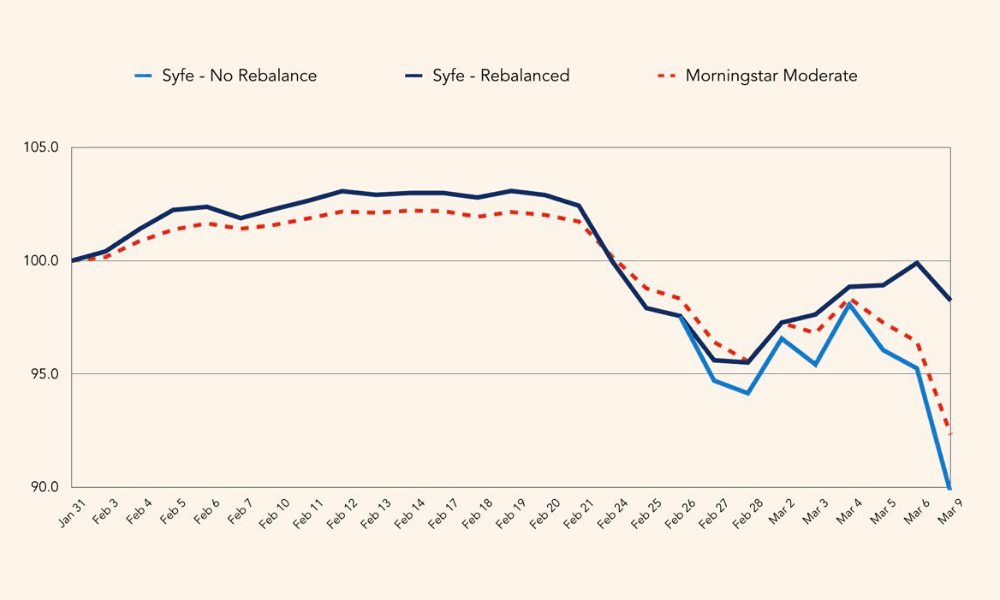

To illustrate, the graph below shows the actual performance of our 15% Downside Risk (DR) portfolio (dark blue line). As the market correction started worsening towards the end of February, the risk level of this 15% DR portfolio had risen to nearly 18%. Consequently, Syfe made a series of rebalancings on 25, 26 February and 2 March to bring the portfolio risk level back to its targeted 15% downside risk level.

When markets dropped again from 26 to 28 February, the rebalanced portfolio experienced a smaller decline in value of about 2.1%. If Syfe had not made any risk-reducing allocation changes, the un-rebalanced portfolio would have suffered a drop of 3.5% instead.

The markets then entered a period of roller-coaster swings from 28 February to 4 March. The rebalanced portfolio not only performed better than the un-rebalanced portfolio but also experienced less of the jarring ups and downs that occurred.

As markets plunged on 9 March, the rebalanced portfolio was significantly more resilient. It experienced a milder 1.7% drop in value compared to the un-rebalanced portfolio, which fell steeply by 5.8%.

The Syfe Difference

The value of Syfe’s risk-based rebalancing approach can also be seen by how the rebalanced portfolio has outperformed both it’s benchmark and the un-rebalanced portfolio over the past weeks. While it still experienced dips in value amid the broader stock market correction, the rebalanced portfolio experienced less volatility as well during this period. This gives investors the assurance that their portfolio risk will not exceed their chosen Downside Risk level i.e. they are unlikely to lose more than what they are comfortable with losing, given their risk appetite.

The S&P 500 has fallen 14.7% from 31 January to date (9 March 2020). In this same time period, Syfe’s 15% DR portfolio only dipped 1.8% due to our portfolio risk management. It is important to note that our ARI algorithm is not designed to react to every single price fluctuation that occurs in the market. Instead, it waits to make significant allocation changes until the increase in volatility can be assessed to be a sustained increase in market risk.

This is why ARI did not rebalance portfolios the moment prices fell – to do so would simply be making trading decisions based on price, instead of risk management. More details on how ARI is able to measure and forecast market risk can be found in our whitepaper here.

Because ARI is designed to keep portfolio risk in line with our investors’ chosen downside risk level, this also means that it will rebalance portfolios again when it detects that market volatility is abating. As the market makes its eventual recovery, ARI will increase the shares of equities across portfolios so investors can capture the market upside.

Syfe’s risk-based rebalancing strategy may not always correspond to the gut feel of investors, but it delivers better risk-adjusted returns over the long term. When investors are assured that their portfolio risk is always in sync with their risk tolerance, they are less likely to panic sell their investments in a downturn, thus paving the way for long-term investment success.

This article first appeared on Syfe.

NAOF SYFE REIT+ performance

So I incepted a position in SYFE REIT+ on the 27th February and Syfe started purchasing units on the 28th February which seems like I have effectively caught the recent bottom in REITs, based on the iEdge S-REIT 20 Index, an adjusted free-float market capitalization-weighted index that measures the performance of the largest and most tradable companies in the SGX S-REIT Index.

From 28 February to 11 March, the index returned a total of 2.4%.

During this same period, my Syfe REIT+ Portfolio generated a return of 2.65%.

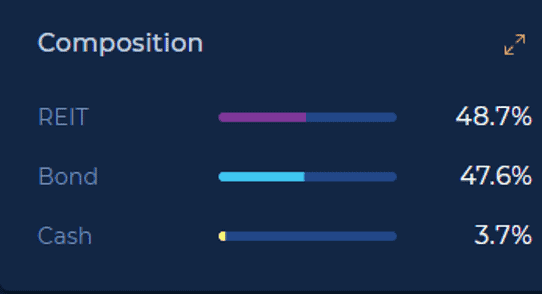

In terms of portfolio composition, the 15% risk profile (standard across all REIT+ portfolio) now composed of 48.7% REIT, 47.6% Bond and 3.7% cash.

During the time period 28 February to 11 March, the bond performance, represented by ABF Singapore Bond Index Fund, generated a total return of 2.2%.

So on a weighted average basis, the portfolio should have generated total returns equating to:

iEdge S-Reit 20 index (2.4%) * 48.7% + ABF Singapore Bond Fund Index (2.2%) * 47.6% = 2.22%

So for it to generate 2.65% during this short period of time, there is some minor outperformance.

Once again, I have got to caution that the time period is just too short for us to make any reasonable conclusion pertaining to the “superiority” of Syfe’s ARI algorithm.

As i have highlighted in my previous article on Syfe, the success of the platform at the end of the day depends on its reaction time pertaining to portfolio adjustment after recognizing a significant change in the volatility profile of the individual asset-class. If Syfe’s ARI algorithm is slow to react to asset volatility changes, it might not be in time to significantly decrease its Reit-weighting (which will be at the peak prior to the market sell-down).

So far, it does seems like the Robo-advisor is doing its job. In the article, Syfe highlighted that the S&P500 index has fallen 14.7% from 31 January to date (9 March 2020). In this same time period, Syfe’s 15% DR portfolio only dipped 1.8% due to their portfolio risk management.

I believe a better comparison will be using a 60:40 equity/bond portfolio composition which is what Syfe’s 15% DR portfolio is generally benchmarked against.

We use the ticker IVV to represent the S&P500 index and the ticker ITE to represent intermediate US bonds. From 31 January to 9 March, IVV declined by 15% while ITE increased by 3.5%. On a 60:40 portfolio, the average weighted return would have been -7.6% vs. Syfe’s -1.8%.

I think this would have been a fairer comparison although the conclusion would remain the same, that Syfe’s risk-focused portfolio has likely outperformed its comparable peers and benchmark.

PROMOTION BY SYFE:

I hope I have presented the relevant information in an unbiased format with my own personal opinion for you to make an informed decision. You might agree or disagree and the decision to invest with Syfe is totally up to you.

Syfe has kindly reached out to NAOF readers and you can choose to sign up through this affiliate link where I may receive a share of the revenue from your sign-ups.

As a special offer for New Academy of Finance readers, you can receive bonuses for creating and funding your Syfe account:

$10 bonus for funding your Syfe account above $500

$50 bonus for investing more than $10,000 with Syfe

$100 bonus for investing more than $20,000 with Syfe

This bonus will be credited within 7 days after receiving your funds and invested together with your portfolio.

To enjoy this promotion, you will need to maintain the portfolio with Syfe for at least 6 months. You can read more details on the promotion here.

Do Like Me on Facebook if you enjoy reading the various investment and personal finance articles at New Academy of Finance. I do post interesting articles on FB from time to time which might not be covered here in this website.

Join our Telegram broadcast: https://t.me/gemcomm

SEE OUR OTHER WRITE-UPS

- GUIDE TO SYFE AND HOW TO OPEN AN ACCOUNT IN LESS THAN 10 MINUTES

- TOP 5 RESILIENT SINGAPORE STOCKS TO BUY AMID COVID-19 UNCERTAINTY

- A BETTER ALTERNATIVE TO DOLLAR COST AVERAGING?

- BEST ETFS IN SINGAPORE TO STRUCTURE YOUR PASSIVE PORTFOLIO

- IS DRINKING LATTE REALLY COSTING YOU $1 MILLION AND THE CHANCE TO RETIRE WELL?

Disclosure: The accuracy of the material found in this article cannot be guaranteed. Past performance is not an assurance of future results. This article is not to be construed as a recommendation to Buy or Sell any shares or derivative products and is solely for reference only.