I wrote about Sembcorp Industries and Sembcorp Marine demerging yesterday in the article below:

Sembcorp Industries and Marine demerger: What you need to know and what to do

In that article, I concluded that the news should be a positive one to Sembcorp Industries as the company can finally become a pure Utilities/Energy play which will aid in a valuation re-rating. There will no longer be the burden of funding its marine arm which has also been loss-making for the past few years.

The price of Sembcorp Industries appreciated by more than 40% at one point in time before closing at S$2.09 today, up 37% from the price before the counter was halted.

Sembcorp Marine’s share price crumbled to as low as S$0.45 before recovering to close at S$0.62, down 27% prior to its halt.

The street consensus seems to favor a continual appreciation of Sembcorp Industries’ share price and reckon that Sembcorp Marine’s share price will continue its downtrend momentum.

Many believe that Sembcorp Industries’ shareholders are getting Marine shares for “FREE”. Is that really the case?

In this follow up article, I also look to decipher what might be a fair value for Sembcorp Industries.

Before that, let’s again examine what has change in terms of the shareholding structure as I believe it is worth a second look.

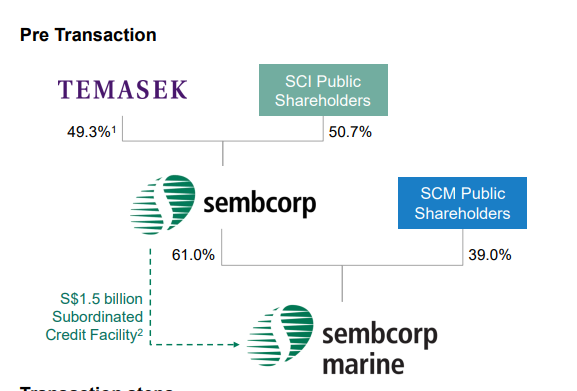

Pre-Transaction structure

Before the transaction, Sembcorp Marine is 61% owned by Sembcorp industries with the remaining 39% in public hands. Temasek owns 49.3% of Sembcorp Industries with the remaining 50.7% ownership of Sembcorp Industries in the public hands.

What else can we glean from this information? That Sembcorp Industries public shareholders in fact have an indirect stake of 30.9% in Sembcorp Marine, calculated as 50.7% * 61% = 30.9%

At this juncture, Sembcorp Industries has previously borrowed S$1.5bn on behalf of Sembcorp Marine as the latter found it increasingly difficult to access bank funding on its own. Even if they manage to get their own bank funding, that will likely come at a high-interest cost. Hence, its parent, Sembcorp Industries decided to tap its own lending facilities through a bond issuance and provide a subordinated loan to Sembcorp Marine.

So Sembcorp Marine remains liable to paying back Sembcorp Industries the S$1.5bn, stretch over 5-years

Post-Transaction structure

Post-transaction, notice that Sembcorp Industries public shareholders continue to own 50.7% of the company but their stake in Sembcorp Marine (previously at 30.9%) has now changed to 30.9% to 35.4%, depending on how much Sembcorp Marine’s shareholders decide to subscribe for the rights. Assuming full subscription from Sembcorp Marine’s shareholders, their stake will remain at 30.9%.

So what has change? Previously, Sembcorp Industries has a “loan receivable” of S$1.5bn from Sembcorp Marine. That has now effectively been “waived” off to offset the rights payment to Sembcorp Marine.

For a Sembcorp Industries minority who does nothing, this transaction has effectively reduced the company’s liquidity by S$1.5bn.

So how is a reduction of S$1.5bn taken so positively by the street? Over here, we assume that Sembcorp Marine’s valuation does not change and the company is valued as much vs. pre-transaction.

It seems like a valuation re-rating (potentially pure-play utilities) for Sembcorp Industries is already taking place or is the market just “fooled” by the “free” marine shares?

Sembcorp Industries fair value

To fairly value Sembcorp Industries, one will likely need to do a sum-of-the-parts valuation of its different businesses.

Sembcorp Industries’ key business entities are Energy(utilities), Marine, and Urban Development. We ignore the “Other Businesses” segment.

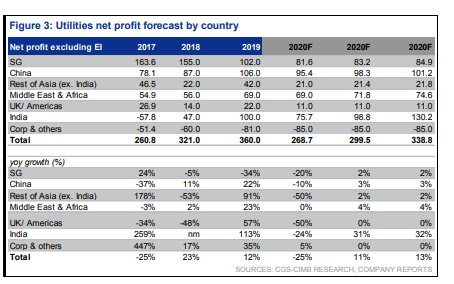

Within its Energy division, one can break it up into 6 geographical sectors, mainly Singapore, Southeast Asia, China, India, the UK, and the Rest of the World.

The table above illustrates the profit breakdown of the various geographical sectors based on its FY19 results.

Singapore, China, and India together account for the lion’s share of profits in its Energy division. However, one would notice that its Singapore operations saw a 34% YoY decline in net profit in FY19.

Ideally, we should derive the individual valuations of its Energy division geographical sector based on its profitability or NAV. However, I currently do not have the means to do just that.

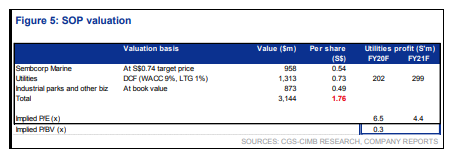

Instead, I refer to CIMB’s SOTP valuation of Sembcorp Industries done on 18 May (note that they have since updated their valuation post this announcement but now using a different methodology)

In their May 18 report, they highlighted that the Energy/Utilities business was worth S$1.3bn or S$0.73/share. This was valued using DCF.

Industrial parks (Urban development) and other businesses were valued at book value, which was worth S$873m or S$0.49/share

Add together, both these entities were worth S$1.22/share. So, if you are a Sembcorp Industries shareholder post the transaction, your Sembcorp Industries stake alone should theoretically be worth only S$1.22/share, according to CIMB in its May 18 report.

Assume you have got 100 shares of Sembcorp Industries. That will entitle you to between 427-491 new Sembcorp Marine shares. Let’s take the average and go with 459 new Sembcorp marine shares.

Base on a scenario where Sembcorp Marine’s share collapsed to S$0.20 post the rights. At S$0.20/share with outstanding shares of 12.54bn, Sembcorp Marine will be worth S$2.5bn or S$1.2bn more than its current market cap of c.S$1.3bn. Granted that the company will now be a much less levered entity.

With 459 new Sembcorp marine shares that are worth S$0.20/share, that equates to a value of S$92 or S$0.92/SCI shares (S$92/100 Sci shares) Add that to your Sembcorp Industries shares worth S$1.22/share and you will have a fair value of S$2.14/share. (not finish)

A key question is if the S$0.73/share ascribe to its Energy division is fair. On the surface, this translates to a value of S$1.3bn and with its energy division generating S$360m in profit before exceptional items in 2019, which equates to trailing normalized PER multiple of just 3.6x. Looks extremely cheap.

CIMB previously forecasted its forward Energy division to generate S$269m in profits for 2020 or a forward multiple of 4.8x. Still decently cheap.

However, given the huge variability in earnings, particularly from India, there is a case to be cautious.

Alternatively, one can strip out the earnings of India and value that entity on a book basis.

In Sembcorp Industries’ book, its India entity alone was valued at S$1.57bn as of end-2019. Compare that to our valuation of the entire energy division at S$1.3bn and it seems like there is a whole lot of re-rating potential for Sembcorp Industries.

However, the only way to realize that potential is to monetize its stake in India through an IPO which has been delayed time and again. If I assume only a 50% value to its India book value, then its India entity will be valued at S$0.785bn.

That will imply that the rest of its Energy division is valued at S$1.3bn – S$0.785bn = S$0.515bn

These geographical entities are forecasted by CIMB to generate combined earnings of S$193m (including corporate expenses). That will imply a forward PER multiple of just 2.7x for these entities.

There is huge value to be unlocked from Sembcorp industries assuming they can get their act together and improve the operating performance of their core Energy Division.

Should we consider the additional debt commitment?

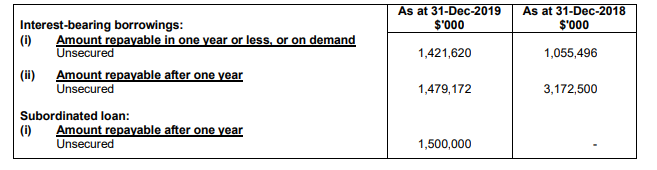

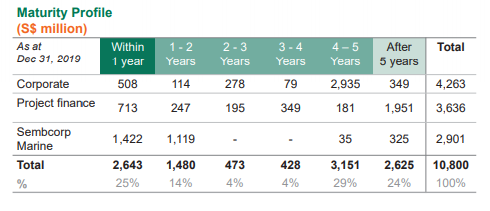

Sembcorp Marine’s end-2019 borrowing status showed that it has a combined $4.5bn in debt repayable.

In Sembcorp Industries’ end-2019 financial presentation, it shows Sembcorp marine’s debt profile of S$2.9bn which excluded the subordinated loan. This subordinated debt is likely to park under the corporate segment with S$2.935bn outstanding.

The question begets if one should take into account this S$1.5bn loan which has now turn into equity in Sembcorp Marine.

If so that translates to S$0.83/ SCI share. Assuming absolutely no re-rating, that will mean a subtraction of S$0.83/share from the fair value of S$2.14/share calculated earlier, deriving a fair value of S$1.31.

However, if the market did decide to re-rate Sembcorp Industries, which we based on the valuation assumption below:

- 50% book value of India entity

- 8x forward PER to its Energy Division

- 1x book for Urban Development

- Value of Sembcorp Marine shares at S$0.92/SCI share

That will translate to a fair of S$1.88/share after deducting the S$0.83/share in additional debt commitment.

Conclusion

This is just my brief stab in trying to derive a fair value for Sembcorp Industries which is likely fraught with huge variability and readers should take with a pinch of salt.

I like the fact that Sembcorp Industries is now a cleaner entity compared to the past and that itself deserves a re-rating. However, even with a substantial re-rating for its Energy Division, I wonder if its share price can continue to appreciate from the current level.

Do Like Me on Facebook if you enjoy reading the various investment and personal finance articles at New Academy of Finance. I do post interesting articles on FB from time to time which might not be covered here in this website.

Join our Telegram broadcast: https://t.me/gemcomm

SEE OUR OTHER WRITE-UPS

- IS TIME RUNNING OUT FOR KEPPEL AND SEMBCORP MARINE AS OIL COLLAPSES BELOW ZERO?

- SEMBCORP INDUSTRIES 4Q19 BETTER THAN EXPECTED. SHENG SIONG MARGINALLY DISAPPOINTS

- SEMBCORP MARINE 4Q19 LOSSES EXCEEDED EXPECTATIONS. WHAT YOU SHOULD KNOW

- SEMBCORP INDUSTRIES: PROFIT WARNING A PRELUDE TO MORE PAIN IN 2020?

- SEMBCORP MARINE 3Q19 LOSSES BALLOONED TO S$53M. WHAT YOU SHOULD KNOW

- TOP 5 UNDERVALUED SINGAPORE DIVIDEND STOCKS (2020)

Disclosure: The accuracy of the material found in this article cannot be guaranteed. Past performance is not an assurance of future results. This article is not to be construed as a recommendation to Buy or Sell any shares or derivative products and is solely for reference only.