Recession-Proof Companies

There are many US companies with an illustrious track record of growing their dividend payment every year. The bests of the bests are the Dividend Kings, companies that have grown their dividend payments by 50 consecutive years. There are currently 28 companies that meet this criterion and one can download the latest list, courtesy of simplysafedividends.

What is even rarer is for a company to demonstrate 14 years of consecutive EPS growth. These companies have been increasing their EPS every single year from 2005 to 2019 which is an incredible feat, noting that it envelopes the Great Financial Crisis (GFC) period of 2007-2009 where numerous companies saw their earnings being devastated.

We found just a handful of large-cap US recession-proof companies that fit this criterion. Just 5 in fact. (Note: this list might not be fully comprehensive, but just the companies that we are aware of)

These are companies that have proven themselves to be recession-proof, as demonstrated by their earnings growth even during a weak economic climate. When economies are doing well, these companies continue to thrive, as seen from the last decade of earnings growth performance.

Out of the 5 stocks, 4 are in the Retail industry while 1 is in the Telecommunication industry.

Without further ado, let’s review the 5 stocks that have demonstrated such a superior record of earnings growth, with a high probability that this track record can be extended into Year 15.

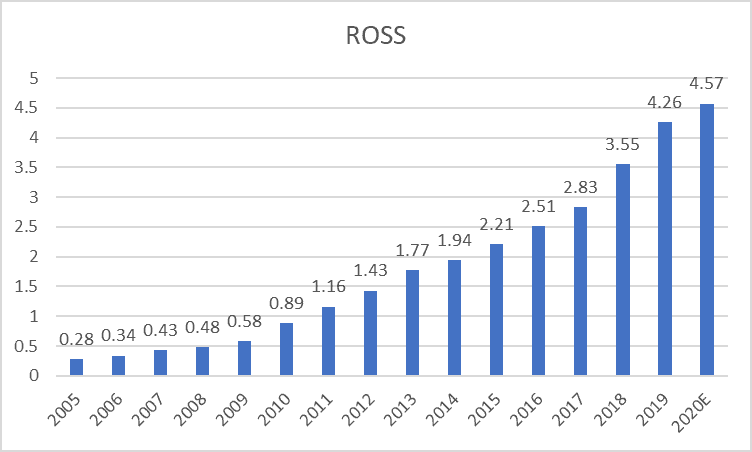

1. Ross Store (ROST)

Ross Store operates under the brand name Ross Dress for Less and is the LARGEST off-price retailer in the US, with the company operating more than 1,500 stores across 39 US states.

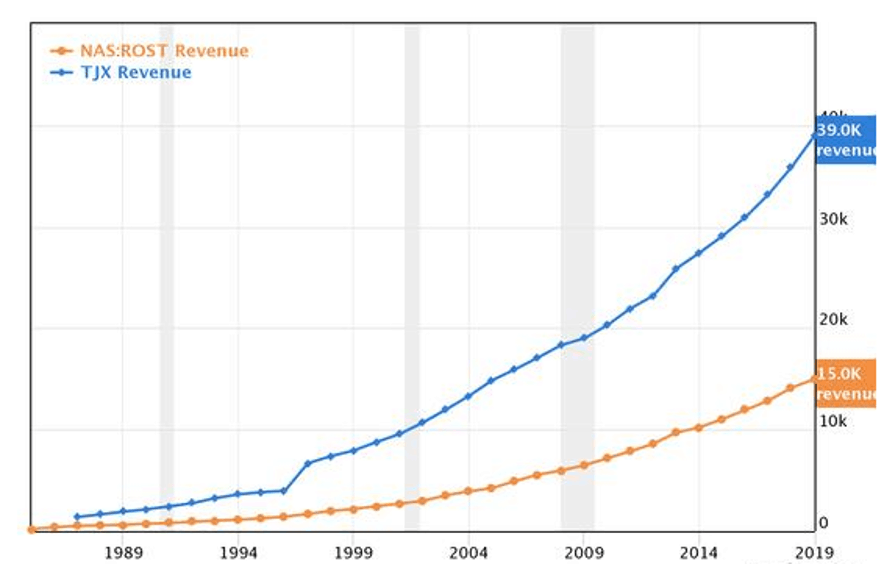

In the US, we see that Ross Stores dominates the off-price space alongside TJX Companies. These two companies both consistently delivered high return on capital over the years.

It is not surprising that a company like Ross Store will thrive in a recessionary climate as US consumers seek out the best bargains. In fact, according to the chart from GuruFocus seen below, both Ross Stores and TJX Companies managed to grow their sales throughout each of the past three recessions.

While investors might be concern about the slowing demise of brick-and-mortar shops due to the proliferation and disruption from e-tailers such as Amazon, a niche off-price retailer like Ross Store could in fact benefit from increasing market share as smaller retailers go out of business.

The company, however, is not trading cheap, with its PER ratio currently at the top-end of its 10-years historical trading range. According to data from GuruFocus, this company has a 10-year PER multiple bands of between 12x and 27x. At its current multiple of 26x, it is definitely priced to perfection.

According to analyst consensus, the company is expected to report FY2020 (financial year-end in January) EPS of $4.57, a 7.3% YoY growth rate. If that materializes (company expected to report FY2020 results beginning of March), the company would have achieved a superior track record of 15 years of consecutive EPS growth, an accolade extremely rare, particularly for a company in an industry (brick-and-mortar retail) that is in a structural decline.

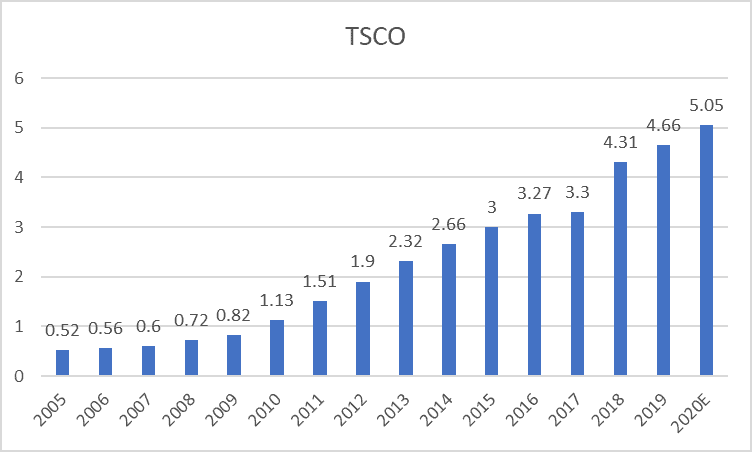

2. Tractor Supply Company (TSCO)

Tractor Supply Company is an American retail chain of stores that offers products for home improvement, agriculture, lawn and garden maintenance, and livestock, equine and pet care.

The retailer’s 3 largest categories are Livestock and Pet (47% of fiscal 2018 sales), Hardware, Tools and Truck (22%) and Seasonal, Gift and Toy product (19%).

Its customers are generally home, land, pet and livestock owners who have an above-average income and a below-average cost of living. Living in towns outside major metropolitan markets and in rural communities, they are often underserved by major retailers, both offline and online.

The company is the only major player focused on the rural-life retail space. Its most relevant competitors are Home Depot and Lowe’s but neither is seen as a threat.

At the same time, the majority of the rural-life retail space is immune to digital disruption as it is cost-ineffective for online platforms such as Amazon to ship bulky items with a limited ticket size.

Thanks to its economically stable customer base, the company is thinly impacted by economic downturns, with the company growing sales during the past 2 recessions back in the early 2000s and during GFC.

Management estimates a total market potential of 2,500 store opportunities. Compared to the existing store count of c.1,800 across 49 states, there are ample growth opportunities to be capitalized on.

On top of this, a rapidly growing pet economy which is seen as highly recession-proof alongside digitalization efforts by the company in support of omnichannel shopping could add fuel to the organic growth engine of the company.

The company is trading at a decent PER multiple of 21x which falls in the lower band of its 10-year range of 13x and 34x. If a recession is to materialize, we believe Tractor Supply has a resilient business model to ride out an economic downturn just like the one back in 2007-2009. A price correction towards the Peter Lynch Earnings Line which is at the USD70 price range vs. current price of USD98 could present a strong buying opportunity.

According to analyst consensus, the company is expected to generate EPS of $5.05 in 2020, which represents an 8% YoY growth rate (faster than ROSS Stores, yet at a lower PER multiple). The street also expects 2021 and 2022 EPS growth to be in the high-single-digit arena.

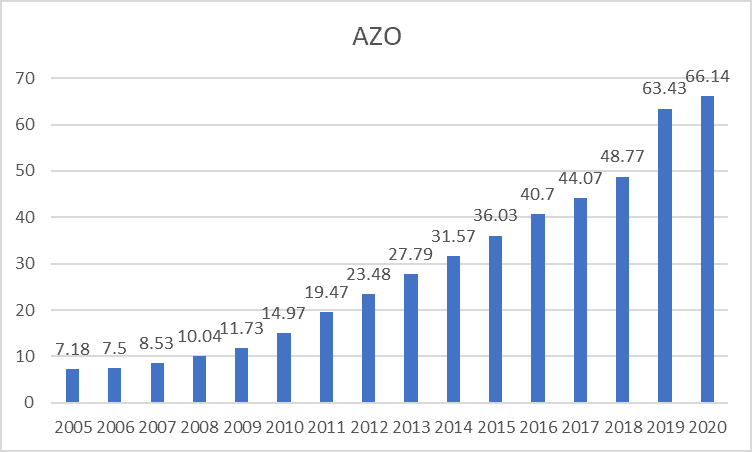

3. Autozone (AZO)

Autozone is an American retailer of aftermarket automotive parts and accessories, the largest in the US. Founded in 1979, AutoZone has over 6,000 stores across the US, Mexico, and Brazil.

The company opened 209 new stores in fiscal 2019 as part of its ongoing expansion plan, including 28 locations in Mexico and 10 in Brazil.

It is easy to see why AutoZone is a recession-proof business. In periods of weak economic growth, consumers tend to delay their new vehicle purchase, opting instead to prolong the life of their existing vehicle. This will involve purchasing automotive parts and accessories.

In order to boost its online presence, the company has made significant technology investments such as expanding its next-day delivery program and reducing customer wait time. For example, it introduced a new point-of-sale system that improved its electronic catalog to provide a more seamless transaction experience for its in-store customers.

Trading at a 2020 PER multiple of 16x, it is currently trading at the median multiple compared to its 10-year multiple bands of 11x-22x.

The street is forecasting the company to generate EPS of $66.14 for FY2020 which ends in August. This represents only a 4% YoY growth rate, the slowest since 2006 which might explain why its share price is currently experiencing some weakness.

The growth rate is, however, expected to accelerate back to double-digits in FY2021 and FY2022.

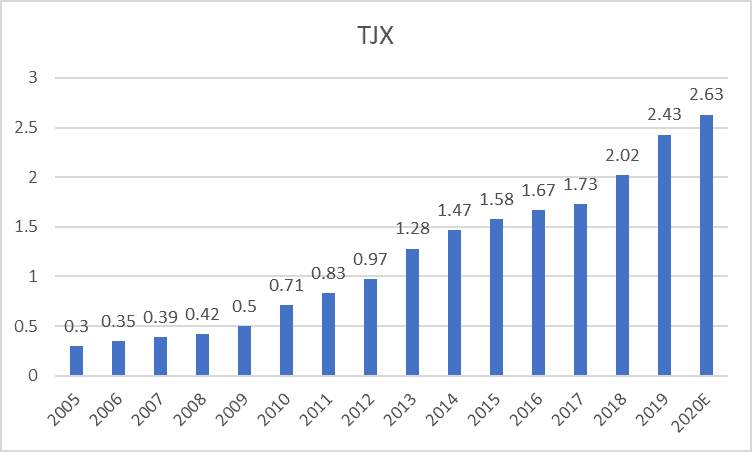

4. TJX Companies (TJX)

Similar to ROSS Stores, TJX Companies is an American multinational off-price department store corporation. There are over 3,300 discount stores in the TJX portfolio located in more than six countries.

The company has benefitted from greater sourcing opportunities due to a weaker-than-expected operating climate for major retail markets in the world, allowing the company to be increasingly selective regarding the types of products that it stocks across its stores as well as the prices it pays for them.

The company has seen increasing demand in its e-commerce segment, with value-added services such as being able to return items purchased online via its physical stores and vice-versa.

There are, however, potential risks associated with this business (as recession-proof as it might be), with margin weakness seen in certain segments such as HomeGoods due to increased costs in its supply chain as well as higher markdowns.

The tariffs placed on Chinese imports might also have a negative impact on its full-year performance where the street expects the company’s EPS growth to decelerate to “only” 8% on a YoY basis for FY2020 (financial year-end Jan).

Similar to ROSS Store, TJX is trading at the top band of its 10-year PER band, with the current 2020 PER of 24x (10-year range: 12-25x). It is slightly cheaper than ROSS store which is trading at 26x with a similar growth profile although the market likely attributes a premium to ROSS Store, the company being the market leader.

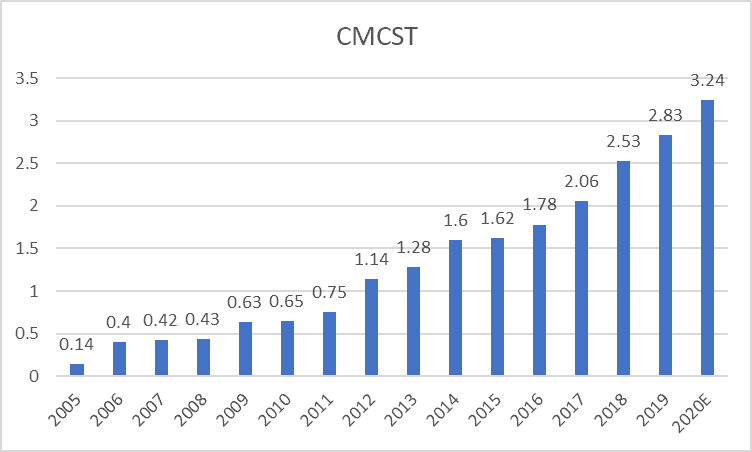

5. Comcast (CMCSA)

The only “odd one out” in this list, Comcast is the second-largest broadcasting and cable television company in the world by revenue and the largest pay-TV company in the US. The US Pay-TV industry recorded its largest-ever video subscriber decline in 2018 (lost of 2.87m customers, with the number likely doubling in 2019) amid cord-cutting and satellite TV providers’ decision to also stop chasing customers that are not profitable.

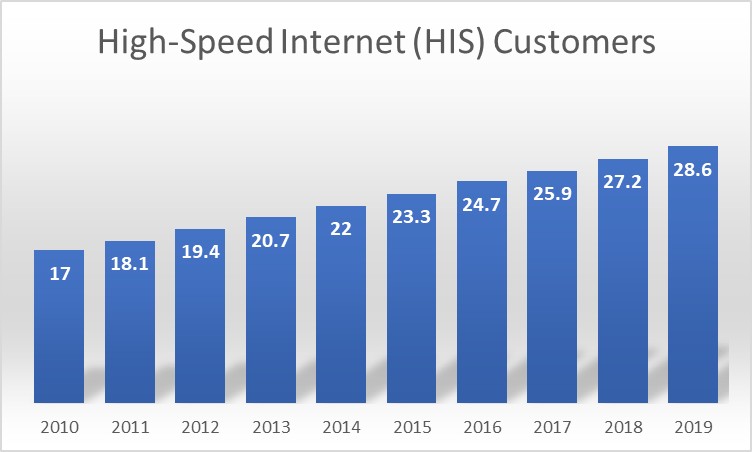

Despite the structurally declining Pay TV operational climate, Comcast’s Pay TV business remains profitable. However, the core business for them is now broadband services, signing up new internet customers to help compensate for the loss of Pay-TV customers.

2019 is the 14th consecutive year that Comcast has added more than 1m net high-speed subscriber customers (1.4m to be exact, the best results in 12 years), with each subscriber paying the company $600-650 a year.

Despite the credible earnings performance, share prices did not appreciate as much as expected due to headwinds stemming from the loss of video subscribers. Management expects the video subscriber declines in 2020 to accelerate even further from the 2019 YoY decline of 3.2%.

Analysts expect the company to report 2020 EPS of 3.24 which is a 15% improvement from the reported earnings of 2.83 for 2019. Trading at a forward 2020 PER multiple of 14x, the company seems to be trading at the lower range of its 10-year PER band of 6x-22x.

While its Pay TV business is in a structural decline and will remain as a strong headwind for the company, the rest of its core business remains strong and a very sticky one that will allow the company to escape unscathed when the next recession arrives.

Conclusion

It is extremely rare for any company to generate 14 years of consecutive earnings growth. These 5 companies have managed to achieve that, particularly credible amid one of the greatest recession in recent history.

In terms of valuation, most of these companies are trading above the average of their historical 10-year PER range, with the exception of Comcast, as its cable business remains bogged by the cord-cutting wave that is unlikely to recede over this decade.

Are there any more blue-chip US companies with 14 years or more of consecutive earnings growth?

Do Like Me on Facebook if you enjoy reading the various investment and personal finance articles at New Academy of Finance. I do post interesting articles on FB from time to time which might not be covered here in this website.

Join our Telegram broadcast: https://t.me/gemcomm

SEE OUR OTHER WRITE-UPS

- WHICH S-REITS HAVE THE BEST RECORD OF DIVIDEND GROWTH?

- A BETTER ALTERNATIVE TO DOLLAR COST AVERAGING?

- DIVIDEND YIELD THEORY – THE UNDERAPPRECIATED VALUATION TOOL

- TOP 5 ANALYSTS OF THE DECADE AND THEIR CURRENT FAVORITE STOCKS

- IS DRINKING LATTE REALLY COSTING YOU $1 MILLION AND THE CHANCE TO RETIRE WELL?

- DIMENSIONAL FUNDS: ARE THEY WORTH THEIR WEIGHT IN GOLD?

Disclosure: The accuracy of the material found in this article cannot be guaranteed. Past performance is not an assurance of future results. This article is not to be construed as a recommendation to Buy or Sell any shares or derivative products and is solely for reference only.